TrueAccord was built as an automated system from day one. Customer care experts handle the cases that needed special care, and teach the machine how to improve. We learned how to do that through a lot of hard work and testing, and we’d like to share some of that with you. In this free eBook, you’ll:

Learn about the different types of automation

Read from TrueAccord’s experience about the benefits of automation

Read about the three keys to a successful automation project

The technical and analytical vision behind TrueAccord is to add data-driven decisions to the communication model in debt colelction. Digital communication enables better data collection, and better understanding of customer behavior patterns. We can collect and observe open, click and browsing patterns that sometimes do more to explain how to engage with a customer than explicit communication. By connecting customer behavior to their mental state, and responding to that state with corrent language, we were able to substantially increase engagement on our collection communication.

We write quite a lot about the law, compliance, and other “boring” stuff over here at TrueAccord. The thing is, we don’t think these topics are boring. Regulation, the law, and working with regulators is something you have to embrace when entering a highly regulated space. Our ability to introduce innovation in debt collection requires multiple skills. Among them, it hinges on our ability to combine forward looking technology with just enough understanding of how to talk about it with regulators. This means taking an active roles in commenting, debating and when possible – crafting opinions about the law itself.

This is why we’re happy that our General Counsel, Avital Gertner-Samet, was appointed to the Consumer Financial Services Committee of the Business Law Section of The State Bar of California (aaaaand… breath!). Seriously, debt collection is no monkey business, and joining these organizations is our way of contributing our thinking to the variety of voices influencing the law.

Congratulations, and to our new partners at the State Bar – we look forward to working with you.

The TrueAccord product can be compared to an automated marketing and sales campaign, focused on identifying payment intent and acting on it. The system classifies customers (we use “customer” to refer to those in debt) by their most probable reason for non-payment, and the “voice” we think is going to drive that to action. Then, it has to decide, out of the hundreds of content items we have, which goes out to which customer, through what channel, and when. Of course, we’d like to learn from history and send the combination most likely to succeed. This raises the important question: what’s “success” in our context?

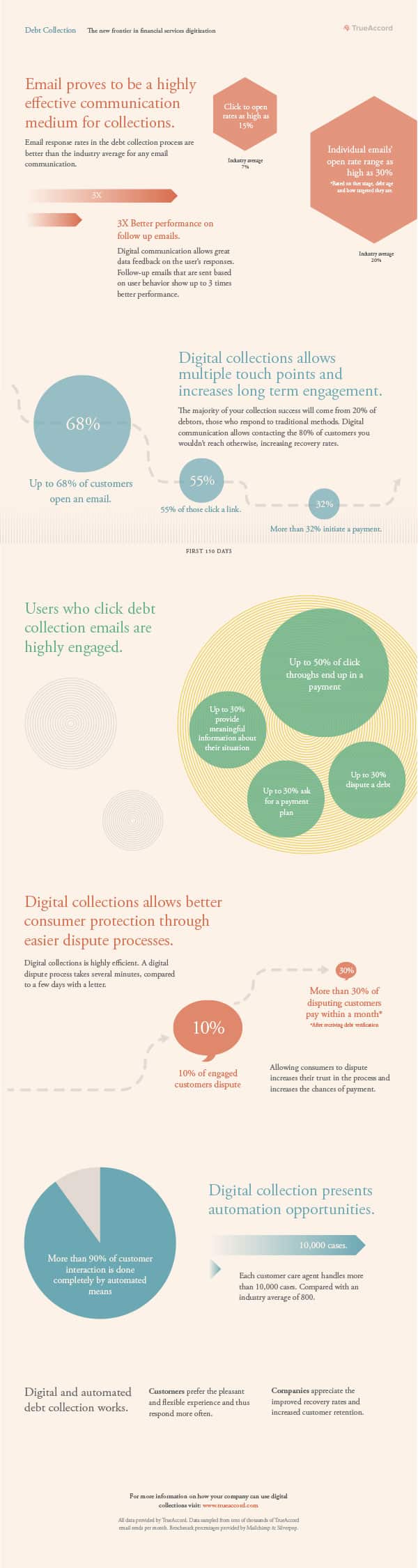

Ever wonder what the numbers really look like for digital debt collection? As it turns out, pretty good. Our design team released this infographic showing how our system is performing across different dimensions. Happy reading!

