TrueAccord is proud to announce that Katie Neill, its General Counsel & Chief Compliance Officer, has been appointed to the Debt Collection Advisory Committee of the California Department of Financial Protection and Innovation (DFPI) for the 2025-2027 term.

This board is comprised of seven members who provide feedback to the DFPI for its debt collection licensing program. The diverse group includes a consumer advocate and representatives from the debt collection, debt-buying, third-party collection, and collection law industries. The committee advises the Commissioner on matters related to the debt collection business, including proposed fee schedules and other requirements.

TrueAccord has been previously represented in this group when its founder, Ohad Samet, served on the inaugural Debt Collection Advisory Committee in 2021. As the debt collection industry has evolved to meet consumer needs and technological advancements, the DFPI has focused on better protecting California consumers, promoting responsible innovation, reducing regulatory uncertainty for emerging financial products, and increasing education and outreach to vulnerable groups.

As a leader in digital-first debt collection, TrueAccord is invested in reinventing the industry for technology-enabled and consumer-friendly outreach that fundamentally changes the approach to debt collection. In her role at TrueAccord, Katie is instrumental in shaping the policies and controls necessary to ensure legal and regulatory compliance amidst the innovation that drives business goals.

“It’s an honor to be appointed to the Debt Collection Advisory Committee and have an opportunity to impact the future of consumer finance regulation in California,” said Katie Neill. “I look forward to contributing my expertise in consumer-focused, technology-driven debt collection practices to support the DFPI’s mission of protecting consumers and fostering responsible innovation within the industry.”

About TrueAccord

TrueAccord is the trusted industry leader in third-party debt collection, leveraging data science and technology to deliver superior results and a best-in-class consumer experience. Since 2013, TrueAccord has served more than 40 million consumers in debt with a more humane collection experience while delivering unmatched liquidation rates as the leader in digital-first collections for the Buy Now Pay Later, fintech, telecommunications and credit union industries, among others. Visit www.trueaccord.com and follow on LinkedIn to learn more.

What do canceled hair appointments and increased lipstick and beer sales have in common? These untraditional indicators, among other discretionary expenditure trends, often show consumer sentiments around finances well before a recession hits. Coming out of 2024, the average U.S. household owed $11,303 on credit cards, and while credit card charge-off rates and delinquencies both declined slightly, experts are not declaring a definitive turnaround given the ongoing economic uncertainties and high balances. Consumers today are confronted with new developments regularly, leading to “considerable turbulence” in the words of JPMorgan Chase CEO Jamie Dimon, and without much guidance on what the implications are for their personal financial outlook, which understandably affects their spending and budget considerations.

The main challenge in engaging with consumers in debt in today’s economic climate is how to offer them an affordable way forward. Other challenges for businesses’ debt collection operations come in the forms of regulatory changes impacting innovation and uncertainty about staying in compliance.

As you try to keep up with your bottom line in a rapidly evolving consumer financial landscape, let’s look at what you should consider as it relates to debt collection moving forward in 2025.

What’s Impacting Consumers?

It’s important to note that this report is from data covering a period of time before the majority of new tariffs went into effect, and everyone from Wall Street to consumers are waiting to see what happens next. Against a backdrop of an erratic market and general unease about the future of the U.S. economy, inflation reports offered a bright spot showing cooling in March to close out Q1. The consumer price index (CPI), excluding volatile food and energy costs, increased 0.1% from February, climbing 2.4% from a year earlier—the least in nine months and lower than expected. The overall CPI declined 0.1% from a month earlier, the first decrease in nearly five years, reflecting a decline in energy costs, used vehicles, hotel visits, car insurance and airfares.

The overall jobs numbers from March signaled a solid labor market, with employers adding 228,000 jobs and the unemployment rate changing little to 4.2%. Job gains showed up

in health care, social assistance, transportation and warehousing, along with retail trade, which reflected the return of workers from a strike, while federal government employment declined as a result of wide-reaching layoffs.

