TrueAccord’s machine learning based system handles millions of consumer interactions a month and is growing fast. In this podcast, hear our Head of Engineering Mike Higuera talk about scaling challenges, prioritizing work on bugs vs. features, and other pressing topics he’s had to deal with while building our system.

TrueAccord’s system is machine learning based, but every new product type requires a little bit of tuning to beat the competition. Hear our CSO and VP of Finance in this short podcast about the Conversion Team and what it does to make sure TrueAccord stays ahead of competition.

Our CEO, Ohad Samet, recorded a podcast with Lend Academy discussing the positive impact technology is creating in the collections space and the need for more innovation. Will discuss TrueAccord’s unique approach to debt collection using data-driven, digital communications to create deeply personalized consumer experiences.

The podcast also covers the current state of the collections industry and where it’s likely headed as regulatory pressure, consumer preferences and compliance requirements converge. Will cover how TrueAccord is using machine learning to deliver deeply personalized and engaging experiences for consumers while achieving higher recovery rates across various debt types.

Tune in and learn:

The state of the debt collection industry today and where it’s headed

How the use of machine learning is personalizing the debt collections experience for greater conversions

Why code-driven compliance outperforms traditional collections practices by reducing risk to organizations

How understanding consumers’ preferences for easy, self-service options with flexibility empowers more consumers to pay off their debt and get on a path to financial health

Yesterday, in an article on InsideARM.com, Tim Bauer, the President of InsideARM, described a somber state of affairs:

The TCPA and the 2015 FCC Rules interpreting the act have effectively eliminated the use of technology to efficiently call cell phones. Land line usage is dropping like an anchor. The CFPB is on the brink of announcing proposed debt collection rules that are likely to reduce the number of call attempts that can be made. Now, add this latest call blocking technology and the industry is challenged again.

This is a strong statement from a prominent thought leader in the debt collection industry. Mr. Bauer pointed out many efforts by different regulatory agencies and how they impact call centers: “anecdotal reports of right party connects down by 15-30%”, as the FCC includes debt collection calls as an “unwanted call” category in it’s “robocall” blocking initiatives.

At TrueAccord, we agree. The industry has been seeing tremendous pressure on its ability to call consumers efficiently, not only because of regulatory pressure – this pressure is driven by consumer preference, and the fact that consumers often opt to not pick up the phone, not to mention opening a letter. As strong advocates for technology in debt collection, with our CEO now part of the CFPB’s Consumer Advisory Board, we will continue to support forward thinkers such as Mr. Bauer and others who call for the use of new technologies in debt collection. It is the consumer friendly, smart, and efficient approach for the 21st century, and we strongly encourage our peers in this industry to begin adopting and utilizing these channels in preparation for the CFPB’s expected Notice of Proposed Rulemaking, expected later this year.

Debt collection is a highly litigated activity. Compliance personnel and systems budgets are crowding out other investments. It’s appropriate: debt collectors and creditors are often hit by class action lawsuits and government action, leading to huge fines and settlements. Reducing risk is their primary priority. When examined closely, though, the traditional debt collection model attracts numerous compliance issues. The legacy approach is being replaced by machine learning and digital first systems. These code-controlled systems offer predictable, scalable, and auditable operations that, coupled with best in class user experience, significantly reduce the risk of litigation and regulatory action.

The traditional model invites regulatory scrutiny and lawsuits

Collectors often cite compliance concerns as impediment to adopting new technologies. Lawyers are concerned about TCPA exposure from text messaging, consent requirements for emails, and FDCPA violations when using social media. These concerns are unfounded: text messages can be safely delivered if consent and revocation are properly documented, the CFPB saw no need for consent to email (as reflected by a growing body of opinions, as well as its 2016 rule outline), and social media can be used with restraint. While dragging their feet on evaluating new technologies, compliance departments embrace and perpetuate much bigger risks: the prevalent use of human labor, over reliance on phone calls, and the outdated, fragmented interfaces used by collectors.

