After three decades of providing exceptional customer experience, a leading national bank recognized a lot has changed in the world of personal banking, technology, compliance, and, in turn, debt collection. To continue delivering the level of service their customers expect meant it was time for the bank to update their recovery methods for the new digital age.

Although the bank had seen moderate success in late-stage collections with their call-and-collect vendor, they had a list of goals that they were unsure their existing collection provider could achieve:

Improve and increase liquidation performance

Keep up with new regulations and ensure compliance

Leverage new, more cost-effective solution

But what was the best way to evaluate the effectiveness of new digital-first engagement versus their existing outbound calling approach?

To test and measure the success of each distinct debt recovery method, the bank decided to use the Champion-Challenger model with TrueAccord joining their existing collections partner.

For their Champion-Challenger test, the bank assigned TrueAccord 50% of primary placements and tertiary placements against their traditional collection provider. By using scorecards, the bank was able to compare the two using set collection goals (varying by month and season) and several key performance indicators (KPIs), including:

Overall liquidation rates

Percentage of settlements in full

Percentage over/under set collection goals

With the Champion-Challenger model in place, collection goals and KPIs designated, and scorecards set, it was time to see how TrueAccord’s digital engagement methods would measure up compared to the old school call-and-collect method…and the numbers would speak for themselves.

If your business plans to use outbound calling as the main mode of engaging past-due customers in 2024…good luck.

Good luck reaching the right number for the target customer. Good luck getting them to commit to repayment over the phone. Good luck not getting complaints.

And if the plan is only to use outbound calling…be prepared to start accepting more losses in 2024. Even if you can get the right customer on the phone, studies show 49.5% of consumers take no action after a collection call.

Let’s look at the challenges around right-party contact rates, consumer complaints, and the timely factors that make the challenges more detrimental to your business’s late-stage debt recovery.

Declining RPC Rates

The decline of right-party contact rates (RPC)—the percentage of calls in which an agent is able to connect with the target consumer—isn’t new for 2024, but its impact on debt collection is reaching new heights in the new year. RPC is considered one of the most accurate measurements for the effectiveness of an organization’s outbound calling efforts, whether internally or through a third party.

Surveys from the Association of Credit and Collections Professionals (ACA International) found that 62% of the respondents reported seeing a decrease in right-party contacts, with 78% of the respondents experiencing call-blocking and 74% having their calls mislabeled.

Call-blocking and spam-mislabeling are only part of the issue for RPC rates: government regulations, robocalls, lack of consumer trust in answering calls, and inaccurate phone data all contribute to the drop in RPC rates.

The bottom line is the declining RPC rates are negatively affecting your business’s bottom line—but that’s not the only challenge outbound dialing for debt collection faces in 2024.

Rising Consumer Complaints

As almost all other forms of financial transactions have evolved, so have consumers’ communication preferences in that arena. Nearly nine in ten Americans are now using some form of digital payments and 59.5% of consumers prefer email as their first choice for communication, but traditional call-and-collect methods still dominate in late-stage recovery efforts.

And with that in mind, it shouldn’t be surprising that consumers complain about debt collectors’ and creditors’ communication tactics used when collecting debts.

But beyond ignoring communication preferences, many consumer complaints actually equate to compliance violations.

According to the 2022 Annual Report on the Fair Debt Collection Practices Act (FDCPA), 51% of communication-related complaints were because of repeated calls. Despite the 7-in-7 Rule (debt collectors are prohibited from calling the same consumer more than seven times within seven consecutive days, unless the consumer directly gives consent to receive any additional calls), 17% of respondents of a Consumer Financial Protection Bureau (CFPB) survey said a creditor or debt collector tried contacting them eight or more times per week. Similarly, other common complaints revolve around the collector or creditor calling at inconvenient hours outside of the FDCPA presumed convenient calling hours from 8:00 a.m. to 9:00 p.m. at the consumer’s location.

But again, even if you are following the letter of the law, it doesn’t protect your brand’s reputation from consumer complaints.

Minimize These Collection Challenges with a Digital-First Approach

Between declining RPC rates, shifting consumer preferences, rising consumer complaints, and increasingly stricter compliance regulations, the once tried-and-true outbound calling methods are no longer viable in 2024.

But your business doesn’t have to resign to accepting losses once accounts hit late-stage delinquency—taking a digital-first approach negates concerns over RPC rates, catches up with evolving consumer preferences, neutralizes the cause of common consumer complaints, and smoothly navigates compliance requirements.

Did you know one of the most common reasons for missing a payment is because customers simply forget to pay their bill?

But staying top of mind for consumers is harder than ever using traditional call-and-collect methods considering stricter compliance regulations and the fact that 94% of unidentified calls go unanswered.

Simply adding email into the communication mix often isn’t enough, and there’s a lot that goes on between hitting “send” and reaching the inbox. For your business to improve performance using digital debt collection, you need a partner with the right expertise.

Let’s look at six key questions to ask your business partners about email deliverability in debt collection, why each question is important, and how TrueAccord measures up.

1) What is Their Primary Method of Communication in Digital Debt Collection?

Why It Matters The success of traditional call-and-collect methods are waning compared to modern digital engagement due to more consumers preferring digital communications, declining right-party contact rates, and increasing compliance restrictions.

This notion is further proven by recent surveys showing that roughly 40% of consumers prefer to be contacted by email first. And honoring a consumer’s preferences in digital debt collection pays off. In fact, contacting a customer through their preferred channel first can lead to a 10% increase in their payments.

How TrueAccord Measures Up TrueAccord is a digital first, omnichannel debt collection agency—and has been a leader in digital consumer engagement. The company believes that digital debt collection is a financial service, and needs to cater to the needs of consumers.

2) 2) How Long Have They Used Email as a Form of Communication?

Why It Matters Many debt collection providers have been slow to adopt digital communication as part of their consumer outreach, and even those who have integrated digital are still refining strategies for optimal outcomes. By choosing a partner who has a history of refining debt recovery email performance, your business will be able to increase collections with strategies that honor consumer preferences.

How TrueAccord Measures Up From the start of the company in 2013, TrueAccord’s approach to consumer engagement has been digital-first. This notion continues to grow into a robust omni-channel operation through machine learning that’s driven by data from 40 million customer engagements and counting.

3) What is Their Debt Collection Email Delivery Rate?

Why It Matters Email Delivery Rate refers to the successful transmission of an email from the sender to the recipient’s mail server, measured by emails delivered divided by the number of emails sent. Digital debt collection partners that can achieve a high rate gives your business confidence that communications are getting in front of delinquent customers.

How TrueAccord Measures Up TrueAccord has a 99% email delivery rate, compared to the average email delivery rate of approximately 90%. It’s one of the main metrics that separates debt recovery email performance of TrueAccord services from the competition.

4) What is Their Email Deliverability Rate?

Why It Matters Successful email delivery doesn’t mean that it actually makes it into the recipient’s inbox. Deliverability divides how many emails reach the recipient’s inbox, as opposed to their spam folder, by the total number of emails sent. Your domain reputation also has a big impact on email deliverability in debt collection. The better your email reputation, the less likely your communications are to end up in spam folders.