The Federal Reserve (Fed) held rates steady at 4.25-4.50% in March. In its statement following the March meeting, the Fed stated that “uncertainty around the economic outlook has increased.” As a result, the Fed lowered economic growth expectations to 1.7% gross domestic product (GDP) growth in 2025, down from a 2.1% estimate, while upping the projected core PCE inflation rate to 2.8% from 2.5%. The next meeting is on May 6 and while many still expect two rate cuts this year, the outcome will reflect the bank’s outlook given the new landscape of tariffs and their anticipated impact on inflation.

In February, the Fed released its Quarterly Report on Household Debt and Credit for Q4 2024, which showed total household debt increased by $93 billion in Q4, to $18.04 trillion. The report also showed that people are having more trouble paying off that debt, with credit card balances increasing by $45 billion to $1.21 trillion and auto loan balances increased by $11 billion to $1.66 trillion. Delinquency rates ticked up 0.1% from the previous quarter, with 3.6% of outstanding debt now in some stage of delinquency. Transition into serious delinquency, or 90+ days past due (DPD), also increased for auto loans, credit cards and HELOC balances.

Experian’s Ascend Market Insights from February 2025 data showed that overall delinquent balances (30+ DPD) increased by 16.67%, driven by a 537.4% increase in delinquent student loan balances, a 16.28% increase for first mortgages and a 4% increase for bankcard balances. The huge surge in delinquent student loans is due to an increase in the volume of 90 DPD data furnishers have started to report after the pause on student loan payments ended.

By the end of February, nearly 8 million people with student loans had missed resumed payments and were met with plunging credit scores. As it stands, 1 in 5 people who are supposed to be making payments on their federal student loans are more than 90 DPD, nearly double the percentage of delinquent borrowers since the pandemic hit and the government paused payments, with reasons for delinquency ranging from inability to pay and difficulties working with servicers to missed communications that never reached the recipient.

The CFPB, Regulations and Compliance are Evolving

While the Consumer Financial Protection Bureau’s (CFPB) normal activity has been disrupted due to changes in direction from the administration, it did release a report looking at national rental payment data from September 2021 to November 2024 showing that the percentage of renters who paid late fees in the last year reached 23% in February 2023. While the rate had declined to slightly less than 14% in November 2024, the CFPB’s analysis found that the median outstanding rental balance rose 60% between September 2021 and November 2024, suggesting increased financial distress among affected households.

Meanwhile, the Federal Communications Commission (FCC) is seeking public input on identifying FCC rules for the purpose of alleviating unnecessary regulatory burdens. In a public notice released March 12, 2025, the FCC announced the Commission is seeking comments on deregulatory initiatives to identify and eliminate those that are unnecessary in light of current circumstances. The FCC notice stated: “in addition to imposing unnecessary burdens, unnecessary rules may stand in the way of deployment, expansion, competition, and technological innovation.”

In the meantime, two FCC Orders about the Telephone Consumer Protection Act (TCPA), which applies only to calls and texts made by an automated telephone dialing system (ATDS) and prerecorded or automated voice calls (aka robocalls or robotexts) come into effect. First, a 2024 Order released last February impacting revocation of consent to receive autodialed calls and texts and prerecorded or artificial voice calls. The 2024 Order conflicts with the CFPB’s Regulation F Debt Collection Rule about the scope of an opt-out. Second, is a 2025 Order released this past February aiming to strengthen call blocking of illegal calls, which may result in the blocking of lawful debt collection calls and texts.

Debt collectors and other companies impacted by these two orders may want to submit comments to the FCC identifying the particularly burdensome aspects that could be revisited and slightly revised to be consistent with consumer preference, consistent with other laws and regulations (like Regulation F), and less burdensome on companies.

Eyes will continue to be on the developments with the ever-evolving regulatory landscape and what happens with the CFPB, which will impact how businesses both comply with regulations and innovate through technology in consumer financial services.

Consumer Sentiment

The Fed’s March Survey of Consumer Expectations showed that inflation expectations increased by 0.5% to 3.6% at the one-year-ahead horizon while consumers’ expectations about their households’ financial situations deteriorated with the share of households expecting a worse financial situation one year from now rising to 30%, the highest level since October 2023. The report also showed Unemployment, job loss, earnings growth and household income growth expectations also deteriorated.

