Technology in Collection: 21 Must-Know Buzzwords

Your Guide to Key Terms for Today’s Debt Recovery Strategy Reaching consumers today requires a more sophisticated process than simply dialing the phone or sending a generic email, especially when it comes to debt recovery and collection. But reviewing potential strategies can often leave you lost in a sea full of acronyms and buzzwords. Between terms like AI, machine learning, and data science, it can be difficult to keep up with the different definitions—and understand how they impact your business and bottom line. To help keep this word salad straight, we’ve compiled a glossary of helpful terms, definitions, and examples to help differentiate them: Accounts per employee (APE), account to collector ratio (ACR): The number of delinquent accounts that can be serviced by an individual recovery agent – often used to measure cost effectiveness.Artificial Intelligence (AI): AI is a blanket term describing a range of computer science capabilities designed to perform tasks typically associated with human beings. Machine learning (ML) is a subset of AI. Through AI, processes like debt collection can become more efficient by developing better outreach and deployment strategies.Big Data: This term means larger, more complex data sets . Big data can save collectors a lot of time by using many variables for analytics-based customer segmentation, insert, insert..Coverage: The percentage of users for whom organizations have digital contact information, such as email addresses or phone numbers.Customer Retention Rate: Measures the total number of customers that a company keeps over time. It's usually a percentage of a company's current customers and their loyalty over that time frame.Data Science: A cross-discipline combination of computer science, statistics, modeling, and AI that focuses on utilizing as much as it can from data-rich environments. Data science (which includes machine learning and AI) requires massive amounts of data from various sources (customer features such as debt information or engagement activity) in order to build the models to make intelligent business decisions.Deep Learning (DL): A subset of machine learning. Deep learning controls many AI applications and services and improves automation, performing analytical tasks with human intervention.Delinquency rate: The total dollars that are in delinquency (starting as soon as a borrower misses as a payment on a loan) as a percentage of total outstanding loans.Deliverability: The percentage of digital messages that are actually reaching consumers (e.g., as opposed to ending up in email spam filters).Digital engagement metrics: A range of KPIs that capture how effectively digital channels are reaching and engaging consumers.Digital opt-in: The percentage of users who have indicated their preference to receive digital communications in a particular channel.Efficiency: Measures a company's ability to use its resources efficiently. These metrics or ratios are at times viewed as measures of management effectiveness.Machine Learning (ML): Technology that uses algorithmic modeling techniques to observe patterns and trends, reassessing the best approach to achieve a goal, and adapting behavior accordingly. It continuously, automatically learns and improves at a massive scale as more data is observed. With the help of machine learning, companies can make sense of all their data and take on new approaches to debt collection processes from better customer experience to more efficient delinquent fund recovery.Net loss rate: The total percentage of loan dollars that get charged off (written off as a loss).Open rate, clickthrough rate: The percentage of users who are actually opening and clicking digital communications.Predictive Analytics: Predicting outcomes is one specific application of machine learning. It allows companies to predict which accounts are more likely to pay sooner and allows them to better plan operations accordingly.Promise to pay kept rate: The percentage of delinquent accounts that maintain a stated commitment to pay.Promise to pay rate: The percentage of delinquent accounts that make a verbal or digital commitment to pay.Right party contact rate: The rate at which a collections team is able to establish contact with the consumer associated with a delinquent account.Roll rate: The percentage of delinquent dollars that “roll” from one delinquency bucket (e.g., 60 days past due) to the next (e.g., 90 days past due) over a given timeframe.SMS: An acronym that stands for "Short Message Service" referring to text messages on cellular devices. For more information on how to get started integrating innovative technologies into your debt recovery strategy, schedule a consultation today.

Reaching Consumers Beyond Outbound Calling: Insights and Learnings from Collection Experts

