Over the past two years, revolving credit card balances have grown more than 25% and are now above $1.2 trillion. Additionally, personal savings rates are stubbornly holding near 65-year lows, and combined with higher interest rates driving higher minimum payments, consumers are obviously feeling the stress. At the same time, delinquency rates on these higher balances have increased over 45%, putting significant strain on bank credit losses.

So what can lenders do? Let’s start by looking at what consumers want, and what outbound calling agents would like to see as well.

What do Customers Want? And What do Agents Want?

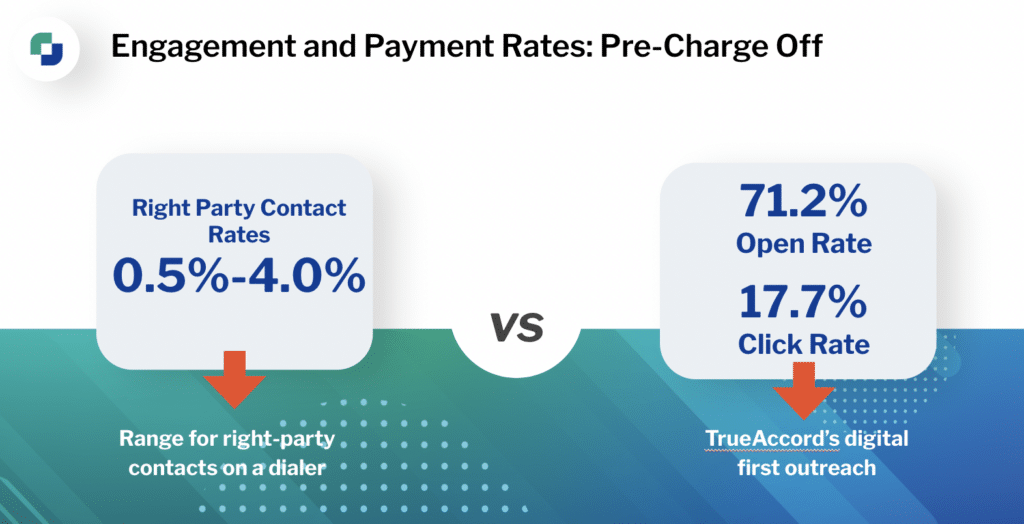

For businesses executing outbound call strategies and leveraging dialer technologies, the range of right party contact rates are anywhere from a struggling 0.5% to 4%. With these diminished returns of connection rates, calls become more expensive and less impactful.

It’s no secret that consumer preferences are changing rapidly and younger generations especially do not want to answer phone calls—and it’s important to keep in mind these younger borrowers will be the customers businesses will be servicing for the next 30 to 40 years, especially in a delinquent environment.

In general, consumers want to pay off their debts, but they want to be able to do so when it’s most convenient for them, which is often outside the “presumptively convenient times” between 8am and 9pm. In fact, 25% of payments come in after 9pm or before 8am. At TrueAccord, results show that more than 96% of customers resolve debts without any human interaction when digital options are offered.

But what does that mean for the humans dialing phones for traditional call-and-collect methods?

When businesses deploy an outbound call strategy before digital, often agents are shooting in the dark despite good intentions and dedicated efforts—which can affect outbound agent morale, making it a difficult environment to hire and retain top talent. And given today’s economic landscape, it’s challenging to call and collect from people who are behind on their bills or payments when so many other financial obligations are competing for dollars.

The key: let agents do what agents are good at—the human touch—but leverage digital as the first touchpoint. Let digital get the customer to understand where they are in delinquency. If and when they want to talk to a human, agents are there to do what agents do best: empathize and resolve any issues that digital cannot.