The latest University of Michigan consumer sentiment survey showed that sentiment fell to 50.8, down from 57.0 in March. The drop, a 10.9% monthly change and 34.2% lower than a year ago, was the lowest reading since June 2022 and the second lowest in the survey’s history since 1952. Respondents’ expectation for inflation a year from now jumped to 6.7%, the highest level since 1981. The current economic conditions index and expectations measure dropped by 11.4% and 10.3% from March respectively.

Similarly, the Conference Board’s Consumer Confidence Index in March fell by 7.2 points to 92.9. The Present Situation Index, based on consumers’ assessment of current business and labor market conditions, also decreased 3.6 points to 134.5 while the Expectations Index based on consumers’ short-term outlook for income, business and labor market conditions fell 9.6 points to 65.2, the lowest level in 12 years and well below the threshold of 80 that usually signals a recession ahead.

What Does This Mean for Debt Collection?

All of the economic indicators and pessimistic consumer outlook, especially given stock market turbulence that impacts many Americans’ retirement savings, makes it likely that consumers across all income brackets will pull back on discretionary spending. And for those already financially stressed, the added burden of increased inflation due to tariffs could make it harder for budgets to meet debt obligations. For lenders and collectors, here are some recommendations for your debt collection strategy in 2025:

Ensure Your Messages Are Getting Through. If you’re calling someone who prefers to receive information by email, they likely won’t answer and get your message. Similarly, if you’re using digital channels and your email gets caught in a spam folder, your message won’t make it to the intended recipient. Best practices for email delivery and deliverability are just as important as using the right channel. Ensure your collection partners who claim to engage consumers via email can back it up with the metrics to prove that their messages actually make it through.

Do More With Less. Technology exists today that can create efficiencies across many aspects of debt collection operations, which means increasing account volume doesn’t have to equal higher costs. Look for ways you and your collection partners can leverage new tech to streamline operations and you can reap the benefits of improved operational efficiency, compliance efforts and consumer experience.

Get Your Lawyer on Speed Dial. Or ensure your debt collection partner is keeping tabs on the rapidly evolving regulatory and compliance landscape to inform their practices. There’s a lot going on, quickly, and if you miss something the repercussions of noncompliance could cost you financially or reputationally.

For consumer engagement in debt collection, many organizations and agencies have moved away from outbound calling—but don’t discount reaching out to consumers’ phones just yet! Text messaging (referred to as SMS or short message service) is becoming a favored method for consumers to receive business communications.

It’s common knowledge these days that people tend to ignore phone calls from unknown numbers and often throw away physical letters without opening them, but they will also delete unfamiliar emails without reading them, too.

So if your digital communication strategy only includes email, consider this: consumers are nearly twice as likely (1.8x) to prefer texting to any other communication method. Gartner reports SMS open and response rates as high as 98% and 45%, respectively, compared to corresponding figures of 20% and 6% for email.

For successful debt collection operations, adding SMS into the digital mix to build an omnichannel approach (along with email, calling, letters, and self-serve options) boosts engagement and liquidation rates.

Why is SMS Critical in Collection Communications?

SMS allows creditors, debt collectors, and financial institutions to communicate with individuals in a brief and direct manner, more so than traditional methods such as letters or phone calls—or even email. SMS is a powerful tool for debt collectors looking to engage with consumers who might otherwise avoid other forms of communication. These messages can serve a variety of purposes, from notifying debtors of outstanding payments to reminding them of upcoming due dates or offering payment plan arrangements.

SMS offers several practical advantages for both debt collectors and consumers. The concise nature of SMS—limited to 160 characters—forces communication to be direct and to the point, ensuring that messages are clear and easy to understand. Consumers who may feel overwhelmed by lengthy phone conversations or complex emails often appreciate this streamlined approach.

