After three decades of providing exceptional customer experience, a leading national bank recognized a lot has changed in the world of personal banking, technology, compliance, and, in turn, debt collection. To continue delivering the level of service their customers expect meant it was time for the bank to update their recovery methods for the new digital age.

Although the bank had seen moderate success in late-stage collections with their call-and-collect vendor, they had a list of goals that they were unsure their existing collection provider could achieve:

Improve and increase liquidation performance

Keep up with new regulations and ensure compliance

Leverage new, more cost-effective solution

But what was the best way to evaluate the effectiveness of new digital-first engagement versus their existing outbound calling approach?

To test and measure the success of each distinct debt recovery method, the bank decided to use the Champion-Challenger model with TrueAccord joining their existing collections partner.

For their Champion-Challenger test, the bank assigned TrueAccord 50% of primary placements and tertiary placements against their traditional collection provider. By using scorecards, the bank was able to compare the two using set collection goals (varying by month and season) and several key performance indicators (KPIs), including:

Overall liquidation rates

Percentage of settlements in full

Percentage over/under set collection goals

With the Champion-Challenger model in place, collection goals and KPIs designated, and scorecards set, it was time to see how TrueAccord’s digital engagement methods would measure up compared to the old school call-and-collect method…and the numbers would speak for themselves.

If your business plans to use outbound calling as the main mode of engaging past-due customers in 2024…good luck.

Good luck reaching the right number for the target customer. Good luck getting them to commit to repayment over the phone. Good luck not getting complaints.

And if the plan is only to use outbound calling…be prepared to start accepting more losses in 2024. Even if you can get the right customer on the phone, studies show 49.5% of consumers take no action after a collection call.

Let’s look at the challenges around right-party contact rates, consumer complaints, and the timely factors that make the challenges more detrimental to your business’s late-stage debt recovery.

Declining RPC Rates

The decline of right-party contact rates (RPC)—the percentage of calls in which an agent is able to connect with the target consumer—isn’t new for 2024, but its impact on debt collection is reaching new heights in the new year. RPC is considered one of the most accurate measurements for the effectiveness of an organization’s outbound calling efforts, whether internally or through a third party.

Surveys from the Association of Credit and Collections Professionals (ACA International) found that 62% of the respondents reported seeing a decrease in right-party contacts, with 78% of the respondents experiencing call-blocking and 74% having their calls mislabeled.

Call-blocking and spam-mislabeling are only part of the issue for RPC rates: government regulations, robocalls, lack of consumer trust in answering calls, and inaccurate phone data all contribute to the drop in RPC rates.

The bottom line is the declining RPC rates are negatively affecting your business’s bottom line—but that’s not the only challenge outbound dialing for debt collection faces in 2024.

Rising Consumer Complaints

As almost all other forms of financial transactions have evolved, so have consumers’ communication preferences in that arena. Nearly nine in ten Americans are now using some form of digital payments and 59.5% of consumers prefer email as their first choice for communication, but traditional call-and-collect methods still dominate in late-stage recovery efforts.

And with that in mind, it shouldn’t be surprising that consumers complain about debt collectors’ and creditors’ communication tactics used when collecting debts.

But beyond ignoring communication preferences, many consumer complaints actually equate to compliance violations.

According to the 2022 Annual Report on the Fair Debt Collection Practices Act (FDCPA), 51% of communication-related complaints were because of repeated calls. Despite the 7-in-7 Rule (debt collectors are prohibited from calling the same consumer more than seven times within seven consecutive days, unless the consumer directly gives consent to receive any additional calls), 17% of respondents of a Consumer Financial Protection Bureau (CFPB) survey said a creditor or debt collector tried contacting them eight or more times per week. Similarly, other common complaints revolve around the collector or creditor calling at inconvenient hours outside of the FDCPA presumed convenient calling hours from 8:00 a.m. to 9:00 p.m. at the consumer’s location.

But again, even if you are following the letter of the law, it doesn’t protect your brand’s reputation from consumer complaints.

Minimize These Collection Challenges with a Digital-First Approach

Between declining RPC rates, shifting consumer preferences, rising consumer complaints, and increasingly stricter compliance regulations, the once tried-and-true outbound calling methods are no longer viable in 2024.

But your business doesn’t have to resign to accepting losses once accounts hit late-stage delinquency—taking a digital-first approach negates concerns over RPC rates, catches up with evolving consumer preferences, neutralizes the cause of common consumer complaints, and smoothly navigates compliance requirements.

It’s hard to believe that the year is already winding down, but consumer debt certainly isn’t. And not having the right collection partner today can equate to missed recovery opportunities tomorrow.

So what makes the end of the year such an important time to evaluate your current collections partner? Let’s take a look at some of the timely factors.

Why Evaluate Your Collection Partner in Q4? To be Better Prepared for 2024

Be Ready for the Aftermath of Holiday Spending

It should come as no surprise that consumer spending typically increases in the last few months of the year—Black Friday, Cyber Monday, Super Saturday, Boxing Day, not to mention the expenses around holiday travel too.

But last year marked a particular surge in consumers putting a lot of that spending on credit, with 41% of Americans putting more than 90% of their holiday expenses on their credit cards, and one-third using credit cards for all their holiday expenses.

With this heavy reliance on credit, nearly 42% anticipate going into debt to pay for the holidays—especially when considering that US shoppers took on over $1,500 in holiday debt in 2022.

It feels almost inevitable that by the end of Q1 in 2024 some consumers will already be rolling over past the 90-day delinquency mark. To be ready, your debt collection should be preparing for Q1 late-stage collections now.

Get a Jump on Engagement Before Tax Season

Even though tax season may feel far off today, now is the time to start preparing engagement strategies to reach and remind consumers to prioritize repayments when tax refunds come around.

And this shouldn’t be a novel concept to customers already dealing with debt: surveys find one in five respondents intend to pay off their holiday spending bills with federal tax refunds. In 2023, 44% of Americans reported earmarking their refunds to pay off their debt overall, according to the CNBC Your Money Financial Confidence Survey.