If transforming the way you reach customers to recover delinquent accounts isn't on your radar in 2022, a year where projected delinquencies are expected to soar, you're at risk. Fortunately, we recently rounded up a panel of experts to share their insights and experiences taking those first steps away from outbound calling and toward better consumer communication in our webinar “What Labor Shortage, Wage Inflation, and Regulatory Restrictions Mean for Your Call Center”—available to watch on-demand now» Heather Bentley, Citizens Bank | John Craven Sr, Cox Communication | Jennifer Masterson, PNC | Richelle Rocazella, TrueAccord Below are some of the top questions, answers, and first-hand accounts from our discussion (plus some attendee poll results): What percentage of contacting consumers is done via phone vs other channels? Heather Bentley [HB]: Overall a little bit above 50%, but that includes outbound calling from live agents and interactive self-serve calls, which really is more the digital channel. John Craven Sr [JC]: Live agent we're at 0%. We do use a virtual agent, so I would say we use that virtual agent probably 40% to 45% of the time. Jennifer Masterson [JM]: We're close to 50/50. We will always be taking phone calls, but we are doing a lot more now in the digital space trying to contact people. Richelle Rocazella [RR]: Less than 1% of our communication is via phone. And that is all inbound when we do engage with our customers. We will only make an attempt to reach a customer via phone if they have requested a call. What does outbound calling versus an omnichannel strategy look like at your organization? JM: An omnichannel strategy triggers customers to get them to self-serve and frees up our agents to talk to customers that need more help or more assistance. That's really where the more valuable conversations happen. HB: It's really about putting the two pieces together [outbound and other channels], and trying to find the sweet spot of customer experience and collection effectiveness. Pulling those two things together - so if we find customers who are responding to a specific channel like text, but then if they go past the point we would normally see in delinquency, we can say, "Wait a minute, something's different. Now we need to call this customer.” JC: When you take a person that's spending a good portion of their day making outbound calls, and you turn them into an inbound agent where they're talking to a customer almost every time that the phone rings, the maximization of your employee's time puts you into a completely different realm of being able to perform. Was COVID or labor shortage and wage inflation a driving factor in the shift to a more digital approach and self-service approach? JM: We started before COVID because consumer behavior was dictating it. It's really hard to get someone to pick up the phone. The number of times that you actually connect to somebody live on dials is really low. That's really what drove us to start going down the digital path. Now, I think there's a ton of benefits to be gained from that, things like when COVID happened, this labor shortage. Once you have the channels in place, it becomes easier to ramp them up or down depending on what's happening in the economy. Once you have the channels in place, it becomes easier to ramp them up or down depending on what's happening in the economy. Jennifer Masterson, Executive Vice President, Retail Lending Solutions, PNC How did you get started? HB: We started individual channels at times with easy things like virtual messages, then interactive messaging and email and text, and then moved into two-way in those channels. And we're still working so that you could have the same experience in that digital space that you'd have with an agent on the phone. JC: In 2014 [Cox Communications] started texting customers and then we added email around 2017, but we didn't have a digital platform at that time. We implemented a digital platform in early 2020, and fortunately we were able to go full omnichannel with integrated channels that we were able to roll out. What are some of the challenges to building an omni-channel strategy? RR: Making sure all channels are integrated to develop a full customer experience journey. Also ensuring service levels are maintained as more channels are added. HB: If you're not sequencing [the channels] and working them together, it can be like bombing your customers again. If you're bombing them with calls and now you're bombing with text and with email and it's just, "Hey, we'll just try everything." You quickly desensitize your customers to your communications. JC: We set up all the channels and then we went on a journey to bring them all in and orchestrate them so they were working together. If I can suggest anything to those that are using the phone strategy, if you're ready to start your digital journey, start with a journey that is an orchestrated journey, instead of building out the channels and then trying to bring them all together. You'll get so much further ahead and a quicker response to digital integration. From a self-serve standpoint for debt collection and recovery, what are some of the compliance or regulatory challenges to keep in mind? HB: As we move to digital channels, [regulators] move their focus to what happens in email and on your website and in text messages, because before their focus has been about calling over the last 10 years. So as an industry we have to stay ahead of that and think both like a customer and like a regulator. Be a bit conservative in some of your interpretations of how far and wide your communications go. JC: From the risk side of things, if you're moving from an analog or non-digital traditional approach to a digital approach, think how to digitize your compliance rules that may have some risk mitigation in it. Don't create a new reality—make sure that you replicate what you have already in place to make sure you have safeguards. JM: On the phone side you're dealing with agents that have to remember to say things right. But coming out of COVID a lot of the banks and other financial institutions put hardship assistance online just as an example, and I think the regulators like that because everybody's essentially getting the same experience. I think it's easier to be in compliance and meet all the regulatory requirements in a channel like that, than it is with agents. As an industry, we have think both like a customer and like a regulator.Heather Bentley, Senior Vice President Head of Consumer Specialty Operations, Citizens Bank What was the best way organizations should have prepared to meet the guidelines for the CFPB’s Regulation F to move to a more omnichannel approach? RR: The best thing any organization could have done for Reg F would be to have a strong legal and compliance group that you work with. While it's not something that drives revenue, it is a must in every organization. Where would be an ideal place to start exploring or considering if you're moving away from the outbound call center and looking to integrate more channels? JC: Whatever your strategy is, you need to set yourself on a path making sure that your digital journey has a brain. Recognize that different profile customers react differently to different contact channels. As you use your omnichannel approach, having that brain mentality. Knowing what your customers' preferences are and then leveraging those preferences will set you on a great path to performance. JM: Every company is different in terms of what capabilities you have or don't have. While texting and emailing made sense for PNC at first, maybe there's another channel that a company can easily plug into. Start wherever you can because consumers don't want to pick up the phone and call. Whether it's the ideal option or not, give consumers another path and another option. Start somewhere and then build off of that in whatever way makes sense for your organization. RR: For businesses in the early stages of adopting a more omnichannel approach for collections, email or text would be a good place to start. Knowing what your customers' preferences are and then leveraging those preferences will set you on a great path to performance.John Craven Sr, Enterprise Center of Excellence Call Center Director, Cox Communication Watch the full webinar for even more insights, advice, and answers to even more audience questions» Ready to get started on the digital transformation of your collection strategy? Schedule a consultation to learn how you can take the first steps»