How TrueAccord Measures Up TrueAccord has a 95% email deliverability rate, compared to the worldwide average of 84.8%.

5) Do They Measure Open Rates and/or Click Rates?

Why It Matters Measuring open rates (percentage of recipients who opened your email) and click-through rates (percentage of those who clicked on a link in the email) play a dominant role in understanding which communications are resonating with recipients and which are not. With accurate reporting of these crucial debt recovery email performance metrics, your business will be better positioned to optimize your collections strategy.

How TrueAccord Measures Up TrueAccord has a total open rate 55.19% and total click rate 1.56%, compared to the average industry total open rate of 27.76% and click rate of 1.3%.

6) How Do They Make Adjustments When Email Deliverability and/or Delivery Rates Fluctuate?

Why It Matters Email delivery and deliverability rates will fluctuate, but how a provider responds and adjusts to these changes is crucial to keeping the rates as high as possible. Every business has unique variables that affect these metrics. By leveraging machine-learning and consumer data, businesses have a better opportunity to keep collection performance high even during times of fluctuation.

How TrueAccord Measures Up TrueAccord’s dedicated email and deliverability experts proactively monitor and make adjustments, along with using our patented machine learning engine, HeartBeat. This technology helps to improve debt recovery email performance by optimizing communication engagement over time.

Ready to Reach Optimal Consumer Engagement in Your Debt Collection Operations?

Is your business ready to improve its digital debt collection strategy? Start by scheduling a consultation to learn more about what influences email delivery and deliverability rates and how TrueAccord consistently performs above the rest. Our email and deliverability experts are happy to talk through how your debt recovery email performance can be improved.

If your business and collection partners aren’t utilizing email in your debt recovery strategy, you’re leaving vital engagement opportunities (and potential collections) on the table. There are plenty of reasons why digital communications are the way to go, but reaching out through email is especially important in collections.

Surveys show that 59.5% of consumers prefer email as their first choice for communication, and 14% of bill-payers prioritize payments that offer lower-friction payment experiences, which increases to 23% for millennials specifically. Considering this, it shouldn’t come as a surprise that courts have actually ruled that “an email is less intrusive than a phone call” for debt collection.

But what makes a successful email program when it comes to connecting with delinquent accounts? Whether your business is handling collections in-house or are looking at working with a third party, your operations should be confident that you have these core components covered.

Core Components for a Successful Email Program

While adding email into the communication channel mix is critical, it is the set up, execution, and continued optimization of that email program that can actually make a difference when it comes to consumer engagement. There are many elements to a successful email strategy, but here are three of the core components that we’ll focus on:

Infrastructure, Data, and Content

All 3 are required for a successful email program—each one relies on the other two to create a high performing program.

Let’s take a look at why each of these is important and the risks that can occur without each component in place.

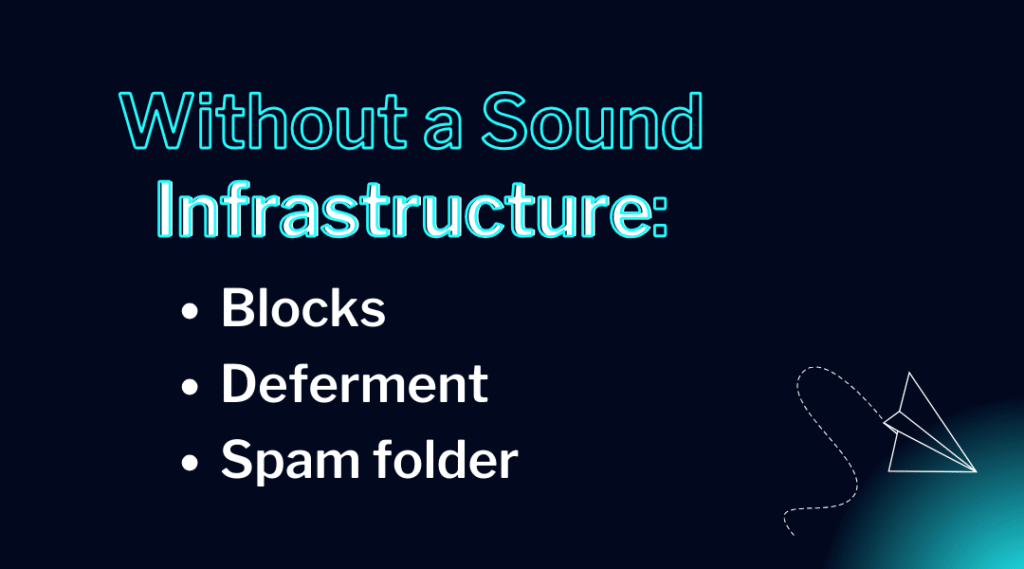

INFRASTRUCTURE

The infrastructure an email program is built on has many components itself: Mail Servers, Mailbox Providers, Internet Service Providers (ISPs), Email service providers (ESPs), and more. How these components are set up and work together influences sender reputation, which in turn influences email delivery rates. You can learn more about these different pieces in our blog focusing on the The (Hidden) Anatomy of Emailhere»»

While infrastructure can admittedly be complex, the risks your operation runs without a sound infrastructure are clear and quite consequential, including having your emails blocked, deferred or delayed delivery, or winding up lost in the recipient’s spam folder.

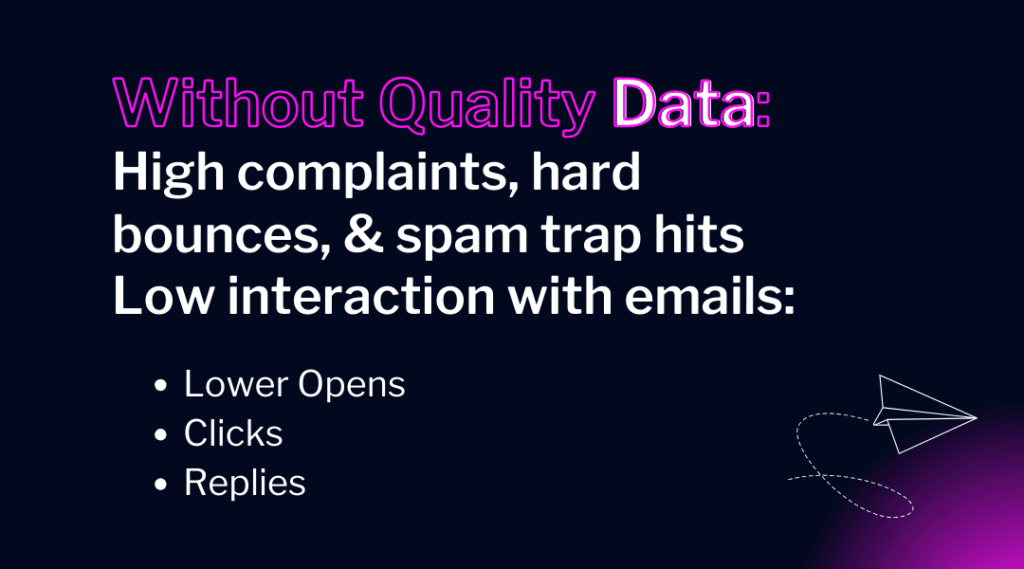

DATA

In today’s digital world, data is everywhere—but how you harness that data can make or break your email program (and even get you into hot water if you or your collections partner are not following all the necessary compliance regulations around data privacy and protection). Understanding data helps intelligently influence an email program, especially when focusing on email engagement metrics such as:

Opens

Clicks

Unsubscribes

Spam complaints

Hard Bounces

Spam traps

But without quality data analyzed appropriately, your emails could result in consumer complaints, hard bounces, falling into spam traps, not to mention negatively impacting all the engagement metrics listed above.