Although paying off debt is a priority, 34% of those surveyed said they were worried their refunds wouldn’t make as big of an impact due to inflation/rising costs while still reporting that their tax refund would be critical to their household finances—don’t let your collection partner show up late to the competition when consumers are allocating those tax refund dollars.

Bottom line: many consumers will likely fall into debt in Q4 due to holiday expenses, but being prepared to engage them come tax season can help influence opportunities to secure repayment as we roll into 2024.

Why Opt for Digital Outreach? To Meet Consumers Where They Already Are

Your collection partner needs to be prepared for when and where your customers are ready to engage. And after the holidays and gearing up for tax season, many consumers are already active online—so don’t miss the chance to engage them through digital outreach.

By the numbers, consumers are primed for digital communications in Q4 and Q1 considering:

In 2022 online holiday sales rose 3.5% year over year, marking the largest ever online holiday season

68% of Americans report they pay more attention to emails from companies during the holidays

93.8% of individual tax returns were filed electronically

Convenience was one of the top six reasons Americans prefer filing taxes online

Given that consumers will be spending a lot of time online through Q4 and into Q1, digital communications is crucial to stay top of mind as holiday spending rolls into delinquency and competition for tax refund dollars ramps up. Your collection strategy should not only include email but also be ready with the right message at the right time to secure repayment—it takes more than just generic mass blast emails to get consumers to engage.

Does your collection partner have a plan to capture delinquent customers’ attention at just the right time with the right message? And not just looking ahead for Q1 engagement, but all year round.

Consumers Prefer Digital for Financial Services—Any Time of Year

While we see spikes in online shopping during the holiday season and more consumers choose to file taxes electronically, these aren’t the only times of year that financial transactions happen digitally.

During any given month, surveys find that 73% of people worldwide turn to online banking at least once a month, with 59% specifically using mobile banking apps. This marks an increasing adoption rate of digital channels by customers to get their banking done, jumping to 83% in 2023 up from 77% in 2020.

Globally, the number of online banking users is expected to reach 3.6 billion by 2024.

Overall, consumers are opting for a digital experience when it comes to their finances, so using digital channels needs to be an integral part of your collection strategy year-round when you consider:

59.5% of consumers prefer email as their first choice for communication

Contacting first through a customer’s preferred channel can lead to a more than 10% increase in payments

14% of bill-payers prioritize payments to billers that offer lower-friction payment experiences

Is your collection partner set to deliver personalized digital communications at scale any time of year?

How to Evaluate a Debt Collection Partner

Selecting a debt collection partner makes an impact regardless of season, but Q4 offers businesses the opportunity to set their recovery efforts up for better success leading into tax season.

But what are the questions to ask and qualities to look for in a partner? Whether your business is looking to work with a collection agency for the first time or want to reassess how effective your current provider may actually be, our latest eBook provides the Top 10 Questions to Ask along with explanations of why each specific question matters and what to look for when evaluating—available for download here»»

The goal of a recovery operation is to maximize profitability by efficiently recovering money lent to consumers—while maintaining consumer loyalty. This means that measuring the success of a recovery strategy goes beyond just dollars and cents and into consumer-centric metrics as well.

But how do teams measure overall portfolio performance, and what are the most important portfolio-level key performance metrics (KPIs)? Let’s take a look at a few of the top KPIs and how they can be categorized.

Key Collections Metrics

Key performance indicators for debt collection and recovery efforts:

Accounts per Employee (APE) or Accounts to Creditor Ratio (ACR): the number of delinquent accounts that can be serviced by an individual recovery agent

Net Loss Rate or Net Charge Off Rate: measures the total percent of dollars loaned that ended up getting written off as a loss

Delinquency Rate: total dollars that are in delinquency (starting as soon as a borrower misses a payment on a loan) as a percentage of total outstanding loans – often an early warning sign on the total volume of delinquent debt

Promise to Pay Rate: the percentage of delinquent accounts that make a verbal or digital commitment to pay

Promise to Pay Kept Rate: the percentage of delinquent accounts that maintain a stated commitment to pay

Roll Rate: the percentage of delinquent dollars that “roll” from one delinquency bucket to the next over a given period of time – provides visibility into the velocity with which debts are heading into charge off

Metrics like net loss rate are the north star of a recovery program, while metrics like delinquency rate and roll rate are leading indicators of future portfolio performance. But just as critical as these traditional KPIs, today’s collection operations need to focus on implementing and measuring digital engagement.

Digital Engagement Metrics

A range of KPIs that capture how effectively digital channels are reaching and engaging consumers:

Coverage: the percentage of users for whom we have digital contact information

Deliverability: the percentage of digital messages that are actually reaching consumers

Digital Opt-In: the percentage of users who have consented to receive digital communications in a particular channel

Open Rate, Clickthrough Rate: the percentage of users who are actually opening and clicking digital communications

Following key collection and digital engagement metrics are all well and good, but how do recovery teams move the needle on those critical KPIs?

Operational metrics are the KPIs that collectively drive overall portfolio-level performance. They represent the “levers” available to change the economics of a recovery model.

Operational Metrics

Metrics that create simple framework to explain the profitability of a recovery operation:

Profitability of a Collections Operation Formula: R x ResF x E

R [Reach]: percentage of consumers in delinquency can you actually reach

ResF [Resolution Funnel]: how effectively you can convert initial contact with a consumer into a commitment to pay – and ultimately, a payment promise kept (see Promise to Pay Rate and Promise to Pay Kept Rate)

E [Efficiency]: calculation of what the “unit economics” of your collection are and how much it costs, on average, for every account that you rehabilitate

In the hyper-competitive financial services space, consumer experience is a source of competitive advantage. That’s why it stands to reason that alongside the “traditional” metrics of recovery economics, forward-looking businesses have pioneered a new set of KPIs that measure the value of consumer experience.