Say R.I.P. to Traditional Call Centers (But Don’t Be Sad)

“Death of the call center”—you may have heard this phrase before, but today’s labor shortage, wage inflation, regulatory risks, and changing consumer behavior are all nails in the coffin of this once sure-fire business tactic. But don’t say a final farewell to the call center just yet. There is a way to utilize those phones to more effectively reach your business goals—especially when it comes to recovery and collection operations. Let’s take a look at how call centers operate today, what factors threaten their effectiveness, and what we can do to make them viable again. You can take an even deeper dive and read our full coverage of “Outbound Calling Doesn’t Work, Here’s What Does” here» Outbound Calling vs. Inbound Servicing To understand how collections call centers can survive and remain profitable in recovering delinquent funds, we need to understand the difference between two basic functions of a call center: outbound calling vs. inbound servicing. Outbound Calling: Call center agents dial out directly to customers Inbound Servicing: Call center agents answer incoming calls made by customers A 2020 survey showed the effectiveness (or ineffectiveness) of outbound phone calls to collect debts due for more than 30 days. When we break it down, we can start to see that the outbound model to collect on delinquent accounts is truly on life support this time around. So What are the Killers of Outbound Call Centers in 2022? When the “Death of the Call Center” was first foretold back in the early 2000s, the culprit was firmly identified as the internet and technology taking over the call center career opportunities for people. But a closer look shows this isn’t the case given today’s massive shifts in the labor market, regulations, and consumer behavior. Labor Shortage & Wage InflationNew technologies aren’t pushing people out of working in call centers—people just don’t want outbound calling jobs like they used to. Competition to hire is fierce and compounded by the Great Resignation sweeping through the market. Unfortunately, many outbound call centers already faced notoriously high (and costly) attrition rates as well. On top of that, call center wages have increased by 15%+ since the pandemic began, an astounding spike even when every industry is riding the wave of wage inflation. Regulations & Consumer ExpectationsOutbound dialing platforms must comply with a long list of regulations—especially in the debt recovery and collection sector, like the TCPA, FDCPA, and Reg F—all before they can even start talking about recovering delinquent accounts…that is, if anyone even answers their call. Consumer preferences have moved away from talking on the phone and moved towards self-service options online. Do a quick google search on how to stop debt collection calls and an endless amount of articles will pop up. But overall, consumers have found an even simpler solution: don’t answer the phone. So can you actually connect with your customers through a call center? A Second Chance for Call Centers In the wake of changing labor markets, regulations, and consumer behavior, businesses must evolve to integrate digital-first solutions into call center operations to save manpower, regulatory compliance efforts, and customer satisfaction. We may be perpetuating the old trope, but 2022 really could spell the end for outbound call centers as we know them, and be the opportunity to transform them into inbound engagement centers. Find out how in our full coverage of “Outbound Calling Doesn’t Work, Here’s What Does” here» None of us should be sad to see it go. Not consumers, not employees, not businesses. It’s time to say R.I.P. to outbound calling for the betterment of all.