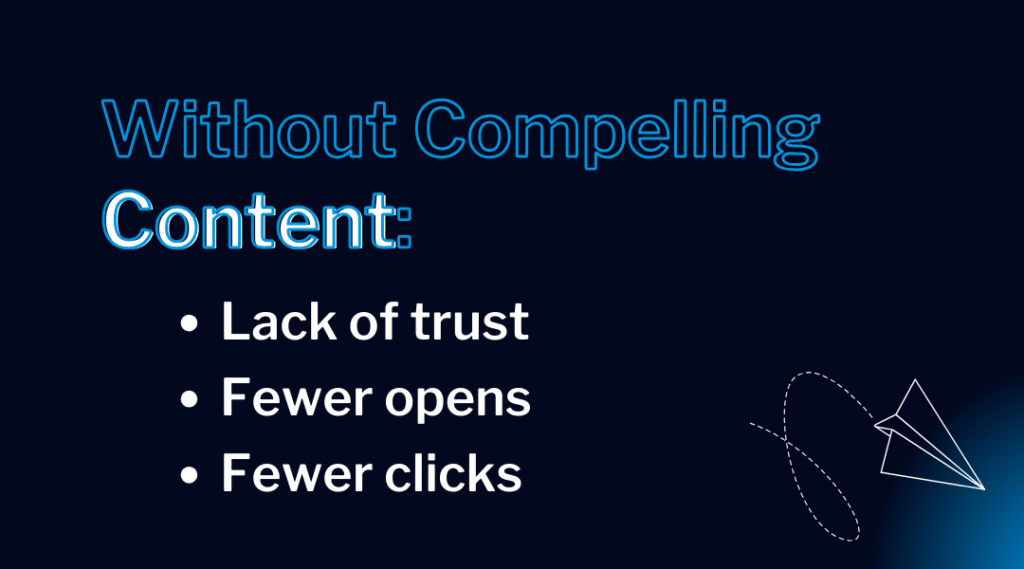

CONTENT

Solid infrastructure and reliable data are essential in any email program, but when it comes to debt collection, content can be the tipping point between a consumer committing to repayment or ignoring the outreach altogether—or even reporting your communications as spam or harassment.

From subject lines to your call-to-action (CTAs), sending the right message to your customers is crucial. Without compelling content you miss opportunities to capture consumers attention resulting in fewer opens, fewer clicks, or even pushing consumer perception in the wrong direction. If you lose your customers’ trust, you’re most likely going to lose the chance to recover their debt.

Successful Email Engagement Can Boost Debt Recovery

Studies have shown that engaging consumers through digital methods can increase resolution rates by as much as 25%. But if your digital efforts are missing any of the core components we just covered above, it doesn’t matter if your collection strategy includes email—your operations are going to be missing recovery opportunities.

When it comes to reaching consumers, it’s no secret that email has surpassed phone calls as the preferred method of communication. In fact, 59.5% of consumers prefer email as their first choice for communication.

But just because your business sends emails to consumers doesn’t mean that your messages make it to their inbox. And if that email never reaches the intended recipient, it doesn’t matter what that customer’s preferred method of communication may be.

There are more factors than you may realize that go into whether or not your email reaches the consumer’s inbox, so let’s look at the hidden anatomy of email and the factors that influence where your emails end up.

What’s the Difference Between Mail Servers, Mailbox Providers, ISPs, and ESPs?

Before we look at what happens when you hit “send” on that email, it’s important to identify some of the key components that operate behind the scenes to get your message from point A to point B.

Mail Server: A mail server (also known as a mail transfer agent or MTA) is an application that receives incoming email from the sender and forwards outgoing messages for delivery to the recipient.

Mailbox Provider: A mailbox provider provides email hosting and implements email servers to send, receive, accept, and store email for the recipient.

ISPs: Internet Service Providers (ISPs) provide internet. Although ISPs can provide email services, separate ESPs are often used for business email operations—but ISPs play a major role in email delivery and landing in the recipient’s inbox.

ESPs: Email service providers (ESPs) are a service that enables businesses to send emails and email campaigns to a list of subscribers.

How Does Email Actually Work?

When you hit the “send” button, your ESP sends the email to the recipient’s mail server through various protocols such as SMTP (Simple Mail Transfer Protocol). The delivery process involves establishing a connection with the recipient’s mail server, transferring the email content, and receiving a response indicating whether the email was accepted or rejected by the mailbox provider.

Several key factors play into whether an email gets tagged in spam or junk or filtered into “social” or “promotion” categories.

Mailbox providers and anti-spam filters make inbox placement decisions based on a 30-day rolling history of sender reputation metrics

Inbox placement is based on the subscriber’s interaction, regardless of your business model

All types of emails are subject to the same filtering, regardless of content

At TrueAccord, every time we send an email our email providers notify us of events like delivered, open, click, hard bounce (such as an email being sent to an invalid or nonexistent email address), soft bounce (typically an indicator of a temporary technical issue on the recipients’ end), and spam complaints.

In the case of bounces, TrueAccord stores that data and categorizes it as not delivered. Emails that result in a soft bounce are temporary bounces and could get delivered within 72 hours. For hard bounces, we will not send to those again—or it severely hurts our reputation among ESPs and ISPs. For Regulation F compliance when delivering disclosures electronically, debt collectors are required to monitor for deliverability. TrueAccord presumes that any hard bounce or undelivered soft-bounce (one that is not delivered after 72 hours of the first soft bounce) has not been delivered.

Why are ISPs So Selective?

the ISPs are selective on what emails get accepted and which actually reach the inbox. But there are three key initiatives ISPs consider:

To protect email account owners from:

Spam

Scams

Poor experience

To protect and prioritize company resources:

Limited email engines i.e. mail servers

Limited bandwidth

Limited personnel or internal expertise

To continue driving revenue:

Lower email interaction reduces ad impressions and revenue

Too many emails can lead to account abandonment from subscribers

Best Practices to Get Your Emails Delivered

Understanding the different components of email, how it actually works, and the selective filters in place to protect consumers are all important to a successful email program. Now let’s look at several best practices to follow:

Build and maintain a positive sender reputation with ISPs and ESPs

Ensure good email list hygiene

Send to actively engaged subscribers

Maintain consistent volume and cadence (avoid spikes)

Avoid spammy subject lines

Develop valuable content that would engage subscribers

While many of these best practices may seem like no-brainers, achieving them can take more skill and effort than most businesses expect. Each of these contribute to email delivery rates and more importantly, deliverability to recipients’ inboxes—key drivers towards consumer engagement and your bottom line.