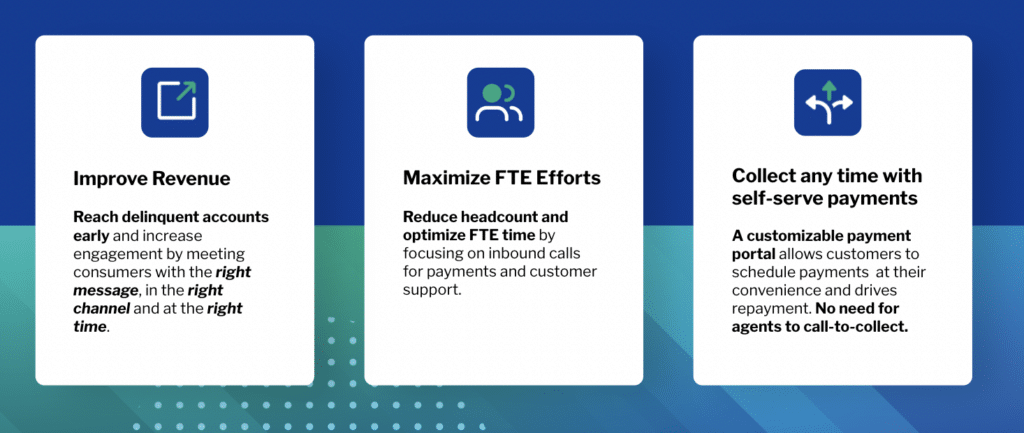

Agents are able to attend to higher-value inbound calls when digital, self-serve options are available for those who just want to make a payment—and it allows those customers to do so in a more convenient, preferred way.

Digital-First, Save More

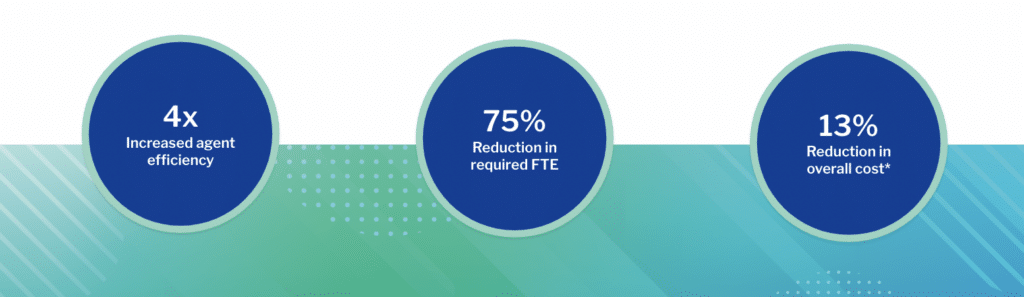

Digital early stage solutions reduce collections costs for leading organizations across industries by making full-time employees (FTEs) more impactful (or even lowering FTE headcount) and reducing overall expenses while maximizing repayment rates.

Companies that do rely heavily on an outbound call strategy must realize how expensive each call becomes. The longer that an account is in delinquency, every call becomes more expensive because the likelihood or the propensity to pay diminishes as the debts get older in age. So being able to automate and find those right channels at the right time with a digital strategy will help those phone calls get better results.

Plus, the digital first strategy is infinitely scalable—it doesn’t matter how rapidly a business grows on the frontend for lending or on the backend with new accounts that fall into delinquency. This digital-first approach allows companies to mitigate against turnover or having to compete for talent in the market. And again, FTEs can now be more effective in the delinquency cycles where phone calls are preferable, especially as accounts get further into delinquency.

Making outbound phone calls absolutely serves a vital part of a business’s omnichannel strategy, but deploying digital first will make those calls more cost-effective. It also delivers a stronger connection rate by identifying those preferences through feedback from leveraging a digital-first communication strategy.

Think about how this data can help businesses not only from a performance and liquidation perspective, but by learning from which customers are opening communications versus which ones aren’t. Those that don’t respond to digital should go to the top of the call queue because the data points towards a probable preference for person-to-person calling.

TrueAccord Difference

Learning from these digital engagements is vital for optimization, but if an organization is new to digital communications or has only been sending mass-blast, one-size-fits-all emails, it can feel like an uphill trek to start getting insights to drive better results.

But by partnering with TrueAccord, who’s been mining consumer engagement data for over 10 years, businesses get plugged in and start benefiting from our data from the get-go. Being able to automate with TrueAccord allows your company to focus on inbound human interactions while simultaneously, TrueAccord’s first-party, client-labeled platform sends effective digital communications to all of your past-due accounts.

The bottom line benefits of working with TrueAccord:

Maximize the productivity of your business’s resources with a managed, digital-first approach that enhances the efforts of your FTEs and overall collections operations. Start with a consultation today!