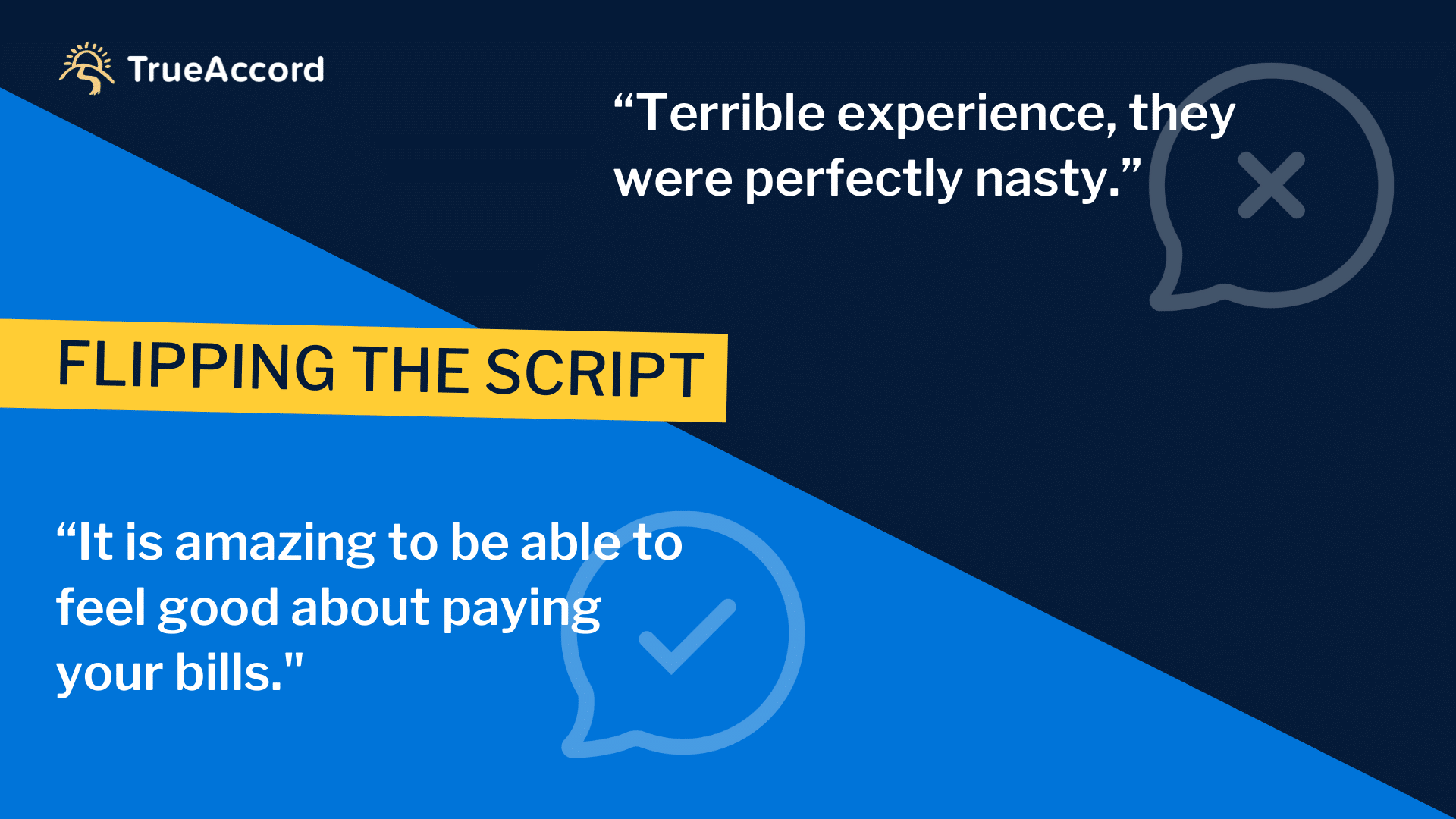

Flipping the Script: Collecting with Kindness

Historically, debt collectors have been depicted as hostile, intimidating or downright rude - and over the years they’ve confirmed those stereotypes through aggressive phone calling and deceptive tactics. But to what success and at what cost? We know there’s a better way. The idea of compassionate, considerate consumer communication is behind TrueAccord’s approach to debt recovery and drives our innovation, and based on what we’ve seen, we believe there’s a lesson to be learned for others in the debt collection space. In collaboration with OnePoll, TrueAccord recently surveyed consumers about their financial regrets and found that 63% of respondents had some amount of money in collections. While 88% of respondents didn’t have any past experience with accounts in debt collection to report, the 12% that did weren’t so lucky, and their experiences were pretty awful. We don’t like to hear about consumers being treated badly and reading these consumer comments brings to light the problem we’re trying to solve. So what are consumers’ complaints about their experiences with debt collectors? Here are just a few: “A million phone calls a day.”“I was disgraced in a public place.”“Relentless and rude, judgemental and uncaring.”“Terrible experience, they were perfectly nasty.”“They are mean and evil and clever and make you feel terrible about yourself.”“They get angry when I don't have the money to pay back in time.” We’re here to flip the script. At TrueAccord, we don’t call consumers to collect past due debts, and we certainly don’t threaten or harass. By using a digital-first communication approach and friendly, humane messages, we actually connect with consumers and they feel empowered and motivated to pay. Don’t believe us? Here’s some real-life customer feedback from people TrueAccord has helped out of debt: “Thank you for your patience and understanding!”“Love the email communication and the ability to pay online.”“I actually looked forward to making payments because I felt there was a sense of mutual respect between myself and TrueAccord. It felt good to take care of a lingering debt.”“Thank you for your kindness, patience and professionalism in the wake of hardship.”“It is amazing to be able to feel good about paying your bills. You helped me all the way. No pressure.”“My experience with TrueAccord was seamless. Truth be told, it's the first time I've ever enjoyed time spent with a debt collection company!” So far the kindness approach has worked for TrueAccord - with more than 16 million customers served, we pride ourselves on our 4.7 on Google reviews, A+ rating with the BBB, and overwhelmingly positive customer feedback, not to mention our industry-leading recovery results. We’re proving that when you treat consumers with respect and kindness you can actually achieve better results for your business and customers. Interested in finding out more about how outbound calling for debt collection is a thing of the past, our approach to digital-first debt collection and how it can work for your business? Check out "Outbound Calling Doesn't Work, Here's What Does" for more.