Outbound calling has been the main mode of collections for decades, but the cost of a call center or in-house full-time employees (FTEs) making calls is no longer justifiable when most consumers simply don’t answer the phone, on top of the mounting compliance restrictions limiting opportunities to call in the first place.

But outbound dialing isn’t completely obsolete—digital-first omnichannel strategies can turn traditional call-and-collect operations around by integrating new digital channels into the communication mix.

Let’s compare traditional outbound calling methods versus a digital-first approach in three key areas impacting your business’s ability to collect more, faster:

COST

COMPLIANCE

CONSUMER PREFERENCES

Get even more statistics and data in our latest eBook — Why Evolve from Outbound Calling to Omnichannel Engagement? Cost, Compliance, & Consumer Preferences — available for download now»»

COST: Call-and-Collect

The cost to collect has been on the rise for traditional methods for years, whether you outsource to a call center or have FTEs dialing the phones.

One reason for this rise is based on the fact that many lenders still practice old strategies to prioritize contacting customers based on their risk profiles, balance, and average days delinquent—completely missing portions of their portfolios. Factoring in propensity to pay is important to successful engagement, but it means that agents’ time is focused on only a small portion of accounts, leaving potential repayments on the table.

Add in the overhead costs, inflation, and hiring challenges of using agents as first attempts at engagement and watch the expenses continue to climb past what you’re able to collect through outbound calling.

COST: Digital-First Omnichannel

Right off the bat, digital-first shows the cost of collections can fall by at least 15%.

Since digital is infinitely scalable, this communication tactic can touch every single account, regardless of scoring models—unlike human dialers who can only physically call a certain number of accounts on any given day. Going digital-first cuts down on the time billed for making repeated outbound calls that are never answered or returned, and it allows agents to interact with customers that want to speak directly to a person.

Overall, digital-first has shown to boost customer engagement by 5x, the first step towards repayment.

COMPLIANCE: Call-and-Collect

It’s no secret that it’s increasingly complicated to reach customers with all the legal communication restrictions.

While all debt collection communication is subject to compliance rules, outbound calling has specific laws and regulations that can carry costly penalties for non-compliance—and it’s only becoming more complex with new state-specific rules rolling out right and left. But no matter where your business is doing business, if you’re making collection calls you must follow these federal guidelines:

Inconvenient Time Rule: prohibits calling before 8am or after 9pm

Regulation F’s 7 and 7 Rule: Cannot call more than seven times within a seven-day period

Telephone Robocall Abuse Criminal Enforcement and Deterrence Act (TRACED Act) tagging legitimate businesses as spam

FCC Orders further restrict dialing to landlines and include opt-out requirements for prerecorded voice messages

But there is a more streamlined way to ensure your collection communications are following all the rules: enter code-based compliance.

COMPLIANCE: Digital-First Omnichannel

Code-based compliance works by programing rules that ensure all communications fall within all federal and state laws and regulations, such as:

Frequency and harassment restrictions

Consent requirements*

Disclosure requirements

This digitally designed approach to compliance greatly reduces the opportunities for human error that are bound to occur in more manual processes. Additionally, the digital-first approach allows companies to continue to collect during times that calling would violate certain regulations, like the Inconvenient Time Rule. In fact, 25% of payments come in after 9pm or before 8am (the determined inconvenient times), since these hours can actually be more convenient for consumers to catch-up on digital communications they received throughout the workday.

*Generally, there is no requirement in the federal law to send debt collection communications by email, though some states are more restrictive. This is not legal advice, please consult an attorney for guidance on your unique circumstance.

CONSUMER PREFERENCE: Call-and-Collect

46% of consumers want to be reached through their preferred channels—so what are today’s consumers’ preferences?

Here’s a hint: phone calls aren’t at the top of the list.

And today’s Right Party Contact rates show it, ranging between just 0.5% – 4.0%. And out of those that do answer the phone, 49.5% of consumers take no action after a collection call. The old call-and-collect tactic may actually do more harm than good if compliance rules are ignored: out of the communication tactic complaints received by the CFPB in 2020, over half complained of frequent or repeated calls.

CONSUMER PREFERENCE: Digital-First Omnichannel

So if phone calls aren’t consumers’ preferred method of communication, then what is? For 59.5% of consumers, email is their first preference when it comes to debt collection communications. This is especially important considering that first contacting a customer through their preferred channel can lead to a more than 10% increase in payments.

This digital preference isn’t surprising since nearly nine in ten Americans are now using some form of digital payments—why would they expect collections to be any different? 14% of bill-payers prioritize payments to billers that offer lower-friction payment experiences, and digital is often preferred because of it. Digital communications are easily controlled by consumers and are tightly managed by service providers with built in mechanisms to prevent harassment (like with code-based compliance), which we know has historically been a challenge for call-and-collect practitioners.

Digital-First is the Future of Collections

And it’s here today, working for TrueAccord clients and customers.

At TrueAccord, we find that more than 96% of customers resolve debts without any human interaction when digital options are offered—reducing costs associated with outbound calling, lowering risks with code-based compliance built in, and delivering an experience that consumers prefer.

Get even more statistics and data in our latest eBook — Why Evolve from Outbound Calling to Omnichannel Engagement? Cost, Compliance, & Consumer Preferences — available for download now»»

When most people think of debt collection, the word “empathy” rarely comes to mind. As a mission-driven company, we at TrueAccord, are trying to change that. We know life happens and financial anxiety has become more common than ever—especially when it comes to dealing with debt. By understanding and anticipating a customer’s needs, TrueAccord takes an empathetic approach which enables us to tailor our message and help the consumer’s journey back to financial health. With this in mind, it’s crucial for us to understand how a consumer might feel when they fall into debt.

Understanding and Engaging with the Customer

Life happens and so do delinquencies. So far, most fintechs have been good at focusing on customer experience by investing in user research and making sure that their products resonate with their target audience. However, a customer’s situation can change at the drop of a hat and with it their financial status, priorities, and motivations. When a customer, whom you thought you knew well, has an account that goes delinquent, they essentially become a stranger. Now a whole new approach is required in order to engage with this consumer.

In order to adopt the right approach to engage a delinquent account, the first thing we have to figure out is who the customer is. What are their needs? What problems do they have? Do they have special circumstances? Not only is every customer different, but every interaction you may have with that customer could be different depending on what life situation they find themselves in. So it is very important to have a broad communication strategy and be ready to meet the customer when and where they are ready to engage. This means don’t limit communication channels and have options that consumers can explore, evaluate, and select on their own time.

Leveraging Digital-First Channels

Most consumers prefer using digital channels over talking on the phone with research showing 94% of unidentified calls going unanswered. Digital channels allow people to choose when to respond without being put on the spot.

But starting a digital-first approach is not easy—it’s not just about sending emails or SMS messages to consumers. At TrueAccord we try to find the right communication channel to use for a specific consumer. We might start with a combination of email and SMS but once we get more engagement with one or the other, we’ll primarily focus on using the channel the customer engaged in.

We make sure that they’re aware of their debt and their options from obtaining more information, disputing, or evaluating payment plans all through a portal where the consumer is in control..