Surveys have found that 85% of consumers state that they prefer to receive an SMS instead of an email or phone call and more than 55% said they prefer text messaging because it’s immediate, convenient, and allows them to quickly get updates—and that’s just the beginning of consumer preference statistics surrounding SMS communication:

65% want their accounts, billing, and payment reminders sent to them as a text

89% say they prefer texting with businesses over any other mode of communication

97% of companies that have launched texting initiatives say those initiatives help them communicate with consumers more efficiently

And studies of overall communications from businesses show that consumers are 134% more likely to respond to a text than an email.

According to the Pew Research Center, 97% of Americans own a cell phone, and nearly the same percentage sends at least one text message each day, making SMS an already well-established communication method most consumers are familiar and comfortable with. By using SMS to reach out to delinquent consumers, debt collectors tap into a channel that’s not only widely accessible but also highly effective in terms of response and engagement. With its speed, convenience, and familiarity, expanding digital strategies to include SMS is critical for consumer preference.

Along with this preference and the corresponding better engagement rates, compliance is one strong case for using SMS in consumer engagement for collections. The implementation of Regulation F by the Consumer Financial Protection Bureau (CFPB) has helped modernize the Fair Debt Collection Practices Act (FDCPA) by focusing on electronic communications and giving guidance on how to properly use SMS as a channel.

SMS provides consumers with links directly to account portals where consumers can get more information, pay, dispute, etc. at a time that is convenient for them and without having to talk to an agent.

“This is my first time paying off a debt collection online by just receiving a text. I just received a text from the debt collector and I made a payment arrangement just by a few clicks. This way is just so much better and easier.” – Real feedback from consumer working with TrueAccord

Positive consumer feedback is just one part of the TrueAccord difference for this channel. TrueAccord goes beyond just adding SMS into the mix—our team digs deeper to ensure the best possible engagement in this channel. Similar to email deliverability, TrueAccord teams track SMS reachability, or the likelihood that a text message sent by a business actually reaches the intended recipient’s mobile device.

And just like with every approach in our omnichannel strategy, our machine learning decision engine, HeartBeat, guides optimal communication with the right message, right time, and right channel. From reminders to direct calls-to-action, SMS offers many benefits for both consumers and businesses thanks to the speed, convenience, and higher engagement rates towards debt resolution.

Looking at key economic indicators—GDP growth, consumer spending, softening inflation and a healthy job market—it would be easy to deduce that consumers in America are faring well. But digging deeper reveals unwieldy debt, expected rises in charge-offs and uncertainty around future economic conditions, painting a less rosy picture of the financial situation.

Consumers certainly faced challenging economic conditions in 2024, but despite record-high credit card balances and delinquency rates, Americans continued spending, accumulating even more debt this holiday season. Data shows that more than a third of shoppers took on additional debt for the holidays, borrowing $1,181 on average, and that 47% of consumers still carried debt from the 2023 holiday season. With inflation proving more sticky than policymakers had hoped and uncertainty around how the new administration’s policies might affect it, it may take longer for people to see lower interest rates on their mortgages, car loans and credit card balances, which could prove challenging to household budgets.

The good news for lenders and debt collectors is that a reported 72% of consumers have a New Year’s resolution to pay off debt in 2025. The challenges will be effectively engaging consumers who want to repay and accommodating their strained budgets. We are entering a year of unknowns across the board, from potential regulatory changes to economic fluctuations to varying consumer sentiments, and there’s a lot to consider as it relates to debt collection in 2025.

What’s Impacting Consumers?

While inflation isn’t cooling dramatically, it also isn’t showing signs of speeding back up. December’s inflation reading didn’t bring any big surprises to close out 2024—the consumer price index (CPI) increased 0.4% on the month, putting the 12-month inflation rate in line with forecasts at 2.9%. The core CPI annual rate, which discludes volatile food and fuel prices and is a key factor in policy decisions, notched down to 3.2% from the month before, slightly better than forecasted.

Despite the nagging inflation and still-elevated borrowing rates, the job market remains resilient, with employers adding 256,000 jobs in December, nearly 100,000 more than economists expected. The unemployment rate in December ticked down to 4.1%, lower than the forecasted steady rate.