Reading Between the Student Loan Headlines: How to Engage Consumers with Multiple Debts

The freeze on student loan payments has been a hot topic since the start of the pandemic—not just for borrowers, but for debt collection departments outside of the student loan debt sector. Although student loan borrowers get a reprieve for another few months, repaying other debts can still be a tricky issue for consumers to budget for today. Debt collectors need to find ways to start engaging with borrowers now before student loans get added back on to the balance. The Freeze Continues Through the Summer On April 6, 2022, only weeks before collections were set to resume in May 2022, the Biden administration announced another four-month extension on the freeze for federal student loan payments, interest, and collections. After granting several extensions due to the ongoing Covid-19 pandemic, the decision to further extend the pause reflects the challenging economic landscape and unmanageable financial burden faced by many Americans. While this is another round of relief for the approximate 42.9 million Americans with student loan debt, the proverbial can is just getting kicked farther down the road as the relief is only temporary. Additionally, uncertainty leading up to the announcement left many in what has become a familiar anxious limbo of whether or not they would be expected to restart their payments; and that uncertainty can have a broader impact for debt collections beyond student loans. Don’t Forget the Debts that Don’t Have an Indefinite Moratorium Student loan debt collection may be dominating the headlines, but it is often not the only financial burden borrowers are carrying. Out of the number of adults with student loans, about 23 million (69%) have at least one additional type of debt, according to the U.S. Census Bureau. Looking at it even closer, surveys found that among those with student loans, consumers also had: Credit card debt (52%)Vehicle loans (33%)Medical debt (18%) The newscycle focus and the ongoing uncertainty of student loan repayments can be confusing to borrowers with multiple debts who are prioritizing based on their cash flow, putting them at an increased risk for delinquency. As noted in our Q1 Industry Insights, February marked the 9th month in a row with increasing 30+ delinquency rates on a unit basis across debt types, notably delinquency increases in first mortgages, second mortgage, auto leases and unsecured personal loans. And with student loans once again receiving temporary relief, these consumers will likely focus on repaying their other debts. The key for collectors is to understand how to engage with consumers that have limited budgets through a variety of affordable repayment options. Engaging Consumers Digitally with Repayment Options The first step is to actually connect with consumers to stay top of mind. While phone calls can go unanswered and canned emails go ignored, reaching customers through customized, digital-first communications can help businesses recover more by reaching those that are ready to repay debts. Consumers already use these types of platforms to interact—surveys found that 46% of people exclusively use digital channels for their financial needs, including banking and bill paying. The second step is to offer consumers repayment options and flexibility knowing they may be balancing multiple bills. With so many financial options at their disposal, consumers have to monitor an increasing number of accounts for banking, credit cards, autopay, recurring payments, installment plans and more. The ability to choose a payment date that aligns with paydays or to push back a payment when something unexpected comes up are invaluable for consumers and will actually lead to brand affinity and better customer experiences. With so much uncertainty already swirling around student loans, businesses have a better chance of successfully reaching and recovering other debt payments if they do so in a way that is familiar to the borrower and provides flexible ways to manage repayment. TrueAccord helps reach consumers where they are when they need to be engaged with through a digital-first approach that cuts through the clutter of other communication channels. Discover how to expand and customize your communication channels for each individual consumer and engage faster with better results. Schedule a consultation today»

Q1 Industry Insights: Consumers Will Consume, Lenders Will Lend, Delinquencies Will Rise