For consumers who do choose to set up a payment plan, we work to make sure that they have everything they need to be successful in their plan – whether that means changing the plan, the payment date, or amount, we monitor and provide content so that the consumer can effectively stay in control of their plan through successful completion – putting the consumer back in control of their own financial health while at the same time recovering for the creditor.

Using Data for a Personalized, Empathetic Experience

To truly engage consumers a successful digital strategy should go beyond a simple campaign that pushes out emails to all of your consumers at the same time every week or every other week with a generic message. Not only do you have to overcome the inboxing challenge to avoid spam filters, you need to deliver the communication at the optimal time for the consumer to open the message. And you have to have the right message, a personalized message that causes the consumer to act – to communicate back to you their intentions related to the account (dispute, full payment, payment plan, hardship, etc.).

But how do you personalize?

This is where it’s vital to leverage an understanding of your consumers. This can be done with experimentation in A/B testing consumer research, and machine learning. A/B testing and consumer research help identify what resonates with consumers and what does not. Machine learning allows personalization at scale. At TrueAccord, we rely on machine learning to continuously improve our models. We can see what digital channels, timing, and messaging each individual consumer responds best to and tailor those specific preferences to the individual journey for each consumer. We also make sure that compliance is included from the start as it needs to be regulated throughout.

For example, the best payment option is different for everyone. We provide a lot of flexibility, but we also know that showing them that flexibility up front, something that they can actually afford, will engage the customer to take the next step. Depending on the size and the age of the debt, we may show a couple of payment plans that we believe will be the most attractive to that customer along with the option to build their own payment plan. Once a customer sets up their payment plan, we send reminders when payment is due. We also have models that predict if a consumer is likely to break their payment plan based on past behavior and offer options to help keep them on track, like pushing the payment if they’re unable to pay on that date (because we understand that life happens, just like delinquencies). And as they make their payments, we celebrate their progress with them and acknowledge that they are making an effort to improve their financial situation!

The End-Product:

TrueAccord has worked with over 20 million consumers and sends over one million communications per day. For each of those communications, we’re making decisions on what to send, how to send it, and when to send it all in accordance with the legal and regulatory compliance obligations. We then use that data to continuously optimize and improve our communication method for each consumer. We’ve learned that if you’re building for the downtimes, it’s critical to realize that debt collection is a part of a consumer financial service. While our creditors are our clients, if we do what is right for the consumer (our clients’ customers), they are more likely to pay back to those creditors. A better consumer experience leads to better outcomes for all.

By incorporating an empathetic approach to debt collections, TrueAccord is able to collect more money while helping consumers with their financial situation.

Want to learn more about how your business can integrate more empathy into your collections communications? Schedule a consultation today!

Delivering communications to your customers has always been a compliance challenge with the plethora of laws, regulations, court decisions, and regulatory guidance in the debt collection space. Today with more communication channels available and regular communication from debt collection regulators—via consent orders, compliance bulletins, supervisory highlights, and even press releases—your compliance management systems and design must be flexible and easy to update.

To get expert insights on the newest compliance issues and opportunities that need to be front of mind when sending digital communications to effectively engage your customers, Associate General Counsel Lauren Valenzuela and Director of User Experience Shannon Brown teamed up to discuss the Future of Collections & Compliance in TrueAccord’s latest webinar.

Below are some of the key takeaways from their discussion, plus attendee poll results on top compliance questions.

*This blog is not legal advice. Legal advice must be tailored to the particular facts and circumstances of each unique matter.

The Current State of Compliance

Lauren Valenzuela [LV]: Needless to say, over the last 10 years the CFPB has fundamentally changed how we think about and approach compliance. That has really influenced our industry and how we think about communications in debt collection.

LV: Over the last decade the CFPB has taught us that compliance is an evolving thing. It’s not something that you can set and forget. It is something that is dynamic and that must constantly evolve and mature in order to be effective, because our environment is constantly changing.

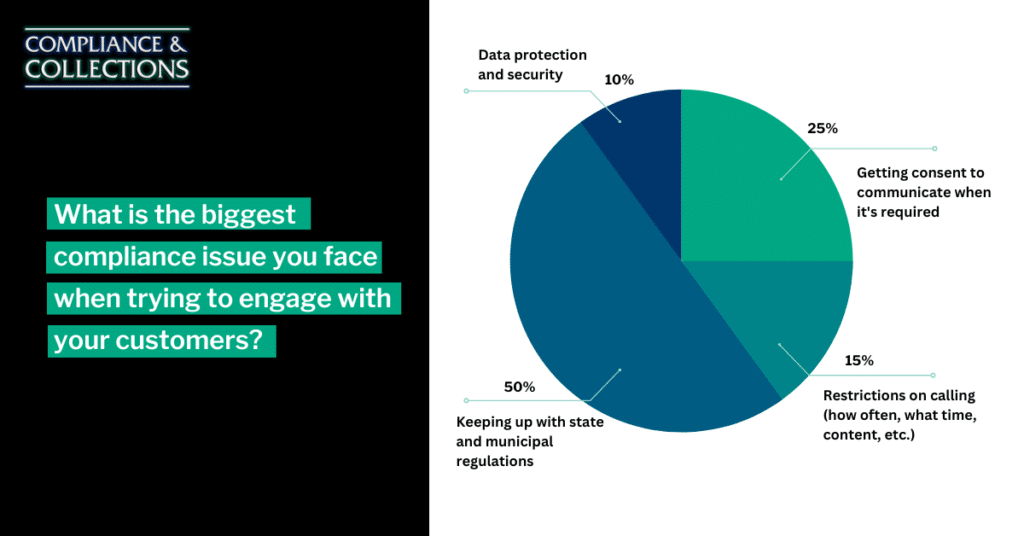

Attendee Poll Question: What is the biggest compliance issue you face when trying to engage with your customers?

Changing Consumer Preferences for Collection Communications

LV: The CFPB recently published a blog and shared that it is a “mobile first” agency, meaning that most people who visit its website are using mobile devices or smartphones. Here at TrueAccord, what does our information show about mobile usage?

Shannon Brown [SB]: Consumer mobile use has skyrocketed. In 2016, about a quarter of our consumers were using their phones to read emails and visit our website—and that number has increased to consistently above 80%. We’ve put a lot of effort into making sure our emails and website are responsive to make sure we’re meeting the needs of our consumers who are overwhelmingly on mobile. We’ve made sure our pages are able to load faster for consumers that have less stable cell connections and really made sure our interactive elements are big and optimized for tapping with a finger instead of clicking with a mouse. As far as communications, our consumer research has really shown that most consumers don’t answer the phone and want to be contacted through digital channels—they want a multi-channel experience.

LV: So we’re seeing consumers increase use in mobile phones. Even the Bureau has seen that, and we’re seeing banks increase their use of digital technologies to communicate and facilitate transactions and engage with their consumers as well.

What’s the Role of the Legal Team in Your Collections Strategy?

LV: There needs to be a partnership between compliance and pretty much all core functions, and especially at a fintech company like TrueAccord where our technology and our digital communications platform are the center of what we do to help consumers. It’s really neat to see compliance interwoven, and I think that’s reflective of its compliance management system and company culture.