Consumer-Centric Metrics

A new set of KPIs that measure the value of consumer experience:

Net Promoter Score (NPS): how likely a consumer is to recommend a given brand after an experience with a brand’s collection organization

Customer Retention Rate: how likely a consumer is to be reacquired by a given brand after his or her delinquent account is rehabilitated

Keep a Close Watch on These KPIs for Collection

As payment-driven organizations across verticals focus further into the world of recovery, it is safe to anticipate that digital engagement and consumer-centric KPIs like the ones we covered above will become even more deeply woven into the fabric of the organization.

If your business and collection partners aren’t utilizing email in your debt recovery strategy, you’re leaving vital engagement opportunities (and potential collections) on the table. There are plenty of reasons why digital communications are the way to go, but reaching out through email is especially important in collections.

Surveys show that 59.5% of consumers prefer email as their first choice for communication, and 14% of bill-payers prioritize payments that offer lower-friction payment experiences, which increases to 23% for millennials specifically. Considering this, it shouldn’t come as a surprise that courts have actually ruled that “an email is less intrusive than a phone call” for debt collection.

But what makes a successful email program when it comes to connecting with delinquent accounts? Whether your business is handling collections in-house or are looking at working with a third party, your operations should be confident that you have these core components covered.

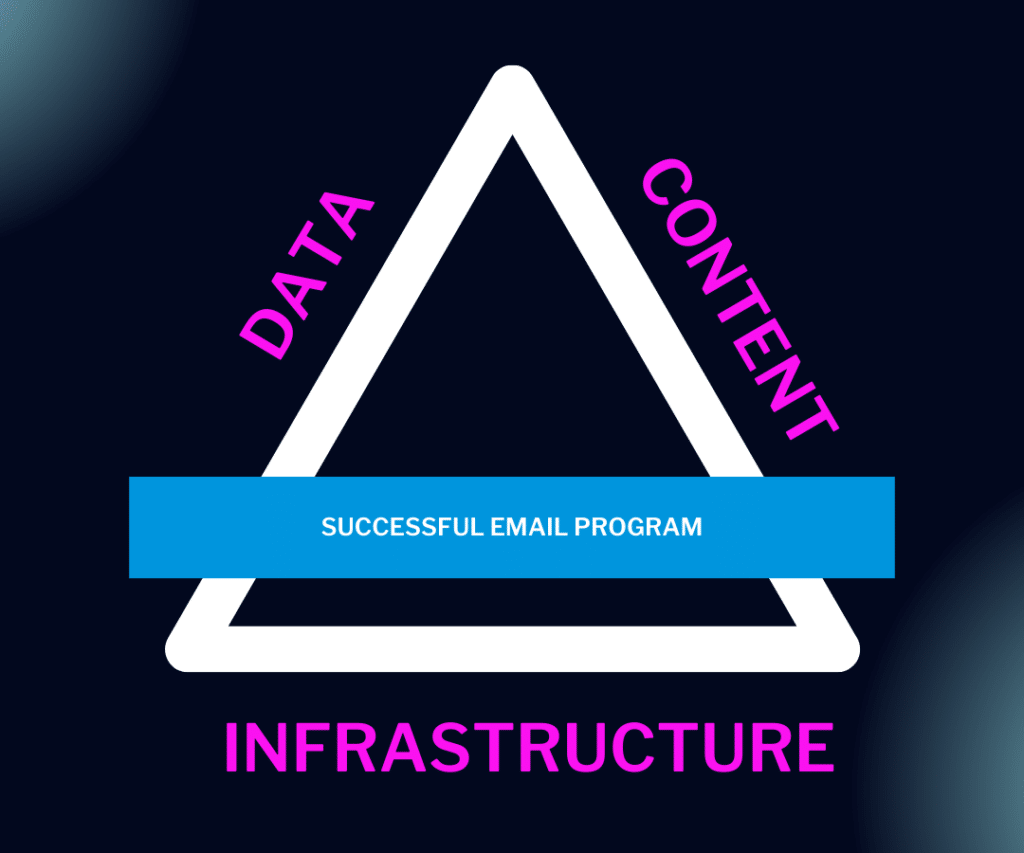

Core Components for a Successful Email Program

While adding email into the communication channel mix is critical, it is the set up, execution, and continued optimization of that email program that can actually make a difference when it comes to consumer engagement. There are many elements to a successful email strategy, but here are three of the core components that we’ll focus on:

Infrastructure, Data, and Content

All 3 are required for a successful email program—each one relies on the other two to create a high performing program.

Let’s take a look at why each of these is important and the risks that can occur without each component in place.

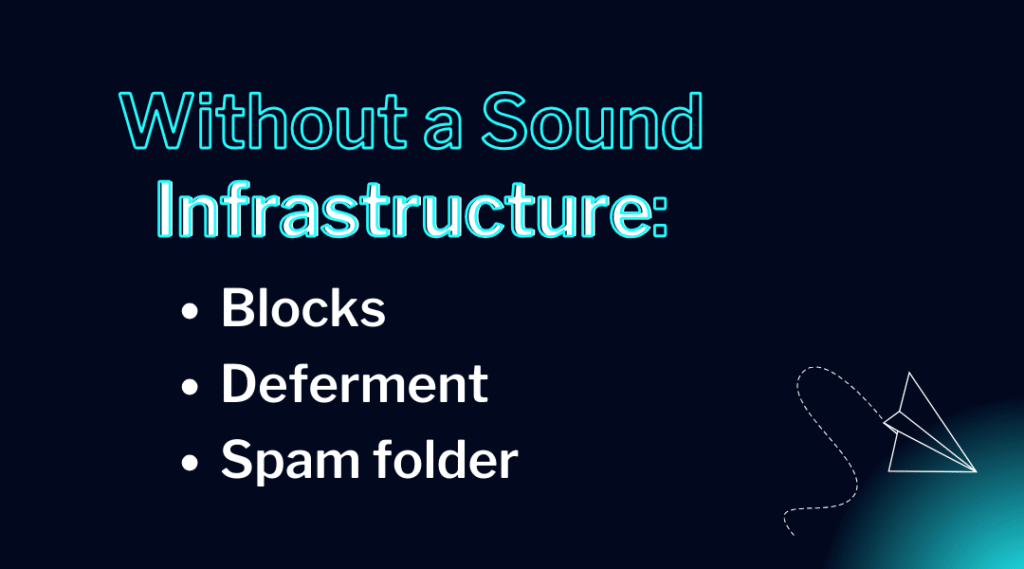

INFRASTRUCTURE

The infrastructure an email program is built on has many components itself: Mail Servers, Mailbox Providers, Internet Service Providers (ISPs), Email service providers (ESPs), and more. How these components are set up and work together influences sender reputation, which in turn influences email delivery rates. You can learn more about these different pieces in our blog focusing on the The (Hidden) Anatomy of Emailhere»»