It’s the end of the quarter and, as always, we at TrueAccord are looking at consumer debt trends that will impact our industry and beyond. The four key trends we’re studying are: resumed foreclosure activity, extensive medical bills, the end of child tax credits and historically high inflation. Add these all together and the financial outlook for consumers, especially those in debt, is scary. But there are silver linings, as well. For one, the consumer credit market is looking strong with signs of expansion, specifically, originations for credit cards and personal loans are increasing. Second, the fintech industry continues to grow and evolve to meet the changing needs of consumers, offering more opportunities for financial inclusion and innovative customer experiences. The Downside Look, coming out of a pandemic and into a tumultuous international economic situation, we don’t expect it to be easy. But some definitely feel it more than others. For many families, government stimulus through child tax credits (which ended in December) was helpful in covering the gaps in income from pandemic losses, but it wasn’t enough to prepare them to take on new expenses and restart all the financial obligations that were temporarily on hold. In fact, a recent report from the Columbia University Center on Poverty & Social Policy found that 3.7 million U.S. children were plunged back into poverty by the end of January when child tax credits expired, indicating that the stimulus was making a significant financial difference for many families. In January, the foreclosure proceedings that were paused under the CARES Act resumed after an 18-month hiatus. In January alone this amounted to 56,000 foreclosure starts, up 29% from the month prior. But that doesn’t tell the whole story: 964,464 mortgages are still seriously delinquent and not in forbearance, with 49% in loss mitigation plans. Even more concerning, of those 474,071 borrowers in loss mitigation, 72% just aren’t paying. The average American household is now paying an additional $276 per month on expenses thanks to record-high inflation. And don’t forget pandemic-related medical expenses from Covid-19 testing and treatment. A recent survey found that 56% of Americans, with or without insurance, owe health-related debt, and almost one in six people with medical bills aren’t paying them off. And it’s not just medical bills. According to Experian’s latest Ascend Market Insights, February marked the 9th month in a row with increasing 30+ delinquency rates on a unit basis across debt types. Their data shows that 30+ day past due accounts showed a 7.59% increase month over month with notable delinquency increases in first mortgages, second mortgage, auto leases and unsecured personal loans. Additionally, month over month views of roll rates show 0.91% of consumer accounts were rolling into higher stages of delinquency in February 2022. This indicator has now returned to the same level as the start of the pandemic in March 2020. While student loan payments are still paused through May, the day is quickly approaching when many will see their financial obligations increase yet again, compounding the burden and financial pressure on consumers. The Upside In spite of the challenging economic landscape, the good news is that consumers now have more options when it comes to lending and personal finance, and they’re taking advantage of them. Higher costs of living and, for some, sustained unemployment (partially influenced by the Great Resignation) are driving consumers to look for new lines of credit to manage expenses. According to TransUnion, originations for personal loans are expected to continue rising in 2022 to both non-prime and prime and above consumers, reaching pre-pandemic origination volumes last seen in 2019, while credit card origination and balances will hold steady near pre-pandemic levels. And lenders are happy to lend. Between extra cash on hand from government stimulus, pauses on many financial obligations and new cash flow budgeting options like BNPL taking the payments industry by storm, consumers actually did a pretty good job managing their finances in regard to repaying debts during the pandemic. Delinquencies were at record lows, causing lenders to become more comfortable serving subprime segments that were performing well. As a result, originations for credit cards and personal loans have returned to pre-pandemic levels and have been holding fairly constant over the last two quarters. This bodes well for financial inclusion and the bevy of fintechs looking to get in on the action. From eCommerce and retail to banking and money transfers, every sector features a fintech company that’s innovating digitally to provide more people with better financial access and positive customer experiences. A recent report by Plaid includes key findings about what consumers want from their financial services: 1) apps and services that work when and how they want and that make it easier to manage money, 2) interoperability, with apps and services providing connected experiences, regardless of the providers, and 3) services that not only help them save money but achieve better financial outcomes. And guess what? Fintech companies are delivering. According to research from Bloomberg, fintech companies now originate 38% of U.S. unsecured personal loans, with a large presence in the mortgage and auto loan categories. Boiling This All Down Remember when stimulus money was flowing, consumers weren’t spending as much (because what was there to do?) and instead taking the opportunity to pay off loans and debt and save at record rates? Those times are gone and signs show that consumers are looking to use more credit and take on new loans in response to economic pressures. Unfortunately, a rise in originations will inevitably lead to a rise in delinquencies, especially in a challenging and unpredictable economy. Knowing what comes next, now is the time to start thinking about pre-default and keeping consumers on track with payments and out of collection. For lenders, this means engaging delinquent customers early on when the first signs of slippage occur, and how you do that is important. Consumers today expect a seamless, personalized experience in every financial transaction, and the right recovery operations can continue to deliver that all the way through the customer journey when you have the right strategy in place. If you don’t know where to start in building a strategy, our Recovery & Collection Starter Kit is a good place.

TrueAccord Rolls Out Web Chat in Time for Tax Season

TrueAccord is an intelligent, digital-first collection and recovery company that uses the industry’s only adaptive intelligence: a patented machine learning engine, powered by engagement data from over 16 million consumer journeys, that dynamically personalizes every facet of the consumer experience in real-time. Our team takes innovation seriously and works tirelessly to provide product and service features that deliver outstanding results for clients and customers. Here’s what’s new from TrueAccord. Feature Update: Web Chat Tax season is upon us and in the debt collection industry that means consumers have access to refunds. According to the National Retail Federation, of the 59% of consumers who are expecting a tax refund this year, 33% plan to spend their refund on paying down debt. For this reason, mid-February through May is considered the most productive time of the year for debt collection with many consumers receiving tax refund money and opting to use this extra cash to catch up on their finances. During tax season, it is important to manage the large volume of inbound requests while also maintaining the quality of customer interactions. As a digital-first company, TrueAccord invests heavily in strategic communication with consumers where and when they want it and doesn’t rely on a large call center operation. With an expected increase in inbound communications during tax season, the TrueAccord team determined that a digital-first live chat feature would align with customer contact preferences and enable better customer service during peak times. To solve for this, TrueAccord launched a custom web chat interface in advance of tax season, which is visible to customers as a chat “bubble” on the consumer-facing web pages. The solution offers myriad benefits to both customers and customer service agents including reducing call volume, improving agent capacity to handle multiple consumers, assisting in managing tax season volume and providing a consumer-friendly self-service option for most commonly asked questions. The result? We’ll monitor and analyze how the new web chat feature performs during this year’s tax season, but consumer surveys have shown that web chat is preferred by 41% of consumers over phone, email and social media support, so we anticipate high customer utilization. The expected outcomes of web chat implementation for tax season are: Improved user experience by offering a preferred method of communicationReduced in in-bound call volume Increased accounts closed rateManaged tax season volume and Improved quality service levels across all operations communication channels with self service options for most commonly asked questions and inquiries now via web chat