Humans are the weakest link in the compliance chain

Traditional wisdom says that only people collect from people. That claim is demonstrably false. People are subject to biases and acting emotionally when interacting with debtors – which is why machine learning based systems collect better than humans. People may be tired, angry, or distracted. They can be baited into violating the FDCPA by a ill-meaning debtor. The prevalent commission-based compensation model, a broken and outdated model for collections, puts them in odds with debtors whenever they interact. Human beings just cannot do error-free work, no matter how trained or experienced they are.

Keeping appropriate staffing levels is another challenge for collection teams. Large market participants report 75-100% annual turnover rates (per the CFPB’s operational survey), requiring constant hiring of collection staff. Training and overseeing these new people is a daunting task, especially with the ever changing case law and legislative landscape in the collection space. Providing an efficient and fully compliant collection experience while relying on new and untrained collectors is almost impossible.

Phone calls are a dying communication method

Consumer preference is shifting away from phone calls, but phone call compliance would have been difficult even if that wasn’t the case. Calls are a compliance liability due to their frequency, their real-time nature, and the overall regulatory sentiment towards them.

Collection calls must be frequent to reach consumers. On days when an agent works an account, they may attempt to contact the consumer 4-6 times, often as frequently as 10 times per day. Consumers aren’t picking up the phone, so agents need to make more call attempts to try and reach them. While most states, and the FDCPA, don’t limit call frequency, high frequency of calls often leads to complaints and lawsuits alleging harassment. Collector take this huge risk because calling is the only tool they understand.

Collection calls are also real-time. No matter how elaborate call scripts are and how experienced collectors may be, it is impossible to completely control the development of any individual call. Voice analytics software is limited, unable to identify most baiting and escalation issues. Real time monitoring of all calls by supervisors is financially implausible. Collection agencies are forced to settle for the best training possible, clear escalation paths for collectors whose calls go badly, and hoping for the best. Realistically, when making a large volume of calls, every day will have some potential violation.

Finally, regulation has been working against phone calls for the past few years. The FCC’s ruling limiting the use of ATDS has been devastating, and expecting it to be completely undone by the new commissioner is a pipe dream – government is not debt collectors’ friend. States like West Virginia and Massachusetts have enacted call frequency limitations, and the CFPB’s new rule outline includes a 6-times-per-week limit on call attempts. All signs point to a future where phone calls cannot plausibly be the main channel for collecting debt with any semblance of compliance.

Code driven compliance is here, and it’s a big step forward

Code driven compliance gives us complete control on what actions can be triggered by our system. It’s one of the components in Heartbeat, our machine learning-based, digital first collection platform. Heartbeat is a leap forward in debt collection, and its compliance advantages are many: from better user experience to perfect auditability.

Best in class user experience in debt collection is a compliance advantage

Many if not most of debt collection lawsuits hang on a technicality. A word is arguably missing or written in a debatable way. It’s unclear whether 8 calls or 9 calls constitute harassment. Often, consumers don’t resort to lawyers because they know for a fact they have been wronged – it is often not clear that they have been – but because their experience with the collector has been bad enough to push them to seek defence or retribution. Great user experience is therefore not only a way to improve the creditor’s brand perception and returns, but also a way to reduce the rate of complaints and lawsuits. TrueAccord’s Heartbeat system attempts to contact consumers an average of 3 times per week, compared to 4-6 times a day for traditional agencies. That, paired with best in class web and mobile experience and a helpful customer service department, significantly reduces consumers’ desire to sue for, or complain about, ambiguous technicalities.