While infrastructure can admittedly be complex, the risks your operation runs without a sound infrastructure are clear and quite consequential, including having your emails blocked, deferred or delayed delivery, or winding up lost in the recipient’s spam folder.

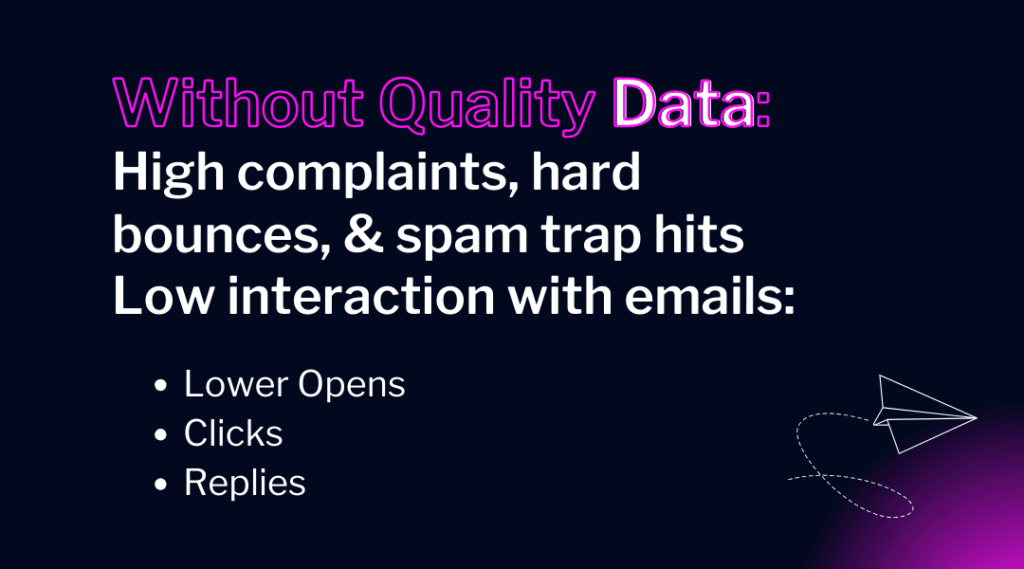

DATA

In today’s digital world, data is everywhere—but how you harness that data can make or break your email program (and even get you into hot water if you or your collections partner are not following all the necessary compliance regulations around data privacy and protection). Understanding data helps intelligently influence an email program, especially when focusing on email engagement metrics such as:

Opens

Clicks

Unsubscribes

Spam complaints

Hard Bounces

Spam traps

But without quality data analyzed appropriately, your emails could result in consumer complaints, hard bounces, falling into spam traps, not to mention negatively impacting all the engagement metrics listed above.

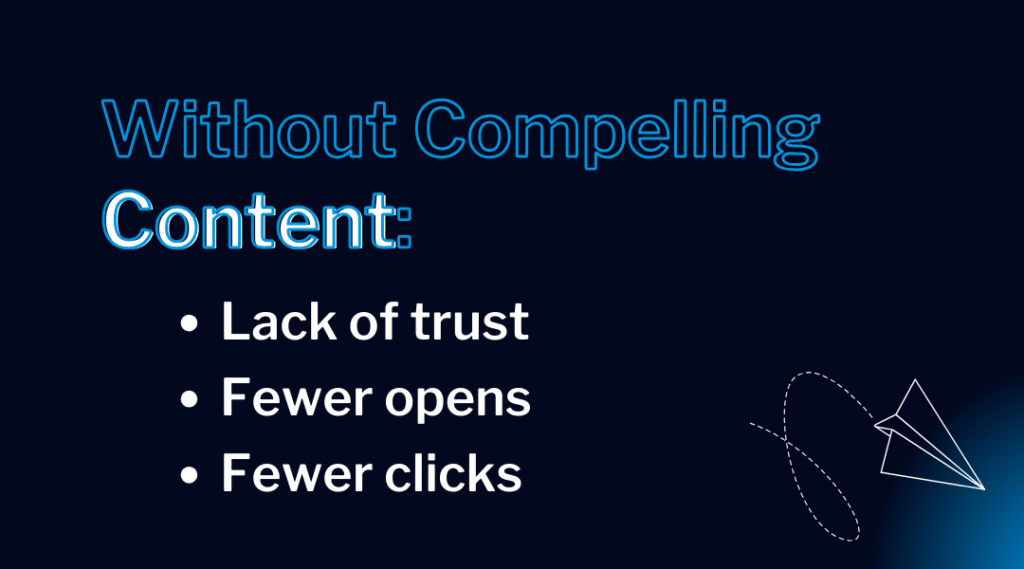

CONTENT

Solid infrastructure and reliable data are essential in any email program, but when it comes to debt collection, content can be the tipping point between a consumer committing to repayment or ignoring the outreach altogether—or even reporting your communications as spam or harassment.

From subject lines to your call-to-action (CTAs), sending the right message to your customers is crucial. Without compelling content you miss opportunities to capture consumers attention resulting in fewer opens, fewer clicks, or even pushing consumer perception in the wrong direction. If you lose your customers’ trust, you’re most likely going to lose the chance to recover their debt.