Building a World-Class Recovery & Collection Strategy: The Complete Starter Kit

Delinquencies are a predictable reality for any business that handles payments, but the most efficient and effective way to recover delinquent funds isn’t always as predictable. A recovery team could theoretically chase down every last delinquent dollar. But it would soon reach the point at which the operational cost of the effort – and the associated legal and reputational risk – would cut into profitability. With so many factors involved, it can be difficult to even know where to start… The planning process should start with an in-depth understanding of what makes a world-class recovery strategy in today’s digital-first age, a look at the big picture for your specific industry all the way down to your detailed metrics, and KPIs that should be steering your strategy. Consumers expect a seamless, personalized experience in every financial transaction, and your recovery operations can continue to deliver that all the way through the customer journey when you have the right strategy in place. There is no one-size-fits-all when it comes to debt recovery and collection, but getting started doesn’t have to be daunting when you have the right resources to get you going. Beyond Best Practices and into Actionable Tactics Go beyond general best practices and start plugging in your own data with the tools inside our new Recovery & Collection Starter Kit. We have assembled guides, calculators, cheat sheets, and more to provide the frameworks and metrics for your organization to get started architecting the right recovery strategy for the long run. Each starter kit includes: World-Class Recovery Guide — pick your industry edition!Manage delinquencies without sacrificing consumer experienceBalance performance with operation metrics and consumer-focused KPIsCompare, contrast, and evaluate in-house vs partner collection strategiesCheat Sheet: Top KPIs for Your Recovery Operations Differences between traditional debt collection metrics, digital engagement tracking, operational KPIs, and moreNew consumer-centric KPIs for today’s most effective recovery strategy How to calculate profitability of a collection operation using operational metricsInteractive Recovery & Collection CalculatorEnter your business's KPIs to measure the profitability of your recoveryDiscover opportunities to improve the reach, resolution funnel, and cost effectiveness of your recovery operationScenario plan how much in additional revenue and cost savings the shift to an intelligent, digital strategy can drive for your businessChoosing a Recovery Partner: Top 6 Questions to AskDetailed questions on communication, technology, risks, and moreWhy each question matters for both profitability and consumer-experience Based on each question, what to look for in a potential partner’s responses Download your Recovery & Collection Starter Kit now>> These tools will teach you how to maximize profitability by efficiently recovering money lent to customers or members—while simultaneously maintaining consumer loyalty. Now is the time for businesses across verticals to embrace a disruptive, obsessively consumer-centric mindset for recovery and collection, and experience the results of this new approach.

Survey: Consumers Talk Financial Regrets, Credit Scores and Debt

Most Americans are in enough credit card debt, they would do anything to go back in time and change the outcome of their financial situation, according to new research. A survey of 2,000 general population Americans examined how they tackle their financial hurdles and found the average person owes $3,083 to credit card debt. Many respondents shared their financial regrets over the years, from not setting up a retirement plan when they were younger (51%), to not paying close attention to their credit score (43%) and buying goods that were too cheap (41%). Three-quarters (76%) have made an average of five financial decisions they regret in the past five years. And those who are eager to get out of debt (76%) have already planned their “debt free” celebrations once they finished paying all their dues. Conducted by OnePoll and commissioned by TrueAccord, a digital debt collection company, the study revealed 77% of respondents have lost an average of nine hours of sleep per week due to their financial woes. When they’re in a financial crisis, 63% of people will turn to someone they trust — with half turning to their parents, 48% to their best friend and 46% to their primary bank. Overall, 87% of people credit their financial “wins” to the people who had given them advice, while seven in 10 (71%) said they’ve learned from others’ financial mistakes. “There are close to 80 million Americans with past due debt and most want to pay it off and move on with their lives. But that is exceedingly difficult, especially in a debt collection system that treats consumers poorly and is more interested in process than simplifying debt repayment,” said Ohad Samet, founder of TrueAccord. “What we see more and more are consumers in debt who want to pay off their balances but are met with challenges of communicating with collectors, financial literacy and budget considerations that create roadblocks to being debt-free.” For many Americans, recovering from financial regrets starts with their credit score. The average person doesn’t understand the importance of their credit score until they’re 28 years old, but believe it’s better to start building a credit at 25 years old. Over four in five (84%) said maintaining a good credit score is important to them, with nearly as many (81%) saying it’s even more important than their social lives. https://www.youtube.com/embed/E2qshqslyxw Respondents also recalled the feelings they have when they see their credit card statements and when they’re about to make a payment. When seeing their statements, 31% said they feel confident and 24% feel fear. On the other hand, people feel satisfaction (36%) and happiness (22%) when making a payment. While 38% don’t plan on taking out any kind of loans in 2022, many are already making plans for loans in the year ahead — including credit card loans (34%), personal loans (33%) and mortgages (30%). “For those who are able to repay their balances, there may still be a longer-lasting impact to their credit score that can be difficult to remedy and further inhibit financial stability,” added Samet. “People will continue to borrow money when they need it, but what’s important is that they are informed on loan or credit terms and have a financial plan in place to ensure they’re making smart spending and repayment decisions. At the end of the day, though, getting into collections is often the result of trauma — loss of work, a healthcare crisis, and so on — many of them unexpected.” TOP 10 FINANCIAL REGRETS AMERICANS HAVE Not starting a retirement plan while I’m young 51%Not paying attention to my credit score 43%Buying cheap goods 41%Defaulting on payments and ending up in debt collection 41%Overspending on credit cards that I can’t afford to repay 38%Buying a car without knowing what’s involved 37%Letting student debt accumulate 36%Getting locked into fixed interest rates 29%Not investing money while I’m young 26%Not buying a home/property while I’m young 25%