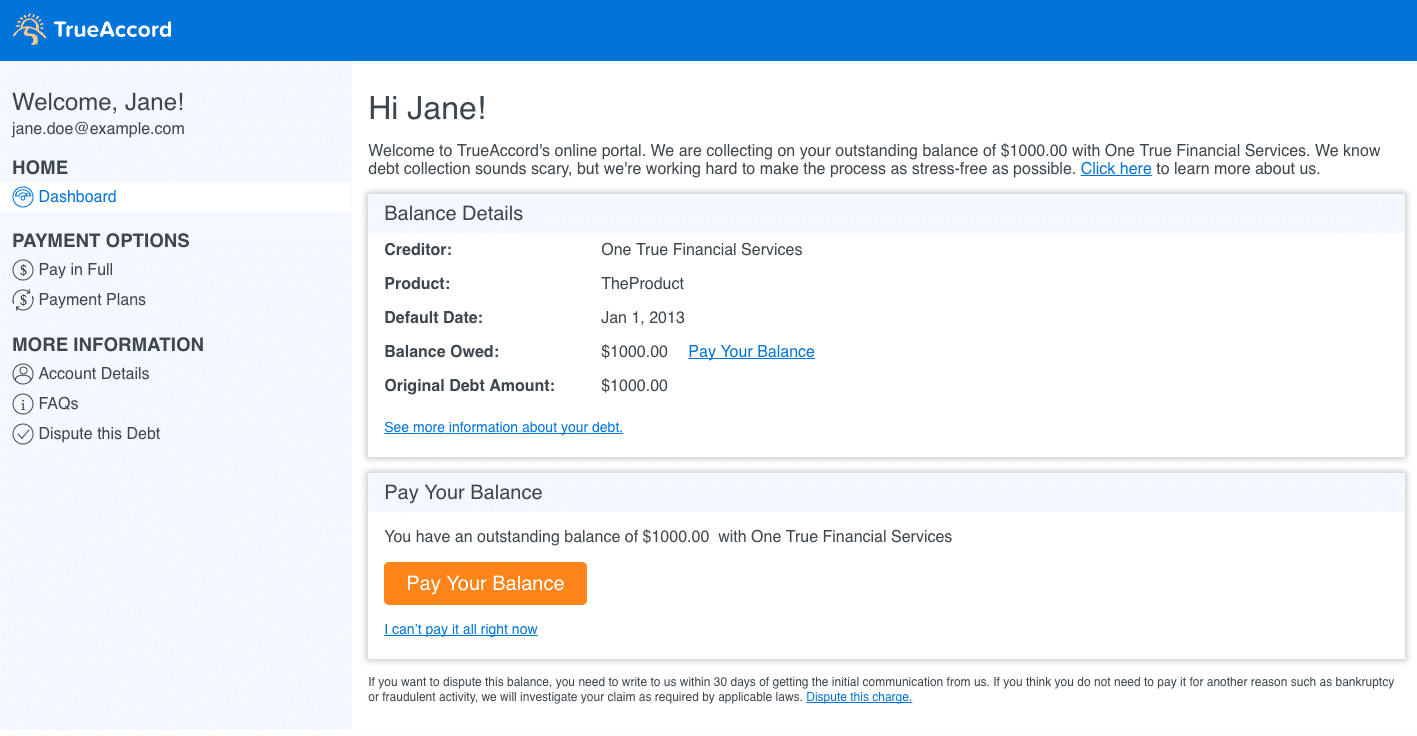

Consumers get a consolidated account page showing all their options

Since more than 90% of Heartbeat’s interactions with the consumer do not involve a human collector, human beings are only needed for a fraction of the work. TrueAccord is able to hire skilled workers and pay them a living wage, with no commission component. Knowing that they will earn a good salary working for a technology startup reduces any incentive our team members would have had to fight with or harass consumers. That, in turn, contributes to great user experience and reduces compliance risk.

Pre-approved content and an integrated system eliminate human error

Human error is the biggest challenge for compliance departments. Collectors today need to navigate multiple systems to call, negotiate with, and collect payments from consumers. Updating the results of a call is often a complex process, requiring yet another system. Many requests to unsubscribe numbers, cease and desist communications, or simply to provide debt verification are lost and lead to complaints. This fragmented process is extremely tedious and time consuming, and inherently flawed. Letting collectors write their own emails and text messages is too much risk – something that will surely lead to violations on a daily basis.