Successful Email Engagement Can Boost Debt Recovery

Studies have shown that engaging consumers through digital methods can increase resolution rates by as much as 25%. But if your digital efforts are missing any of the core components we just covered above, it doesn’t matter if your collection strategy includes email—your operations are going to be missing recovery opportunities.

In today’s financial landscape, regulators at both the federal and state level are driving accountability for companies when it comes to data protection and security. We see that with the express requirement in the Gramm-Leach-Bliley Act, or GLBA, Safeguards Rule—which went into effect on June 9, 2023—that organizations have one qualified individual to oversee the information security program, and that the qualified individual provides regular reports to the highest governing body of an organization. This underscores the importance of protecting customer information in a digital age where information has its own intrinsic value.

Let’s take a look at how the new updates to GLBA Safeguards Rule, how these security policies are important specifically for debt collection, and what best practices your business should follow to protect consumers’ data.

The GLBA Data Protection Law

The Gramm-Leach-Bliley Act, or GLBA, is a federal regulation to control how financial institutions collect, store, and transmit consumer information. GLBA was enacted by the Federal Trade Commission (FTC) in 1999 and recently rolled out new amendments to the Standards for Safeguarding Customer Information, known as the “Safeguards Rule,” that went into effect on June 9, 2023, in effort to continue protecting consumer data in an ever-evolving digital environment.

A few of the updates to GLBA’s Safeguards Rule include:

Provides covered financial institutions with more guidance on how to develop and implement specific aspects of an overall information security program

Improves the accountability of these security programs, such as requiring financial institutions to designate a qualified individual responsible for overseeing, implementing and enforcing the program

Data Protection is Critical in Debt Collection

To attract clients today a debt collector must demonstrate the implementation of a full suite of information security practices covering physical, technical, and administrative safeguards, including a comprehensive employee information security training. Failure to implement these best practices can result in a security incident or worse, a data breach. Not only are data breaches costly because of the notification provisions, including providing credit bureau monitoring, it can be difficult for a company to survive after a breach. It is not unusual for a company to file bankruptcy after a data breach.

Reputation and Customer Retention

Although complying with federal and state regulations helps companies avoid costly—even criminal—penalties, consumer trust that their financial data is being protected is critical to maintaining a positive reputation and retaining customers (even if they fall into delinquency).

Data protection policies can often be treated as a set-it-and-forget-it, or even treated as a luxury of lower priority due to limited resources, expertise, or familiarity. But for today’s consumers, data security is a top priority.

A recent study by MAGNA Media Trials and Ketch, showed across every age group74% of people rank data privacy as one of their top values—consistently rank data privacy as their top concern. And on the flip-side, the study showed nearly 9 out of 10 consumers report strong data privacy practices positively impact their relationship with a company.

Keeping Up With Compliance

Along with federal regulations, individual states are also issuing new laws focused on consumer data protection. California, Utah, Colorado, Connecticut and Virginia all passed data privacy laws over the past several years that take effect in 2023. This past March, Iowa passed a Data Privacy Law that takes effect on January 1, 2025 that is very similar to both Virginia and Colorado’s laws affording consumers a right to know and right to request deletion. Pennsylvania amended its Breach of Personal Information Notification Act, by among other things, expanding the definition of “personal information” to include medical and health information, and a username or e-mail address in combination login credentials. Several more states have draft privacy and security laws in draft.

Although GLBA and other data protection and privacy laws are the hot topic when it comes to compliance today, it isn’t the only federal privacy regulations lenders and debt collectors need to follow and monitor for changes—or face the consequences of non-compliance. Here are some recent laws and amendments impacting the industry:

The Fair Credit Reporting Act: Credit reporting companies and users of credit reports have specific obligations to protect the public’s data privacy, with potential criminal liability for certain misconduct.

Health Insurance Portability and Accountability Act (HIPAA): Two part rule for privacy and security of personal health information that applies to covered entities (doctors, hospitals, pharmacies, insurers, and their vendors). PHI – is defined broadly to include any information provided to the covered entity by the patient.

Consumer Data Protection is Not a Luxury

Having good security practices in place is not only beneficial for both consumers and businesses, but also critical to stay compliant with all the new laws and amendments being introduced. Here are some of the best privacy and security practices to implement to protect customers, companies, and stay compliant:

Practice data minimization.

Know where personal information lives at all times by creating a data map of where the data goes and is stored throughout your systems, which includes knowing your vendor’s data security and privacy practices and controls.

Know who has access to personal information and routinely examine if that access is necessary to complete that job function.

Be intentional with how data is organized and stored so it can be easily segmented and treated differently if need be (think network segmentation).

Have a public facing Privacy Notice–and make sure it accurately reflects your practices for use, collection, deletion and correction.

Conduct an annual data security risk assessment to continually reassess areas for improvement and where you may need additional controls.

Ensure contracts with parties whom you receive and/or give personal information to specifically address each parties’ obligations and restrictions for how personal information is used, shared, disclosed, stored, and sold (if permitted).

The TrueAccord Approach

At TrueAccord, empathy towards the consumer is a core part of our company mission: we enable businesses to collect more, faster, and from happier customers.

Ready to collect more, faster from happier customers? Learn how TrueAccord weaves compliance and data security into debt recovery by scheduling a consultation today»»

Outbound calling has been the main mode of collections for decades, but the cost of a call center or in-house full-time employees (FTEs) making calls is no longer justifiable when most consumers simply don’t answer the phone, on top of the mounting compliance restrictions limiting opportunities to call in the first place.

But outbound dialing isn’t completely obsolete—digital-first omnichannel strategies can turn traditional call-and-collect operations around by integrating new digital channels into the communication mix.

Let’s compare traditional outbound calling methods versus a digital-first approach in three key areas impacting your business’s ability to collect more, faster:

COST

COMPLIANCE

CONSUMER PREFERENCES

Get even more statistics and data in our latest eBook — Why Evolve from Outbound Calling to Omnichannel Engagement? Cost, Compliance, & Consumer Preferences — available for download now»»

COST: Call-and-Collect

The cost to collect has been on the rise for traditional methods for years, whether you outsource to a call center or have FTEs dialing the phones.

