Debt collection and account receivable departments often start with one person contacting late customers and evolve from there. Even third party collection agencies grow this way as they get more business. As a result, most collection departments are comprised of large teams of operators trying to negotiate with customers. Data science teams that are tasked with improving performance and profitability usually approach the task in one of two ways: process automation or agent-independent decision automation.

Process Automation is the effort to automate manual tasks done by collection agents, replacing them with an automated process or a self-service portal. This may mean skip tracing, logging payments, or queuing up phone numbers to call. The data science team acquires data sources or builds a process that replaces manual work with automated one, reducing the amount of time an agent spends per case. It’s about optimizing agent time on the phone, making sure that every action an agent takes is a high yield one, while busy work is replaced by some level of automation.

Decision automation means trying to teach a machine how to make the same quality of decision an agent makes in the collection process. For example: how to talk to debtors, what to tell them, how to respond to their issues. Because most agents have a hard time explaining in detail why they made one decision and not the other (they “just know”), often data science teams treat agents as an unreliable source of information. The team determines what they are trying to optimize – for example, right-party contact or the number of calls ending with a payment. They then build models that optimize these metrics, but without asking agents for feedback – only looking at long-term liquidation results.

While both approaches are important and are often used at TrueAccord as well, there’s a third one that often gets overlooked because data scientists and agents don’t interact often: Agent Dependent Decision Automation, or Expert Based Automation.

This study was sponsored by Castel, a provider of solutions to call centers; furthermore, the experts interviewed have built successful businesses using call center technology. Therefore the focus on call solutions makes sense. We also understand that the TCPA is vague, that consent is an issue and that consumer attorneys are putting compliance teams on edge. As a licensed agency, we’re in the same boat. However times are changing, and it’s high time that we embrace the change.

What technology solutions is the discussion raising? Mostly solutions to manually dial phone numbers, maybe a way to place a voice mail without a ring. The discussion offers little other options other than the iterated duo: those who don’t believe in technology, and those who deem it too risky.

The school of “technology won’t work”

The collection industry has been around for decades, and many of the businesses that comprise it were started long ago by “old school” collectors. That’s why the following quote didn’t surprise us.

“We’ve looked at technology like online chat interface,” said Christian Lehr with Healthcare Collections in Phoenix. “But we haven’t moved forward because it’s a business decision, not a compliance decision. I’m not sure it is the best way to serve the consumer. Much like with emails or text messages, it can be hard to understand context. And there is a time lag for communication. We may be able to serve the consumer faster on a phone call.”

As a company that uses machine learning to develop hybrid collection systems that collect better than call centers, we understand the sentiment but beg to differ. We also have the data to back this disagreement. Not only are email, text and website more effective for collections (from 30% better to 5 times better for low balance debts), consumers prefer them. More than 50% of TrueAccord’s traffic is from mobile devices; more than 35% of payments are made on a mobile device; 25% of interactions with our system happen in non-FDCPA hours. If this isn’t a “better way to service customers”, what is?

The school of “we need permission”

Collectors have been trained by regulators and lawyers to be very compliance minded. This makes them pessimistic about any new technology that hasn’t been tested by courts and lawyers. We hear a lot of the following from agency leaders.

“The only way we can move forward and success is to embrace technologies that are available to us,” Strausser said. “We should be looking at contemporary means of communication and exploring how to pull the trigger when and we are granted approval.”

We’d like to challenge this approach from two directions.

First, when thinking about texting and emails, compliance minded collectors are worried agents on the floor are going to abuse these new tools. However email and texts can be pre-written, optimized, and sent at exactly the right moment. They actually present a much stronger compliance framework when handled properly.

Second, collectors won’t adopt new technologies without explicit approval form the CFPB, but hold on to old call center technology even though the FTC clearly signals it’s all but forbidden. Is explicit approval, which the CFPB rarely provides, the thing to stop us – or can we have an honest analysis of the FDCPA to show us what reasonably can and cannot be done? Are we holding on to old and challenged technology due to inertia?

Bottom line: progress

There is much to do in debt collection. Consumer expectations, client requirements and regulatory pressure are mounting. The right thing to do is take a hard look at the old ways of doing business, and realize that the days of hiring to fight turnover and living off thin margins are almost over. Technology can help us service consumers at scale, provide great customer service, and get results that are better than anything we’d forecast based on old paradigms. We are excited to partner with some of the biggest financial institutions in investigating this possible future.