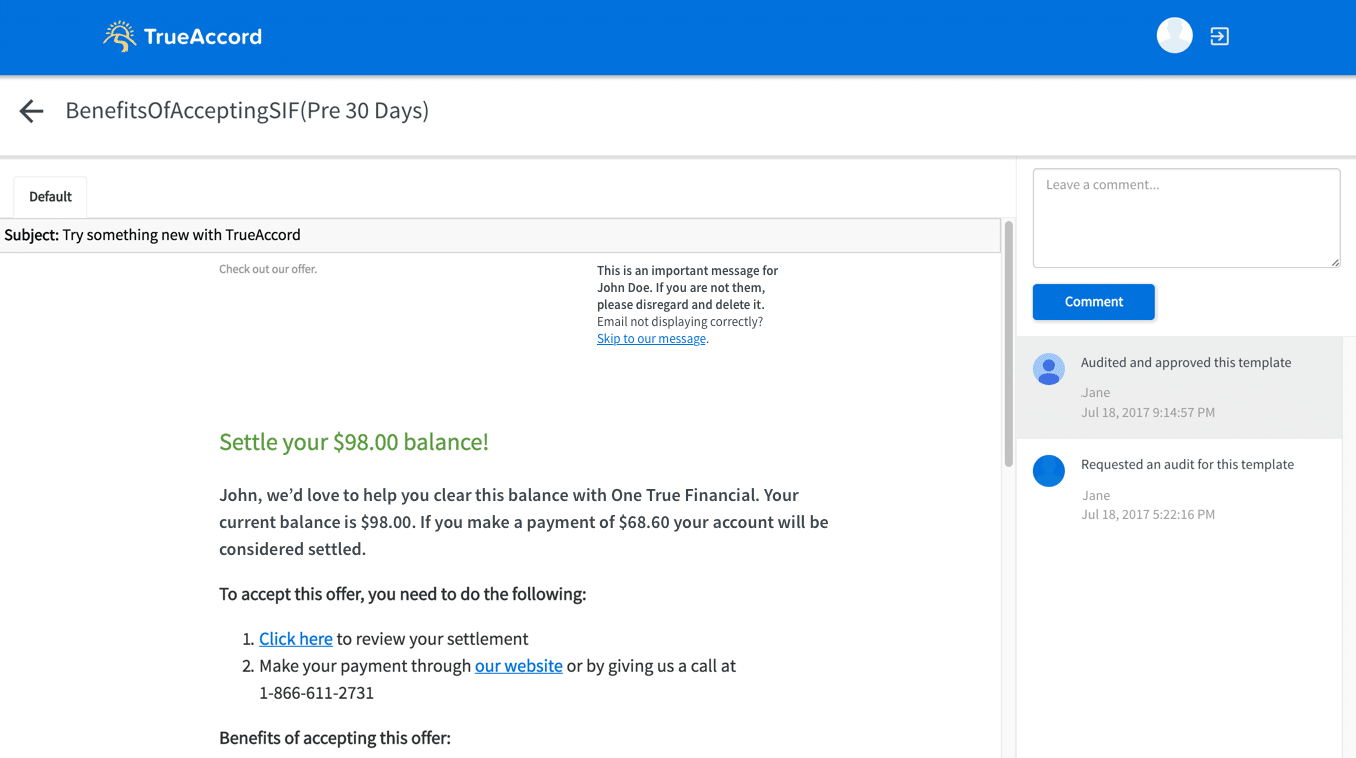

TrueAccord’s content approval console

Heartbeat takes a code controlled approach to communications. Every outgoing communication is pre-written, then reviewed and pre-approved by TrueAccord’s legal team. Every email, text, web page and letter have to pass TrueAccord’s content guidelines driven by law, policy and procedures, including required disclosures and forbidding certain words and phrases in subject lines, or in the body of communications. Our clients’ legal and content team are also involved in commenting on our procedures as well as specific content items, to make sure we fit each company’s risk tolerance. Heartbeat will only send text messages to numbers that it knows it has express consent to text, and that have gone through an ownership check within a defined time period. Even when collectors respond to inbound consumer emails, they use pre-written replies that then direct Heartbeat how to proceed in serving the consumer. The decision to proactively communicate is strictly based on Heartbeat logic, not on collector whims; collectors cannot decide to contact consumers whenever they see fit.