One reason for this rise is based on the fact that many lenders still practice old strategies to prioritize contacting customers based on their risk profiles, balance, and average days delinquent—completely missing portions of their portfolios. Factoring in propensity to pay is important to successful engagement, but it means that agents’ time is focused on only a small portion of accounts, leaving potential repayments on the table.

Add in the overhead costs, inflation, and hiring challenges of using agents as first attempts at engagement and watch the expenses continue to climb past what you’re able to collect through outbound calling.

COST: Digital-First Omnichannel

Right off the bat, digital-first shows the cost of collections can fall by at least 15%.

Since digital is infinitely scalable, this communication tactic can touch every single account, regardless of scoring models—unlike human dialers who can only physically call a certain number of accounts on any given day. Going digital-first cuts down on the time billed for making repeated outbound calls that are never answered or returned, and it allows agents to interact with customers that want to speak directly to a person.

Overall, digital-first has shown to boost customer engagement by 5x, the first step towards repayment.

COMPLIANCE: Call-and-Collect

It’s no secret that it’s increasingly complicated to reach customers with all the legal communication restrictions.

While all debt collection communication is subject to compliance rules, outbound calling has specific laws and regulations that can carry costly penalties for non-compliance—and it’s only becoming more complex with new state-specific rules rolling out right and left. But no matter where your business is doing business, if you’re making collection calls you must follow these federal guidelines:

Inconvenient Time Rule: prohibits calling before 8am or after 9pm

Regulation F’s 7 and 7 Rule: Cannot call more than seven times within a seven-day period

Telephone Robocall Abuse Criminal Enforcement and Deterrence Act (TRACED Act) tagging legitimate businesses as spam

FCC Orders further restrict dialing to landlines and include opt-out requirements for prerecorded voice messages

But there is a more streamlined way to ensure your collection communications are following all the rules: enter code-based compliance.

COMPLIANCE: Digital-First Omnichannel

Code-based compliance works by programing rules that ensure all communications fall within all federal and state laws and regulations, such as:

Frequency and harassment restrictions

Consent requirements*

Disclosure requirements

This digitally designed approach to compliance greatly reduces the opportunities for human error that are bound to occur in more manual processes. Additionally, the digital-first approach allows companies to continue to collect during times that calling would violate certain regulations, like the Inconvenient Time Rule. In fact, 25% of payments come in after 9pm or before 8am (the determined inconvenient times), since these hours can actually be more convenient for consumers to catch-up on digital communications they received throughout the workday.

*Generally, there is no requirement in the federal law to send debt collection communications by email, though some states are more restrictive. This is not legal advice, please consult an attorney for guidance on your unique circumstance.

CONSUMER PREFERENCE: Call-and-Collect

46% of consumers want to be reached through their preferred channels—so what are today’s consumers’ preferences?

Here’s a hint: phone calls aren’t at the top of the list.

And today’s Right Party Contact rates show it, ranging between just 0.5% – 4.0%. And out of those that do answer the phone, 49.5% of consumers take no action after a collection call. The old call-and-collect tactic may actually do more harm than good if compliance rules are ignored: out of the communication tactic complaints received by the CFPB in 2020, over half complained of frequent or repeated calls.

CONSUMER PREFERENCE: Digital-First Omnichannel

So if phone calls aren’t consumers’ preferred method of communication, then what is? For 59.5% of consumers, email is their first preference when it comes to debt collection communications. This is especially important considering that first contacting a customer through their preferred channel can lead to a more than 10% increase in payments.

This digital preference isn’t surprising since nearly nine in ten Americans are now using some form of digital payments—why would they expect collections to be any different? 14% of bill-payers prioritize payments to billers that offer lower-friction payment experiences, and digital is often preferred because of it. Digital communications are easily controlled by consumers and are tightly managed by service providers with built in mechanisms to prevent harassment (like with code-based compliance), which we know has historically been a challenge for call-and-collect practitioners.

Digital-First is the Future of Collections

And it’s here today, working for TrueAccord clients and customers.

At TrueAccord, we find that more than 96% of customers resolve debts without any human interaction when digital options are offered—reducing costs associated with outbound calling, lowering risks with code-based compliance built in, and delivering an experience that consumers prefer.

Get even more statistics and data in our latest eBook — Why Evolve from Outbound Calling to Omnichannel Engagement? Cost, Compliance, & Consumer Preferences — available for download now»»

Reaching consumers can feel harder than ever these days, so struggling to engage delinquent customers can leave some businesses ready to accept losses as just another “cost of doing business.” With 75% of Americans reporting that they will never answer calls from unknown numbers, even the most targeted scoring model for calling has low chances of recovering funds.

But the omnichannel approach—utilizing a combination of calling, emailing, text messaging, and even self-serve online portals—is the preferred experience for 9 out of 10 customers, according to a study conducted by UC Today. And it’s not just beneficial for consumers. The omnichannel approach has been shown to increase payment arrangements by as much as 40%!

So integrating an intelligent digital communication strategy with traditional call-and-collect or letters sounds like a smart plan, but why is it more important now than ever before?

Let’s look at why today’s economic landscape makes omnichannel engagement critical for collections and how your business can get there.

Delinquencies are Rising—And Call Centers Can’t Keep Up

The first quarter of the year revealed that Americans have almost reached $1 trillion in credit card debt, breaking a record set in 2019. Fueled by inflation and higher interest rates among other economic factors, some card issuers’ charge-off and delinquency rates are also rising back up to their pre-pandemic levels.

So we know that delinquencies are on the rise in addition to new compliance regulations that have put greater restrictions on calling (such as the inconvenient times rule, 7-in-7 rule, among others), which put greater limitations on the reach call centers can actually have. Even using scoring models to focus on those who have the highest propensity to pay, consumer preferences have moved away from engaging through (or even answering) the phone.

Even if you know which delinquent accounts are primed for repayment, old school methods will never be able to reach them all efficiently in comparison to digital engagement.