The Federal Reserve started cutting rates in September 2024 and lowered its benchmark for a third straight month in December based on signs that the economy was slowing down. But the healthy December jobs report combined with lingering inflation supports the Fed’s intention to move forward with a slower pace of rate cuts this year—it is now penciling in only two quarter-point rate cuts in 2025, down from the four it forecasted in September.

In November, the Fed released its Quarterly Report on Household Debt and Credit for Q3, which showed total household debt increased by $147 billion (0.8%) in Q3 2024, to $17.94 trillion. The report also showed that credit card balances increased by $24 billion to $1.17 trillion, with the average U.S. household owing $10,563 on credit cards going into the Q4 holiday shopping season. According to Experian’s Ascend Market Insights, at the end of November, 5% of consumers had total balances over their limits and 11% of consumers had a high utilization of 81-100%.

Experian’s Ascend Market Insights from November also showed overall delinquent balances (30+ DPD) decreased by 3.78% while up on unit basis by 1.61%. This net was driven by decreases in delinquent first mortgage and unsecured personal loan balances, which were offset by increases in delinquent bankcard balances and on a dollar basis in delinquent second mortgages.

Meanwhile, millions of Americans may see significant changes to their credit reports in the coming months if they have either unpaid medical bills or student loans, but the effects of each are opposite.

Since March 2020, delinquent student loan borrowers have been exempt from credit reporting consequences, but the required payments resumed in October 2024. As a result, an estimated 7 million borrowers who have fallen behind on their federal student loan payments or remain in default will start seeing negative credit reporting in the coming months if they don’t resume payments.

Conversely, for the roughly 15 million Americans with unpaid medical bills, a new rule from the Consumer Financial Protection Bureau (CFPB) will ban and remove at least $49 billion in medical debt from consumer credit reports and prohibit lenders from using medical information in their lending decisions, providing a boost to credit scores and financial access.

CFPB Looks at Medical Debt, Student Loans and So Much Data

Medical debt wasn’t the only focus for the Consumer Financial Protection Bureau in Q4. In addition to specific actions targeting offenders in the consumer financial services industry, the CFPB announced myriad other topics of interest to close out 2024 with a sharp focus on protecting consumers and their data.

At the end of October, the CFPB finalized a personal financial data rights rule that requires financial institutions, credit card issuers and other financial providers to unlock an individual’s personal financial data and transfer it to another provider at the consumer’s request for free, making it easier to switch to providers with superior rates and services. The rule will help lower prices on loans and improve customer service across payments, credit and banking markets by fueling competition and consumer choice.

In November, the CFPB issued a report detailing gaps in consumer protections in state data privacy laws, which pose risks for consumers as companies increasingly build business models to make money from personal financial data. The report found that existing federal privacy protections for financial information have limitations and may not protect consumers from companies’ new methods of collecting and monetizing data, and while 18 states have new state laws providing consumer privacy rights, all of them exempt financial institutions, financial data, or both if they are already subject to the federal Gramm-Leach-Bliley Act (GLBA) and the Fair Credit Reporting Act (FCRA).

Then, the Bureau finalized a rule on federal oversight of digital payment apps to protect personal data, reduce fraud and stop illegal debanking. The new rule brings the same supervision to Big Tech and other widely used digital payment apps handling over 50 million transactions annually that large banks, credit unions and other financial institutions already face.

As 28 million federal student loan borrowers returned to repayment, the CFPB issued a report uncovering illegal practices across student loan refinancing, servicing and debt collection, identifying instances of companies engaging in illegal practices that misled student borrowers about their protections or denied borrowers their rightful benefits. This followed the release of their annual report of the Student Loan Ombudsman, highlighting the severe difficulties reported by student borrowers due to persistent loan servicing failures and program disruptions.

Uncertainty in Consumer Sentiment

The Fed’s Survey of Consumer Expectations from December showed that inflation expectations were unchanged at 3.0% for this year, increased to 3.0% from 2.6% at the three-year horizon, and declined to 2.7% from 2.9% at the five-year horizon. Reported perceptions of credit access compared to a year ago declined as did expectations about credit access a year from now. Additionally, the average perceived probability of missing a minimum debt payment over the next three months increased to 14.2% from 13.2% and was broad-based across income and education groups.