After contacting consumers, the system monitors their response. Consumers can easily opt out of communications, by replying to a text message or by clicking a link in every email that lets them easily unsubscribe from future email communications. Every email and every payment page contain a link that lets consumers ask for debt verification via a few simple online steps instead of a cumbersome and mail-based process. Every interaction is designed to give consumers an opportunity to ask for more information or limit communications to their preferred channel. Though easy to dismiss as an invitation for abuse, these options increase consumer engagement and result in overall better collections – while significantly reducing complaints about continued communications and missing documentation. These two categories have consistently been the top reasons for filing CFPB disputes ever since its dispute portal was made public.

The compliance firewall: enforcing compliance at scale

Human collectors are expected to remember dozens, maybe hundreds of compliance laws and regulations as well as creditor-imposed rules. It’s an impossible task, greatly simplified by Heartbeat’s Compliance Firewall. Since it controls all contact decisions by code, Heartbeat can enforce its compliance policy at scale on every interaction without needing to train human collectors. Contact timing or frequency, matching content to the right stage in a consumer’s process or preventing the use of unsubscribed contact methods, even making sure that a consumer doesn’t get a payment offer that the creditor didn’t approve – all are controlled by the Compliance Checker. Any attempted action outside of its well defined policy is dropped. Since it’s code controlled, it cannot forget to check the time and call a consumer after 9pm or before 8am.

The Compliance Firewall also allows updates to policies and procedures. Every new update can be implemented with accuracy within days, once the appropriate code is written. By taking judgement away from the collector and subjecting all contact decisions to a data-based, code-controlled system, Heartbeat makes the optimal decision for consumer experience and driving payments, without harassing the consumer or violating the myriad of restrictions that govern debt collection.

The easiest system to audit

Compliance requires tight monitoring, and creditors audit a large sample of collection activities by their vendors. With so many voice calls, even if they are all recorded, complete and accurate audits are impossible. Auditors need to sample cases and hope to find the right patterns, or employ a large and expensive team for sufficient coverage. Heartbeat eliminates almost 95% of phone calls (typically attempting to reach the consumer 3-5 times over a 90 day period), instead focusing on written communication. Back and forth written interactions are easier to capture, store, and search. The system also saves consumers’ browsing pattern on the website and their interactions with the content they receive. It’s easy to track consumer behavior and how the system responded to it, as well as why it made a specific decision. Code controlled compliance means that decisions are easy to replicate and trace back in case they’re questioned.