On top of that, consumers are typically already carrying out financial transactions online—so why would a business expect their preferences to shift offline when it comes to handling another financial interaction? When a customer defaults on their account, it is a disruption to their lives to suddenly receive phone calls and letters regarding an account for which they previously only communicated via digital channels.

From our own experience, many of TrueAccord’s creditor-clients prefer a seamless transition to debt collection, and will even go so far as to prohibit TrueAccord from making any outbound calls or sending letters on their accounts because their customers have only ever interacted digitally.

It can even stifle the flow of information that helps consumers make informed decisions about their finances. According to the Pew Research Center, “reliance on smartphones for online access is especially common among younger adults, lower-income Americans and those with a high school education or less.” In fact, 87% of TrueAccord consumers visit our web portal from their mobile devices and tablets, not their desktop computers. Choosing not to engage via digital methods can hurt vulnerable populations of consumers who primarily conduct most of their affairs digitally.

But the answer to this challenge isn’t going 100% all-in on digital communications necessarily. There’s a better way to reach past-due customers and collect more, faster (and from happier people).

Enter the Omnichannel Approach

We’ve seen that call-and-collect operations have proven less successful over time, even using propensity to pay scoring models, but there is a time and a place for those traditional methods in an omnichannel strategy. Adding different technologies to your debt collection operation like email, SMS, and even self-serve online portals can actually enhance the hard work your call centers are already doing and make it overall more effective.

Why is the use of different channels—and more importantly a customer’s preferred channel—so critical for today’s debt collection efforts? The numbers speak for themselves:

46% of consumers expect to communicate through preferred channels

Initiating contact with delinquent customers through their preferred channels can lead to a more than 10% increase in payments

Some banks have found digital communication channels can increase payment rates of customers in late delinquency by 30%

Lenders that have implemented digital-first solutions have seen their cost of collections fall by at least 15%

Traditional outreach methods like outbound calling elicited 18% fewer responses from customers with accounts 30 days past due who prefer digital communications.

The key takeaways from these studies go beyond just “going digital”—to see improvements in engagement rates, repayments, and operational costs you must communicate through the consumer’s preferred channels.

At TrueAccord, we’ve seen this approach’s success time and time again for our own clients and their customers.

Statistics and Stories from the TrueAccord Omnichannel Strategy

Almost all TrueAccord communications with consumers (93%) happen electronically with no agent interaction. The remaining 7% of consumers who do interact with an agent, send an inbound email or make a phone call to our inbound call center where any of our customer care agents are prepared to assist with their request. This is a more cost-effective and efficient use of agents’ time versus making outbound calls, which benefits both businesses and their customers, as one consumer told us on June 1, 2022:

“Thank you for not calling a million times and texting me and allowing me to pay this when I could.”

As described above, TrueAccord primarily sends digital communications to help consumers navigate and take actions at their convenience online, as this consumer told us on January 18, 2023:

“I like how you explain everything in detail by email and easy payment plans for people to regain their credit scores and to get back on their feet.”

In fact, more than 21% of consumers resolve their accounts outside of typical business hours (before 8am and after 9pm) when it is presumed inconvenient to contact consumers under the federal Fair Debt Collection Practices Act (FDCPA). If we relied solely on reaching consumers during a call center’s business hours, that is almost a quarter of consumers who wouldn’t engage and take the next steps in their repayment process.

Our omnichannel approach is compelling for our clients as well—and it’s proven to pay off. As Todd Johnsen, Senior Manager of Collections Vendors for Snap Finance, explained:

“This audience [consumers in debt] may have already had experiences with incessant collection phone calls, and they are used to avoiding them. I wanted to find an agency that was doing things differently. I knew that TrueAccord was using technology and digital channels in a way that other providers weren’t. What we saw was almost 25-35% better performance with TrueAccord, compared to the accounts we placed with traditional agencies.”

See what other clients and consumers had to say about their debt recovery experiences with TrueAccord in our case studies and resources here»»

The Recovery Opportunities are Ripe with the Omnichannel Approach

Omnichannel targeting is a more effective way of maximizing repayment and conversation rates by offering a level of service and personalization that customers have come to expect from companies in the digital age.

With this holistic communication strategy, you can engage with every single account while call center agents still deliver the human touchpoint that can never fully be replaced. Reach customers with the right message, through the right channel, at the right time that works best for them—whether through email, text, or with a real person ready to guide customers back to financial health.

Businesses and consumers are buckling up for a bumpy economic road in 2023, but your company doesn’t have to accept that these recovery roadblocks spell inevitable losses. With the right digital communication strategy you can turn challenges into opportunities and engagement into recovered revenue.

Let’s look at the roadblocks—and uncover the opportunities.

The Roadblocks Between Your Business and Better Recovery

Delinquencies have been rising (and show no signs of slowing down). According to the latest Experian’s Ascend Market Insights report released in January 2023:

Overall balance delinquency rates increased 6.88% in December

30+ day past due accounts showed a 3.94% increase month over month

Month over month views of roll rates show 1.05% of consumer accounts rolled into higher stages of delinquency in December 2022

And looking ahead, TransUnion forecasts serious delinquency rates of 2.6% on credit cards by the end of 2023, up from 2.1% at the end of 2022.

Additionally, it’s no secret that consumer preferences have changed. It’s becoming nearly impossible to reach consumers through traditional methods like outbound calling and letters.

49.5% of consumers take no action after a collections phone call

But now “going digital” isn’t enough—consumers expect self-service, a dynamically personalized experience, and continuous optimization that helps them resolve debt on their own terms and according to their own preferences.

46% of consumers expect to communicate through preferred channels

72% of consumers say they only engage with personalized communications

90% of customers globally expect brands or organizations to have an online self-service support portal

Turning Roadblocks into Omnichannel Opportunities

These ongoing trends could be perceived as challenges, and as a result, many businesses accept losses as a “cost of doing business”—but with the right strategy these roadblocks can actually be opportunities to drive optimization and better engagement.