How to Use Recovery KPIs: Your Keys to Building a World-Class Strategy

Measuring the success of a recovery strategy goes beyond just the dollars and cents recovered. Yes, the goal of a recovery operation is to maximize profitability by efficiently recovering money lent to consumers, but other key factors — like consumer experience and retention — are also important in evaluating the success of your business. A recovery team could theoretically chase down every last delinquent dollar, but doing so is often not worth the operational cost of the effort, and the associated legal and reputational risk can cut into profitability. In this blog post, we’ll share the most important key performance indicators (KPIs) for collections and recovery — and how you can use them to create a seamless, scalable, and world-class recovery practice. Meet the Metrics Whether looking at portfolio performance, operational profitability, or consumer experience, different KPIs play a role in measuring the success of a recovery strategy. Collectively, these metrics make up the “language” of recovery and collection — helping organizations understand the fundamentals of their operation. Here are a few of the most integral metrics to know: Accounts per Employee (APE) or Accounts to Creditor Ratio (ACR): the number of delinquent accounts that can be serviced by an individual recovery agent Net Loss Rate or Net Charge Off Rate: measures the total percent of dollars loaned that ended up getting written off as a loss Delinquency Rate: total dollars that are in delinquency (starting as soon as a borrower misses a payment on a loan) as a percentage of total outstanding loans - often an early warning sign on the total volume of delinquent debt Promise to Pay Rate: the percentage of delinquent accounts that make a verbal or digital commitment to pay Promise to Pay Kept Rate: the percentage of delinquent accounts that maintain a stated commitment to pay Roll Rate: the percentage of delinquent dollars that “roll” from one delinquency bucket to the next over a given period of time - provides visibility into the velocity with which debts are heading into charge off Profitability of a Collections Operation Formula: R x ResF x E R [Reach]: percentage of consumers in delinquency can you actually reach ResF [Resolution Funnel]: how effectively you can convert initial contact with a consumer into a commitment to pay – and ultimately, a payment promise kept (see Promise to Pay Rate and Promise to Pay Kept Rate) E [Efficiency]: calculation of what the “unit economics” of your collection are and how much it costs, on average, for every account that you rehabilitate The following diagram highlights the relationship between these core operational metrics of a recovery strategy and portfolio-level outcomes. In the hyper-competitive financial services space, consumer experience is a source of competitive advantage. That’s why it stands to reason that alongside the “traditional” metrics we see above, forward-looking fintechs and lending organizations should include KPIs that measure the value of consumer experiences: Net Promoter Score (NPS): how likely a consumer is to recommend a given brand after an experience with a brand’s collection organization Customer Retention Rate: how likely a consumer is to be reacquired by a given brand after his or her delinquent account is rehabilitated How to Make the Most Out of These Metrics So you have traditional metrics and consumer-focused KPIs, but how do you use it all? Managing performance with operational and consumer-centric metrics requires understanding the economics of recovery. Successful organizations will use the data to measure trends against the company’s own historical data, evaluate partners and strategies, and understand the big picture. Understand the Big Picture Visualize the relationship between operational metrics and portfolio-level outcomes. Conduct scenario planning exercises (e.g., “if we were able to improve the reach of our efforts by 25% through digital outreach, we would be able to reduce our net loss rate by 750 basis points”). Measure Trends Longitudinally Benchmark against a company’s own historical data as the collection team rolls out new strategies and tactics (e.g., “we boosted our promise to pay kept rate by 350 basis points relative to the previous vintage with pre-payment date reminders”) Evaluate Partners Assess potential collection vendors against a standard slate of metrics and KPIs (e.g., “of the three vendors that we evaluated for our collections, which one led to the greatest reduction in roll rate?”) Moving Towards World-Class Recovery Understanding collection KPIs and how to use them is a critical part of creating an effective recovery strategy — learn about all the components of a successful collection operation in our new ebook, the Guide to World-Class Recovery. Available for download now, this ebook provides the tools and frameworks to ensure that you’re architecting the right recovery strategy for your company for the long run. Download the Guide to World-Class Recovery»

Get started right now.

Whatever your organization’s technical needs, we have the tools and experts to onboard you today.

Get Started