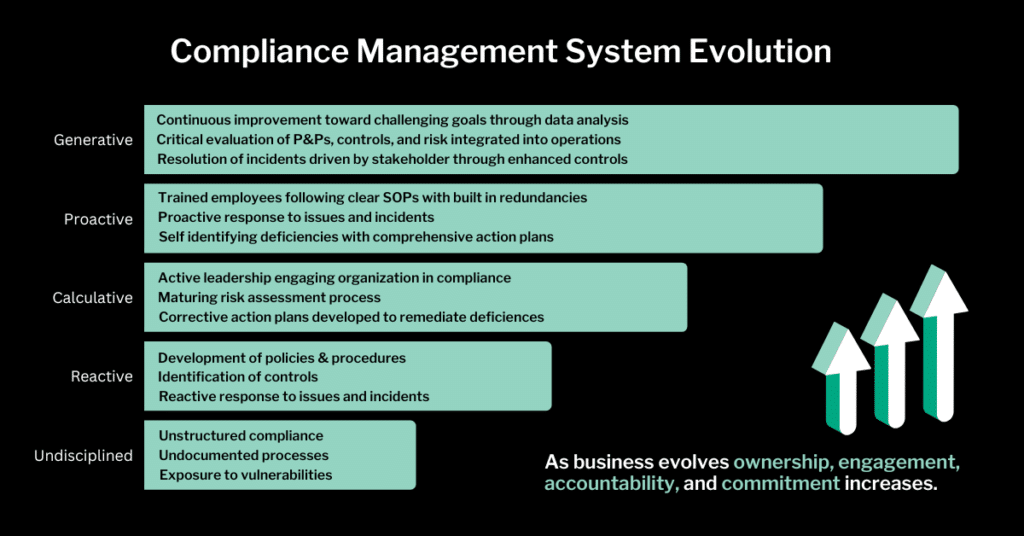

Compliance Management System Evolution

LV: Ten years ago, many collection agencies were likely in the undisciplined stage, where there was some type of compliance ongoing, but it didn’t have much structure—processes may be undocumented, potential exposure to vulnerabilities that expose themselves on lawsuits, for example.

The next iteration is reactive, meaning there is development of some policies and procedures, controls are identified, and the company is responding to issues and incidents reactively.

The next level is calculative. At this level, leadership is actively engaging the organization in compliance, risk assessment processes are maturing, corrective action plans are being developed and executed to remediate deficiencies.

This next level is proactive, meaning employees are trained and following clear policies and procedures, and such procedures have built in intentional redundancies. The organization is being proactive in identifying and responding to issues and incidents and is self-identifying deficiencies and essentially executing on comprehensive corrective action plans.

Generative means that there’s continuous improvement towards challenging goals, which are driven by data analysis. There’s critical evaluation of policies and procedures and controls, and risk is integrated in operations. Issues and incidents resolutions are driven by stakeholders and really enhanced controls.

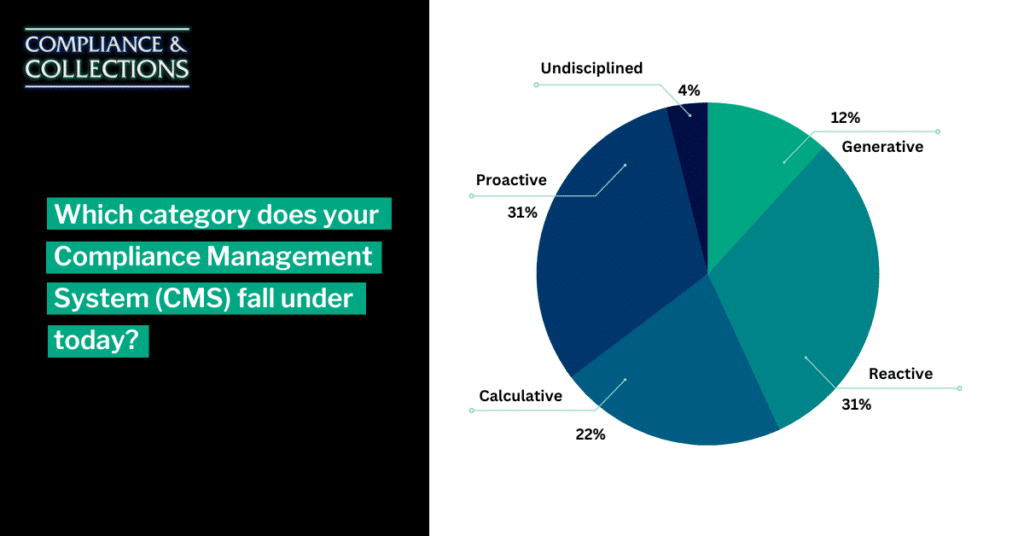

Attendee Poll Question: Which category does your Compliance Management System (CMS) fall under today?

LV: So no matter where you’re at within your compliance management system and no matter what maturity level, the important thing to remember is that you don’t have to stay there—you can evolve. We can’t stress this enough. Compliance is an evolving and dynamic thing, and should be constantly evolving to stay effective in whatever environment it is in.

The fact that TrueAccord has a well-oiled compliance management system allows us to study that climate and then figure out how to translate it and make tangible improvements in our consumers’ experience. That’s something we encourage everyone to do: think about the consumer experience and the environment you’re collecting in, because it looks remarkably different than it did five years ago for example, and we should all be evolving.

The Product Perspective

LV: How has the CFPB influenced how we develop our products here at TrueAccord?

SB: Compliance has been built into our product development life cycle. Besides frequent meetings with our compliance team for feedback and approvals throughout the life cycle, we’ve designed and built our product so we can be nimble in responding to regulatory changes, which we know happen a lot.

LV: There are numerous federal, state, and local laws. Can you give some insight into how we at TrueAccord keep up with all of that?

SB: One of the ways we efficiently keep up with the requirements is through our code-driven approach.

But what does that mean practically? It means, for example, that for any phone call coming in, our agent knows exactly what disclosures need to be given to that consumer via our system, and then gives them an opportunity to log it. It means that any email that goes out has all the necessary disclosures appended, such as out of statute disclosures, state disclosures, et cetera, and these are all kept in our code base. Not only does it take the guesswork out of the equation for our agents and our content team that’s sending communication, it reduces human error. It also means that anytime anything needs to be updated, for example, a wording in a disclosure or when a new disclosure needs to be added, we can do it in one place instead of across a variety of templates and areas of the website. We can do it in one place and then that change propagates throughout the system. This helps us to react to changes really quickly.

Our compliance team is involved in every aspect of the process. They start as educators for the whole product team—we’re all aware of regulatory considerations and know where and when we need to ask for feedback and approvals from our compliance team. So they aren’t just making sure that agents are acting compliantly, but that the product team has that knowledge as well.

And as a product team, we have this wonderful research function that’s constantly talking to consumers and trying to understand their needs and asking for feedback, which we share with our compliance team so that they can go and advocate for consumers when they are talking with regulators and legislators

Future Forecast: Where is Compliance Heading in the Collections Industry?