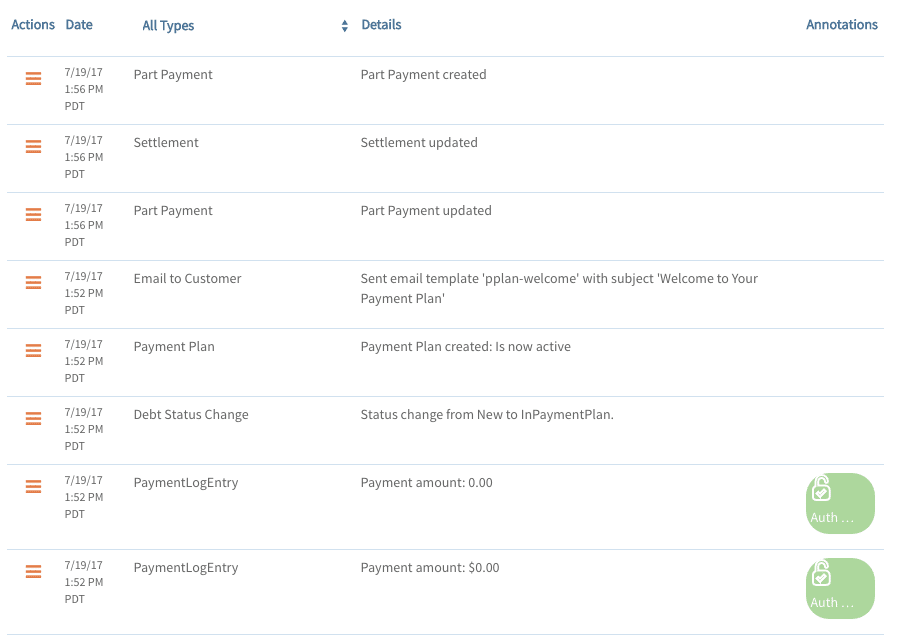

A readout from TrueAccord’s event-based audit trail

TrueAccord’s system also has an audit interface for creditor audits. Compliance staff can easily search for accounts and review all collection activity – including recorded calls, emails, and every other contact. It’s a much easier approach to compliance and controls than an unwieldy excel file or PDFs dropped in an FTP folder. TrueAccord’s data retention and tracking of consumer behavior provide a fuller snapshot of Heartbeat’s collection decisions and how consumers reacted to them.

Code driven compliance is the future

We examined the inherent risks in traditional collection activities and how sticking to the phone as the leading collection tool in a call center environment creates more risks than rewards. Then, we dove into how code controlled compliance offers predictable, pre-approved, and consistent collection strategies that are easy to audit and understand. The coming years will see more and more creditors and collectors move to these machine learning based systems, as they demonstrate dominance in returns and compliance. It’s time for risk averse compliance departments to realize that they are putting businesses at risk by sticking to their phone-based roots, and look beyond tradition. A whole world of mature, stable and trustworthy technologies awaits.

Though historically resistant to innovation, the collection industry feels pressured to make changes. Consumer preference, requirements from clients and mounting costs dictate increased use of technology – a welcome trend. Among those new tools, we are starting to see increasing adoption of emails for collections. Agencies have a small selection of vendors to blast out an email. Agencies with large call centers view this as a cost reduction exercise, and another way to get consumers to call in and talk to their agents.

Consumer behavior is changing. As more of us are glued to our mobile phones, emails, and social media accounts, it’s clear that the old ways of collecting debt are quickly becoming irrelevant. Still, the market doesn’t offer a multitude of collection solutions aimed at responding to the digital consumer. When we present our machine learning-based solution to prospective customers, we’re often asked about the difference between our solution and a self service portal. Although both solutions are digital, they cannot be less alike.

Automation and digitization offer new tools for the collection strategist, augmenting the traditional building blocks. These new tools, introducing flexibility and sophistication that are usually attributed to other parts of the business, can mitigate common pitfalls.

Automation and digitization offer new tools for your collection strategy, augmenting the traditional building blocks. These new tools, introducing flexibility and sophistication that are usually attributed to other parts of the business, can mitigate common pitfalls.

In this series, adapted from our free eBook Automating Debt Collection 101, we’ll review the three major areas where automation and digitization can boost a collection strategy:

Early contacts and improved segmentation

Persistent communication

Improved customer satisfaction

In this second part, we’ll focus on improving performance with persistent communication.

Customers in debt are in a dire situation, cannot pay the balance in full, and many times even a payment plan isn’t feasible. A call center is limited in its flexibility – beyond a certain number of payments or customizations, a human agent is just too expensive. These accounts risk being mishandled, and end up paying less than they could with some “hand holding”.

Automated collections have a tremendous advantage in handling complex cases. The platform consistently follows up with customers using multiple channels, offering various solutions according to an optimized offer strategy, and administers changes in those solutions (split payments, rescheduling and more) over time as needs change. These tools can accept and administer a monthly $5 payment that increases over time, even if the customer misses a few payments and needs consistent follow-ups. When the vast majority of contacts are automated, even small amounts are profitable – and add up. The system doesn’t get tired, doesn’t get angry, and doesn’t need to go home by the end of the day. It’s there to service the customer.

TrueAccord sees more than 35% of customers in an average placement click on a link and negotiate with an automated system, thanks to diligent and relevant follow ups. In tests, working on the long tail of underserved accounts yields 4-8% of additional recovery – dollars that would otherwise be considered lost.

TrueAccord is a machine-learning and Al-driven 3rd-party debt collection company that is reinventing debt collection. We make debt collection empathetic and customer-focused and deliver a great user experience.

Our digital-first approach to debt collection creates a cycle of collections growth:

1. Improve the perception of the industry

2. Provide a personalized experience

3. Build brand equity and collect