When we started working on TrueAccord, we had a limited understanding of various technical aspects of the problem. Naturally, one of those unclear aspects was the data model: what data entities we will need to track, what will be their relationships (one-to-one, one-to-many, and so on), and how easy it is going to be to change the data model as business requirements become known and our domain expertise grows.

Using Protocol Buffers to model the data your service uses for storage or messaging is great for a fast-changing project:

adding and removing fields is trivial, turning an optional field into a repeated field and so on. If we modeled our data using SQL, we will be constantly migrating our database schema.

the data schema (the proto file) serves as an always up-to-date reference documentation for the service’s data structures and messages. People from different teams can easily generate parsers for almost every programming language, and access the same data.

We started TrueAccord to make a difference in the debt collection industry, and that includes shining a light on practices that may not be illegal, but we think are either unethical or promote unethical behavior. We started by reviewing the downsides of quotas in debt collection, and today we’d like to touch on another burning issue: convenience fees.

Charging convenience fees for certain type of payments (card, electronic, or every payment that isn’t cash) is a common practice in debt collection. Even if the agency you’re working with aligns well with your values and expectations (a tough proposition in this fragmented market), you should be very careful about allowed convenience fees, for the following reasons:

Getting a debtor on the line, or to respond to an email, is a hard task. Customers don’t end up in this point if they have money and intend to pay promptly. Therefore, once you do talk to them, it’s important to use that time in the best way possible. There are three things to pay attention to when interacting with a debtor:

Instill a sense of urgency

Get the truth

Counter the excuse

Instilling A Sense Of Urgency

If your approach to getting paid is laid back and non-committal, your debtor will take this approach as well. When you communicate with late customers, you must demonstrate that the issue is urgent and important in order to get their attention and move them to action.

Getting The Truth

Sometimes the truth sounds like an excuse. Your debtors might be in real trouble or they might be tricking you. Asking the right questions will help you determine the facts and act accordingly.

Countering The Excuse

Once you’ve established you are hearing an excuse, you need to counter it in a way that makes sure you won’t need to deal with it again for this debtor.

Did you find this helpful? Download our free eBook “The Top 4 Excuses Debtors Make” and learn more about how to counter common excuses.

Collection operations base their high recovery rates on models allowing optimal utilization of collectors’ time. Since the person to person call is almost the only available too to convert debtors into paying customers, every minute is important. It’s obvious that self-service portals cannot bridge that gap on their own, because they won’t capture intent to pay in exactly the same way.

While we may never be able to move away from making phone calls, the user experience in the collection process can and should be adapted to use behavioral cues to capture payment intent. Thinking of the set of tools as a spectrum, with a high touch phone call on one end and a low touch self-service portal on the other, modern technology allows us to maintain contact with the customer more consistently and longer than before. The key, as discussed in the webinar embedded below, is in designing the experience to use the way we think to capture that intent.

In this webinar about behavioral economics in debt collection, we explore the mechanisms that drive decision in humans, and how to work with these mechanism to identify when a customer is ready to pay, or able and just needs a small nudge. These mechanisms are in the heart of every effective online experience, and they are explained here with their relevance to the debt collection process, with real life examples.

As of Q3-14, more than $6 Billion have been borrowed on Lending Club. The p2p lending platform allows individual investors to lend to consumers for various needs – most often, credit consolidation – and get a hefty interest in return. Most of the loans on Lending Club are paid back, but some of them don’t. We estimate that default rate at 5-7% overall, and naturally much higher when the loans are riskier. Borrowers pay their loans back via a monthly ACH payment, split and applied to all the notes that make up their loans, with the different lenders whose money they got. What happens when the note defaults? How do you see what happened? What is the Lending club debt collection process? Let’s take a look at the Lending Club interface and find out.

TrueAccord is a machine-learning and Al-driven 3rd-party debt collection company that is reinventing debt collection. We make debt collection empathetic and customer-focused and deliver a great user experience.

Our digital-first approach to debt collection creates a cycle of collections growth:

1. Improve the perception of the industry

2. Provide a personalized experience

3. Build brand equity and collect