LV: The next iteration of compliance can be seen in some of the recent CFPB and FTC activity. Last year in 2021 for example, the CFPB published a new section of its supervision and examination manual, specifically an information technology focused compliance management review section. The Bureau is looking at any type of technologies that you may employ, like machine learning models, algorithms, or analytics.

If you’re using any kind of algorithms or machine learning to help inform any aspect of your collection strategy—or if any of your service providers are using any type of algorithms or machine learning to help provide a service to you—you must pay attention to this section of the manual because it’s incredibly informative. We’re seeing the CFPB and the FTC addressing companies’ use of data and technology, wanting to make sure that companies have proper governance and oversight of it.

All of this recent activity shows how compliance within any company, more than ever before, must really take a cross functional approach to its work in order to keep up with the evolving environment. The compliance function should not be siloed. It really needs to be in partnership with all different disciplines and functions within the organization. We’re seeing right here and now and into the future, your information technology professionals, your information security professionals, your product professionals, your engineers, your data scientists, anybody who looks, touches, thinks about data and technology should all be working with compliance

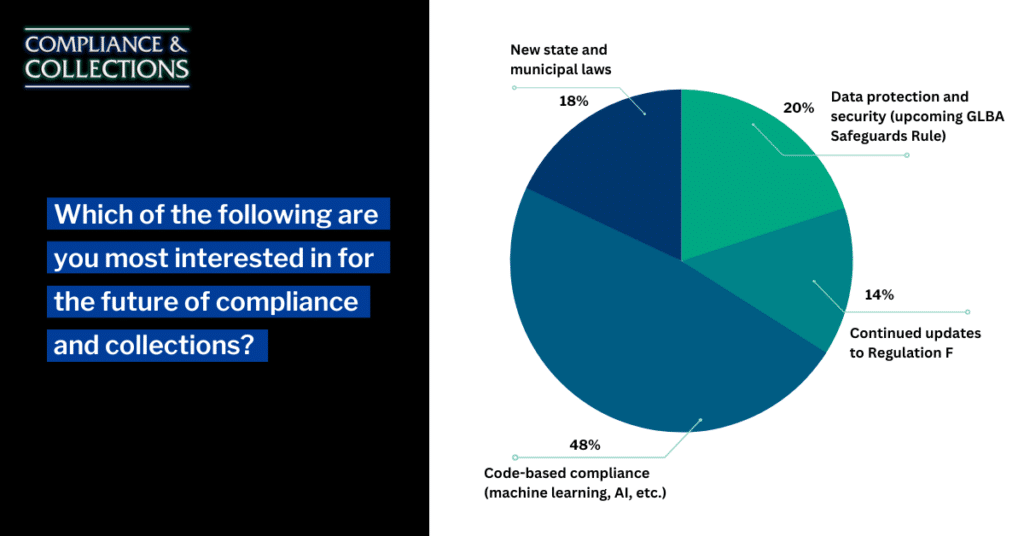

Attendee Poll Question: Which of the following are you most interested in for the future of compliance and collections?

Three Key Takeaways

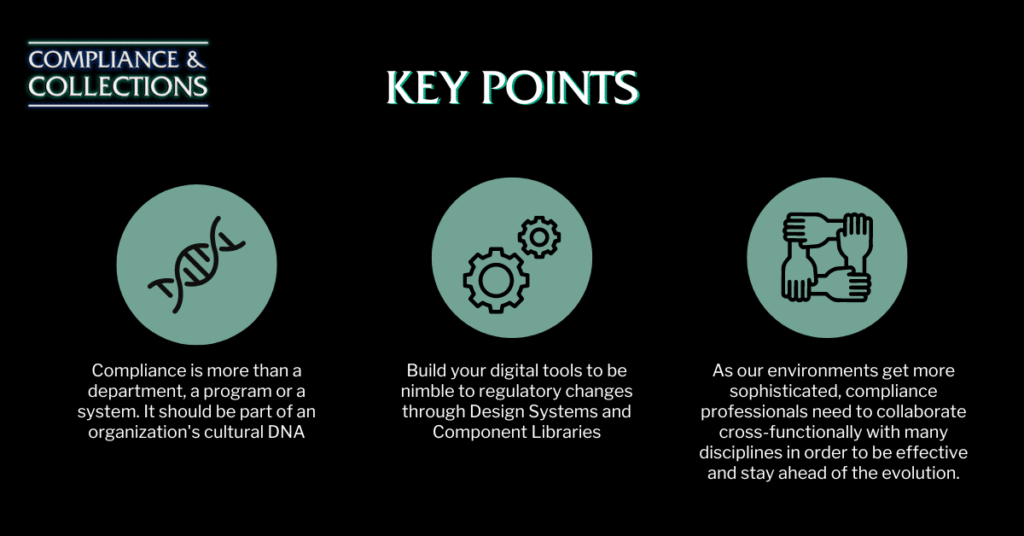

LV: Compliance is more than a department, it’s more than a program, it’s more than a system. It should be part of an organization’s cultural DNA. So when you think about compliance, wherever you are within an organization, think about how you can make it part of your organization’s DNA.

SB: Concentrate on building your tools to be nimble to the regulatory changes. Things like the design systems and the component libraries that allow you to make those changes quickly and easily, and make sure that they’re made everywhere across the system so you don’t have those older disclosures hanging out somewhere that someone forgot to change. Build your tools so you can make changes in one place efficiently.

LV: As our environments get more sophisticated around us, compliance professionals need to collaborate cross functionally more and more with other disciplines within a company to be effective and stay ahead of the evolution.The more the industry uses data and technology, we have a responsibility to make sure that it is being used in accordance with the law and best practices.

Anyone working in the collections space should be familiar with the federal Fair Debt Collection Practices Act (“FDCPA”) and its regulation, Regulation F; but did you know that there are multiple debt collection laws and regulations at the state and local level too?

State and local laws and regulations often mirror aspects of the FDCPA, however, there are a handful which are remarkably different from the FDCPA. In fact, the FDCPA makes clear that it is not designed to “annul, alter, or affect, or exempt any person” from “complying with the laws of any State with respect to debt collection practices, except to the extent that those laws are inconsistent with any provision of [the FDCPA], and then only to the extent of the inconsistency” (refer to 15 USC § 1692n). The FDCPA goes on to clarify that “a State law is not inconsistent with [the FDCPA] if the protection such law affords any consumer is greater than the protection provided by [the FDCPA].” Therefore, debt collectors collecting nationally have to grapple with and reconcile a patchwork of federal, state, and municipal debt collection laws and regulations when collecting in multiple states.

It is no simple feat to build and maintain a compliance program which keeps a debt collector in compliance with this patchwork of differing and competing debt collections laws and regulations. Debt collectors take different approaches to stay in compliance—from training their collectors on each and every state law and regulation, to deciding not to collect all together in a particular state/locality. Ten years ago when I first started in the industry, I remember compiling a job aid of all the state and local laws debt collectors had to remember and abide by—it was long and nuanced.