The November PYMNTS Intelligence “New Reality Check: The Paycheck-to-Paycheck Report” found that from September to October 2024, the share of consumers living paycheck to paycheck overall rose slightly from 66% to 67%. Surveyed cardholders said their outstanding credit balance is either holding constant or increasing—25% said their outstanding balance increased over the last year, while 55% said it stayed about the same. Moreover, many consumers, and especially those having trouble paying their monthly bills, report maxing out their cards regularly and using installment plans to cover basic necessities.

According to NerdWallet’s 2024 American Household Credit Card Debt Study, more than 1 in 5 Americans who currently have revolving credit card debt (22%) say they generally only make the minimum payment on their credit cards each month. And with credit card rates averaging 20%, interest costs could almost triple the average debt for those making minimum payments after factoring in interest expenses.

The University of Michigan’s index of consumer sentiment dropped to 73.2 at the start of January 2025 from 74.0 in December after views of the economy weakened on expectations of higher inflation in light of the new administration’s proposed tax cuts and new import tariffs. Unlike some of the polarization of recent months, which had seen more positive responses among Republicans than Democrats, January’s deterioration in economic expectations was seen across political affiliations. While consumers’ views of their personal finances improved about 5%, their economic outlook fell back 7% for the short run and 5% for the long run, with year-ahead inflation expectations jumping to 3.3%, up from 2.8% in December and the highest since May last year.

What Does This Mean for Debt Collection?

Over the next 12 months, debt collection companies expect an increase in account volume but a potential decrease in account liquidity, according to TransUnion’s latest Debt Collection Industry Report. If the goals are implementing strategic operational efficiencies and improving the consumer experience to facilitate debt repayment, the means to the ends include investing in technologies like artificial intelligence, solving for scalability, and optimizing communication channels and consumer self-service engagement. For lenders and collectors, here are some recommendations for your debt collection strategy in 2025:

Scalability, Go Big or Go Home. Higher account volume calls for operations that can scale cost-effectively while offering the right consumer experience. Embracing smart technology is your best bet to keep up, and figuring out when to buy tech-enabled products and services versus when to invest in building it yourself will be key to making it work.

Reduce Friction for Consumers.Self-service portals in collections reduce friction and foster a sense of autonomy for consumers to manage their debt without the pressure or inconvenience of interacting with a call center agent. Besides creating a more streamlined experience for the consumer, organizations will also benefit from associated cost-savings, compliance controls and scalability.

Compliance Changes, Adapt or Perish. The debt collection industry experienced notable legal and compliance changes in 2024, including important litigation outcomes and updates to digital communications regulations, and keeping up with more changes to come will be critical to your business. Join our Legal and Compliance Roundup webinar on Jan. 29 to learn about the latest developments and how they will shape strategies and industry practices in 2025. Register here: https://bit.ly/4h4tacd

The big inflation situation plaguing the U.S. for the past three years seems to be coming to an end, and it could be that American consumers are partially to thank. Tired of paying higher prices, consumers increasingly turned to cheaper alternatives, bargain hunted or simply avoided items they found too expensive, pressuring retailers to accommodate them or lose their business. That’s not to say Americans have stopped spending altogether—the economy continues to expand and people continue to struggle against inflated prices for necessities across the board, often still turning to credit cards to make ends meet.

With consumers setting the demand amidst elevated prices and inflation declining slowly, retailers have gotten an even earlier jump on holiday promotions this year in the hopes of boosting sales in a price-wary environment. Spreading holiday expenses out over a longer period of time may ease the financial burden slightly, but the cumulative dollars spent will still weigh heavily on consumer finances for Q4 and rolling into 2025. The National Retail Federation is forecasting that winter holiday spending is expected to grow between 2.5% and 3.5% over last year, with a total reaching between $979.5 billion and $989 billion.

We are starting to feel an economic shift, but what does this all mean and what’s the outlook for the end of the year? Read on for our take on what’s impacting consumer finances, how consumers are reacting and what else you should be considering as it relates to debt collection today.

What’s Impacting Consumers?