If your business has been relying on only call center operations, it’s time to shift gears and move to an omnichannel approach—a more effective way of maximizing repayment and conversion rates by offering a level of service and personalization that customers have come to expect from companies in the digital age. An omnichannel strategy facilitates engagement with customers and enables them to self-serve while freeing up agents to talk to customers that need more assistance.

McKinsey found in a study of 1,000 delinquent customers that digital channels such as emails and text messaging drove higher repayment action rates vs traditional channels, like outbound calling. In some cases, traditional outreach methods elicited 18% fewer responses from customers with accounts 30 days past due who prefer digital communications.

And the benefits of communicating with consumers digitally continues:

65% of consumers open at least one email

35% click at least one link in an email

25% visit links after 9PM and before 8AM “presumptively inconvenient times”

And predictions show that 61% of total interactions with a brand will be through messaging by the end of 2023

At TrueAccord, we’ve found that 96% of consumers who resolve their debt with us do so via digital self-service, without any human interaction. But don’t just take our word for it:

“This audience [consumers in debt] may have already had experiences with incessant collection phone calls, and they are used to avoiding them. I wanted to find an agency that was doing things differently. I knew that TrueAccord was using technology and digital channels in a way that other providers weren’t. What we saw was almost 25-35% better performance with TrueAccord, compared to the accounts we placed with traditional agencies.”

Navigate 2023’s Roadblocks with Your Roadmap to Better Recovery

While the economic landscape may seem like there’s a rocky road ahead, consumers aren’t taking an entirely negative outlook. According to TransUnion’s Consumer Pulse study, 52% of U.S. consumers said they are optimistic about their financial future during the next 12 months.

Now is the time to focus on creating a better experience and supporting consumer optimism about their road to financial health. Discover your own path to helping customers move into repayment with our new eBook, Your Roadmap to Better Recovery in 2023 – available for download now»

When it comes to New Year’s resolutions, improving personal finances isn’t anything new. But as we look ahead to 2023, we see more and more Americans adding serious financial goals to their list. A recent Ascent survey found 66% of Americans plan on making a financial resolution.

And your business should be paying attention to the New Year goals of consumers: it’s the ideal time to support your customers to pay off debt (one of the most common financial resolutions for 2023) by meeting them where they are—with the right message, right channel, and right time.

Let’s take a look at why now is one of the best times to start engaging with consumers in a more flexible way to recover more in 2023.

Financial Resolutions Rise, Along with Delinquency Rates

As we mentioned above, financial resolutions aren’t new, but the number of Americans making them is rising (which might have something to do with rising delinquency rates). For 2022, it is estimated that more than 92 million Americans made financial new year’s resolutions, compared to only 60 million who reported making a financial resolution in 2021. And surveys found that 41% of respondents expressed a strong desire to prioritize paying down debt in 2022—a trend that will continue into 2023 for good reason.

For six consecutive months there have been increases in the 30+ days past due delinquency rates, with those accounts showing a 3.28% increase month over month in October, according to Experian’s November Ascend Market Insights. Looking ahead, TransUnion predicts delinquency rates could rise to 2.6% at the end of 2023 from 2.1% by year-end, which would represent a 20.3% year-over-year increase in delinquent accounts if the projections prove accurate.

Regardless of consumers’ personal financial goals, these delinquency rates and predicted trends are a sign that if you’re not already tailoring your collections communications to today’s consumer preferences, then a better engagement strategy needs to be your organization’s resolution for 2023.

New Year, New You, New Collection Strategy

Meeting consumer preferences is about more than just boosting your bottom line (although that is a bonus)—showing empathy as delinquencies continue to rise can help retain customers even during their often stressful experience of being in debt. An early December survey from U.S. News & World Report shows that 81.6% of Americans who have credit card debt are experiencing anywhere from a little to a lot of anxiety about it. Among respondents to the Ascent survey who plan to make financial New Year’s resolutions for 2023, only 20% are optimistic about keeping them, with 63% predicting it’ll be too expensive to do so.

Help your customers keep their resolutions by making it easier for them to engage on their own terms with the right message through the right channel at the right time, and recover more in 2023.

Let’s look at how to do it:

Right Message As all these recent surveys have shown, consumers are literally telling us that they want to pay down debt in the new year. But treating them in a one-size-fits-all approach can fall flat when trying to engage an individual, especially when it comes to sensitive financial situations or delinquent accounts. In fact, 72% of consumers say they only engage with personalized communications, so don’t miss the opportunity to communicate in a way that resonates with them. Learn more in our Buyer’s Guide to Digitally Engage Your Past-Due Customers here»

Right Channel Engage with consumers through their preferred channels, whether it’s by email, SMS, or traditional calling. Research shows that 46% of consumers already expect to communicate through preferred channels. By using advanced machine learning (like TrueAccord’s patented decision engine, HeartBeat), your business can identify the ideal way to reach the customer and pivot in realtime based on reactions or engagements. Learn more about how to Elevate Your Collection Strategy with Machine Learning and HeartBeat here»

Right Time Minimize unnecessary communication efforts and reach consumers at a productive time—which can be easier said than done if your business is still relying solely on call-and-collect methods. To meet compliance regulations, the FDCPA prohibits communication through any channel at known inconvenient times for consumers, presumed to be inconvenient between 8AM to 9PM, but often customers choose to pay their bills and resolve their accounts outside the presumptively inconvenient hours as long as they can access online account portals that allow them to see account information and take actions to resolve their account. Learn more about it in our State of Compliance & Collections report here»

Not sure if strategizing to engage your customers is the right New Year’s Resolution for your business? Just look at how customers responded to TrueAccord’s customer-friendly, digital approach to debt collection in our 2022 Year in Review and schedule a consultation today to get started!

TrueAccord is a machine-learning and Al-driven 3rd-party debt collection company that is reinventing debt collection. We make debt collection empathetic and customer-focused and deliver a great user experience.

Our digital-first approach to debt collection creates a cycle of collections growth:

1. Improve the perception of the industry

2. Provide a personalized experience

3. Build brand equity and collect