For example, the FDCPA explicitly permits debt collectors to speak to a consumer’s spouse without such communication resulting in a third party disclosure (see 15 USC § 1692c(d)), whereas some states such as Arizona and Connecticut are silent on this issue and other states, such as Iowa, consider spouses as third parties. In those states, a consumer must provide their consent in order for a debt collector to speak with their spouse. Another example is communication frequency limitations. While Regulation F provides parameters for call frequency (i.e., calls made in excess of 7 times in a 7 day consecutive period, and calls within 7 days of having had a phone conversation, are presumed harassing), Massachusetts has an entirely different call frequency regime. Massachusetts outright prohibits debt collectors from engaging any consumer in a communication by phone (i.e., calls and texts) more than twice in a 7 day period. While these phone restrictions are similar, they are nuanced nonetheless (e.g., one applies only to calls while the other applies to calls and texts; one in a presumption of harassment and the other is an outright prohibition, etc.) These are just a few examples to illustrate how there may be little distinctions and differences between the FDCPA/Regulation F and state/local laws.

In an effort to simplify how many rules debt collectors have to learn and abide by, some debt collectors design and adopt policies which reconcile as many of the laws and regulations as it can for a particular topic. For example, choosing to adopt the strictest law/regulation as a company policy so that it applies across the board is one strategy some companies may adopt. While this approach will help a debt collector meet or exceed a state law requirement, this approach can unnecessarily limit a debt collector’s ability to communicate and/or collect in more places than necessary, thereby undermining those state economies that have no such restrictions.

While the patchwork may seem daunting, this is an area ripe for compliance innovation—where technology can be leveraged to automate controls and guardrails. For example, instead of requiring debt collectors to memorize multiple state laws/regulations, controls can be designed to automate guardrails for state laws in a collection system. Here at TrueAccord, compliance has a close partnership with its product and engineering teams, to help leverage technology when laws and regulations are introduced or changed. While technology will not replace a compliance monitoring team, it has the potential to increase the efficiency and efficacy of any human monitoring by helping front line agents understand their state by state requirements and compliance teams focus their auditing and monitoring efforts.

*Lauren serves as TrueAccord’s Associate General Counsel. This blog is not legal advice. Legal advice must be tailored to the particular facts and circumstances of each unique matter.

Just as technology has evolved leaps and bounds, so have consumer communication preferences, especially when it comes to debt collection. The Consumer Financial Protection Bureau (CFPB) recognized in Regulation F—rules updating the Fair Debt Collection Practices Act (FDCPA)—that consumers in debt want to communicate with debt collectors through digital channels, like email and SMS.

Under the FDCPA, Regulation F, and other state laws, these digital channels have the same compliance requirements as calls, such as no harassment or abuse, no false or misleading representations, and no unfair practices. Even though these additional channels have the similar compliance requirements, businesses must still manage these requirements across all channels and have the capacity to update requirements as new laws are passed, new cases come out, and new guidance is released from regulators causing a need to change in a compliance practice. How can businesses ensure compliance through the evolving regulatory landscape?

Code-based compliance is a critical component for the debt collection industry.

We interviewed five key stakeholders in this process to get different perspectives on what code-based compliance is and how it benefits businesses, lenders, consumers, and auditors. Read below for insights from: Eric Nevels, Director Operational Excellence; Hal Eisen, VP Engineering; Kelly Knepper-Stephens, Chief Compliance Officer and General Counsel; Michael Lemoine, Director Client Success; and Milo Onken, Director Quality Assurance.

What is Code-Based Compliance?

Eric Nevels: When an algorithm is used to help make decisions on consumer communications in debt collection, a code-based compliance system would be coded into that algorithm or work side-by-side with the algorithm to ensure that all digital communications fall within federal and state laws and regulations.

Michael Lemoine: Here’s an analogy to help explain code-based compliance: You lace up your new running shoes. You scoured all the online reviews and this pair provides the best ankle support. You ate a light but fuel packed breakfast, no mid run slump for you. You eyed the weather app on your phone, all clear and perfect temp. Hydrated, check. Headphones, check. Mood, great! You’ve got this, everything is under control and accounted for. Off…you… go!

Even if you’re not a big runner this sounds like a safe and productive way to start a day. But what if instead of checking for rain and eating a little oatmeal to make sure you had a good jog, you had to manually complete a full body diagnostic and perform microsecond electrical and chemical adjustments to your body just so you didn’t become disabled or even die while getting a little exercise? Not so safe and productive now. Is the risk of immediate death worth the effort and small reward of a single run?

Every second your body automatically, without thought or effort, reads your current condition and reviews thousands of risks and initiates controls, responses, and actions to keep you alive—called the autonomic nervous system. Code-based compliance is the autonomic nervous system of an organization’s risk and control program. Now, it’s not as dramatic as life and death, but code-based compliance can supercharge any compliance management system because once the code has been programmed and deployed the system always follows the programmed rules leading to consistency and accuracy.

How is Code-Based Compliance Different From More Traditional Approaches to Compliance?

Eric Nevels: In the absence of code, human beings would need to check against the various restrictions on communications. Anytime humans are involved, even with rules and procedures in place, it is possible for errors to occur. With a code-based system, it is impossible for that action to take place.

Kelly Knepper-Stephens: Certainly it’s better than manual compliance because with manual compliance you have an opportunity for human error. But it doesn’t mean that code-based compliance is “code it and forget it.” Your coders need a process to quality check the code. And your compliance team or a front line control team needs to monitor to make sure the coded compliance rules are working as you intended them to work.

How Does This Approach Benefit Collection Compliance Strategies?

Hal Eisen: Code-based compliance is great because it never gets tired or distracted and is not subject to any of the other human frailties. Done correctly, it can be efficiently applied to a wide range of software products without needing additional investment. Most compliance rules were written for the benefit of consumers. The better we comply, the safer consumers are. Consumers should have accurate disclosures, fewer annoying interactions and feel better about the whole experience.

Eric Nevels: Lowers operational risk and ensures compliance with regulations. Additionally, it is much easier to update the code when regulations are changed. It helps ensure that they are being treated within the bounds of the law, which is their benefit.

Milo Onken: The code-based approach ensures accuracy and tangible evidence for compliance audits. Collaboration with different internal teams and Legal ensures we check, implement, and follow industry compliance directives.

A Code-Driven Future for Debt Collection

Code-based compliance offers predictable and consistent collections methods when coupled with digital platforms. New technology can be mistaken as a risky investment, but digital debt collection systems offer more compliance security and more transparency—for consumers and creditors. Digital collection solutions not only evolve to meet consumer needs, but they can also continually adapt to changing regulations and quickly meet compliance requirements.

Beyond code-based compliance, what are compliance issues unique to collections that need to be front of mind when sending digital communications to effectively engage your customers?

Join us Thursday September 29th at 1pm ET for our interactive webinar, The Future of Collections & Compliance, hosted by TrueAccord Associate General Counsel Lauren Valenzuela and Director User Experience Shannon Brown.

Reserve your space now for an interactive discussion on:

Cutting edge digital collection compliance

The role of the legal team in creating a digital collection strategy

TrueAccord is a machine-learning and Al-driven 3rd-party debt collection company that is reinventing debt collection. We make debt collection empathetic and customer-focused and deliver a great user experience.

Our digital-first approach to debt collection creates a cycle of collections growth:

1. Improve the perception of the industry

2. Provide a personalized experience

3. Build brand equity and collect