When we started working on our patented collection engine, Heartbeat, the industry told us: you’ll fail. Computers can’t collect. Humans do. The best you can do with automated communications is to drive inbound calls, so human collectors can “seal the deal”. Fast forward 18 months since our launch, and Heartbeat beats call-center based agencies in a growing number of segments. It turns out that computers collect debt pretty well. How come?

Debt collection is a numbers’ game. Consumers are ready and able to pay at different times, react to different stimuli, and need varying levels of support in the process. Teaching a machine to respond to these needs was historically more expensive than hiring humans, but as technology improves and compliance requirements grow, this is changing rapidly.

Humans are great at acting on intuition and responding to a changing situation. We act well based on partial information, guesses, slight changes in tone of voice and intonation. Good sales people do so without thinking. Humans are great at identifying and understanding corner cases and responding to complex inquiries. Machines can’t learn these things unless explicitly taught, and many of these skills are nuanced and complicated. Machines are “robotic”, for better and worse, and can’t have empathy.

Humans do have downsides, too. We are susceptible to biases. We make decisions based on the few past examples we remember and ones that fit what we believe. Collectors fixate on high balance accounts, worry about missing their goals, fight with their significant other and lose focus. Machines do not. Machines don’t forget a thing, and they always take as much data as available into consideration. Machines don’t talk back or get angry.

Historical attempts failedbecause they either tried to replace humans with even lower-paid humans, or tried to automate and get rid of humans altogether. We realized that a hybrid approach was the best one: machines make accurate decisions based on historical data when available, and learn from humans when not. Humans understand corner cases. We had to create a combination of a strong engine, and a team of experts to continuously improve it.

How does that work? When Hearbeat doesn’t “know’ what to do with a customer, it defers to our team of experts in San Francisco. They resolve the issue for the customer, and also give enough input so Heartbeat will know how to deal with the same situation in the future. The combination allows us to hit incredible productivity rates, while beating other “robotic” and passive “payment gateway” solutions.

Can machines collect? They can, and apparently many who are in debt prefer their targeted approach. When you think about the user experience, the ease of use and the automation, it’s actually not that surprising.

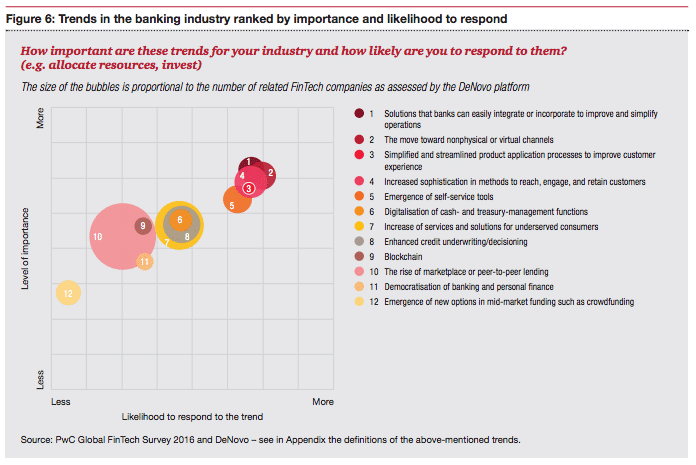

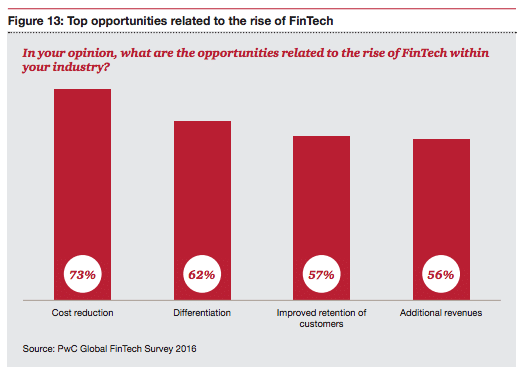

PWC just posted an interesting research (PDF) showing how Fintech firms influence financial institution from the outside in. We especially liked these two graphs:

More virtual channels, simpler products

“Banks are moving towards non-physical channels by implementing operational solutions and developing new methods to reach, engage and retain customers.” says PWC. We couldn’t agree more: the time for digitization has come, in debt collection as much as in any other part of the business (read more about eDisputes). As a result, banks are listening: “As they pursue a renewed digital customer experience, many are engaging in FinTech to provide customer experiences on a par with large tech companies and innovative start-ups.”

Top Fintech opportunities: cost reduction and differentiation

“B2B FinTech companies create real opportunities for incumbents to improve their traditional offerings”, says PWC, “incumbents could simplify and rationalise their core processes, services and products, and consequently reduce inefficiencies in their operations.” We see that in the marketplace: technology and automation help us scale (read more about 30,000 cases per agent) but it also helps us provide personalized, tailored treatment to consumers. As a result, lenders that work with us see better results (through complex recovery strategies), better customer satisfaction, and increased compliance.

Bottom line

Banks are leaders of the Fintech community. Often they are reluctant to adopt a trend until it visibly gains traction, but once they do, their scale draws attention from all participants. It’s 2016, and banks have noticed Fintech and the upside it brings with it. It’s going to be a fascinating year!

Tasked with creating a collection strategy? Fighting to reinvent your collection funnel or turn around a failing operation? It’s time to harness technology to get ahead. 21st century technology has arrived, and digital collections are here for you.

This 28 page book includes:

Collection strategy 101: for the uninitiated – learn the basics

The pitfalls in common collection strategies – how legacy forces constraints

Using technology to get superior results – how machine learning and digital collections can help you blog through your goals

Learn from our experience working with dozens of companies from various segments and different stages, and with hundreds of thousands of customers in debt. Download the free eBook here.

Already interested in digital collection and how they can enhance your strategy? Worried about upcoming changes in debt collection rules and how you’d adapt to them? You’ve come to the right place. Check out our website and talk to our experts about what we could do for you.

Are you a member of the California Bar, or just interested in ethics in debt collection? Join and hear a talk by our General Counsel, Avital Gertner-Samet.

Date and Time: January 21, 2016, 11:45 a.m. to 1:00 p.m.

Committee secretary Avital Samet, General Counsel at TrueAccord, will lead the presentation covering potential ethical conflicts to be aware of and avoid while practicing debt collection law. The attorney’s loyalty and confidentiality duties to his client will be juxtaposed against the attorney’s duty as an officer of the court and duties owed to the consumer. These aspects are relevant both to third party and first party debt collectors as well as to counsels that advise to creditors and consumers alike.She will be joined by Matt Loker (Kazerouni Law Group, APC) and Jeffrey Ehrlich (Consumer Financial Protection Bureau).

To attend, please use the following dial-in number at 11:45 a.m.

The online lending space is experiencing tremendous interest, leading to explosive growth and an influx of capital. Many companies grow overnight, raise big rounds of venture capital; vying for a piece of an increasingly competitive market. While top-line growth and customer acquisitions are top of mind for new and existing players, the increase of competition puts a lot of pressure on margins. When focus moves to profitability and unit economics, reducing defaults has a significant impact. After optimizing underwriting criteria, many lenders turn to optimizing collection and recovery strategy.

Now, there is a limited set of tools available to collection strategists, especially considering it’s a service that’s been around for millennia. Traditionally, companies collect in-house, outsource to an agency, sue debtors, or sell their debt (or any combination of the above). Are these tools efficient? Which ones are best? And specifically – should new lenders sell their debt?

Happy to see our name on Forbes’ Fintech 50, recognizing industry leaders. As Forbes puts it, “Digital disruption is going to soon affect every aspect of your money: how you earn it, save it, invest it and spend it.”

Hiring collectors is one of the biggest challenges in collections and recoveries. Most collection processes are manual and require extensive training: the low, commission based salaries and the adversarial nature of the job lends itself to high turnover. Once agents are trained and working, collection managers must keep them up-to-date on debt collection regulations, as well as implement quality controls. One ill-trained agent’s compliance violations can put an operation at risk due to the many regulations that govern the US collection and recovery process. This results in a big investment in human resources. It’s no surprise this is one of the biggest line items for any collection operation. Beyond payroll and training, turnover results in low morale, often hurting organizational cohesion. Continue reading “Stop the hiring craze: How TrueAccord reached 30,000 cases handled per agent”→

TrueAccord is a machine-learning and Al-driven 3rd-party debt collection company that is reinventing debt collection. We make debt collection empathetic and customer-focused and deliver a great user experience.

Our digital-first approach to debt collection creates a cycle of collections growth:

1. Improve the perception of the industry

2. Provide a personalized experience

3. Build brand equity and collect