While not the straight line decline economists would like to see, the September results show that inflation is slowly and steadily easing back to the Federal Reserve’s 2% target. After several months of decreasing inflation and amid slowing job gains, the Fed in September announced the first in a series of interest rate cuts, slashing the federal funds rate by 1/2 percentage point to 4.75-5%. Federal Reserve Chair Jerome Powell indicated that more interest rate cuts are in the plans but they would come at a slower pace, likely in quarter-point increments, intended to support a still-healthy economy and a soft landing.

The rate cut plans have been made possible by consistently declining inflation. The Consumer Price Index rose just 2.4% in September from last year, down from 2.5% in August, showing the smallest annual rise since February 2021. Core prices, which exclude the more volatile food and energy costs, remained elevated in September, due in part to rising costs for medical care, clothing, auto insurance and airline fares. But apartment rental prices grew more slowly last month, a sign that housing inflation is finally cooling and foreshadowing a long-awaited development that would provide relief to many consumers.

The September jobs report supported the economic optimism by adding a whopping 254,000 jobs, far exceeding economists’ expectations of 140,000. The unemployment rate lowered to 4.1%, below projections of remaining steady at 4.2%. The government has also reported that the economy expanded at a solid 3% annual rate Q2, with growth expected to continue at a similar pace in Q3. This combination of downward trending interest rates and unemployment plus an expanding economy is great news for consumers and businesses alike, and can’t come soon enough for many financially strained Americans.

Coming out of Q2, total household debt rose by $109 billion to reach $17.80 trillion, according to the latest Quarterly Report on Household Debt and Credit. This increase showed up across debt types: mortgage balances were up $77 billion to reach $12.52 trillion, auto loans increased by $10 billion to reach $1.63 trillion and credit card balances increased by $27 billion to reach $1.14 trillion.

Unsurprisingly, delinquency and charge-off rates ticked up as consumers struggled against still relatively high prices and interest rates. In mid-September, shares of consumer-lending companies slid after executives raised warnings about lower-income borrowers who are struggling to make payments. Delinquency transition rates for credit cards, auto loans and mortgages all increased slightly, with a steeper increase in flow to serious delinquency for credit cards, up more than 2% over last year from 5.08% to 7.18%. This kind of delinquency can be especially difficult for consumers to recover from given the record-high credit card rates many are stuck with.

While still low by historical standards, the mortgage delinquency rate was up 3 basis points in Q2 from the first quarter of 2024 and up 60 basis points from one year ago. The delinquency rate for mortgage loans increased to a seasonally adjusted rate of 3.97% at the end of Q2, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey, an increase that corresponded with a rise in unemployment and showed up across all product types.

For those with student loans, September marked the end of the ‘on-ramp’ to resuming payments, which was the set period of time that allowed financially vulnerable borrowers who missed payments during the first 12 months not to be considered delinquent, reported to credit bureaus, placed in default, or referred to debt collection agencies. However, the grace period is over and anyone who doesn’t resume making student loan payments in October risks a hit to their credit score—we will see these delinquencies reported in Q4.

Financial Protection for Consumers Across the Board

The Consumer Financial Protection Bureau (CFPB) continued with a high level of activity through the summer. Along with taking action against more than a handful of financial services companies in the name of consumer protection, the agency made headway on myriad other issues.

To kick off Q3, the CFPB published Supervisory Highlights sharing key findings from recent examinations of auto and student loan servicing companies, debt collectors and other financial services providers that found loan servicing failures, illegal debt collection practices and issues with medical payment products. The report also highlighted consumer complaints about medical payment products and identified concerns with providers preventing access to deposit and prepaid account funds.

Then, the CFPB and five other agencies issued a final rule on automated valuation models. The agencies, including the OCC, FRB, FDIC, NCUA, and FHA designed the rule to help ensure credibility and integrity of models used in valuations for certain housing mortgages. The rule requires adoption of compliance management systems to ensure a high level of confidence in estimates, protect against data manipulation, avoid conflicts of interest, randomly test and review the processes and comply with nondiscrimination laws.

Next, the CFPB joined several other federal financial regulatory agencies to propose a rule to establish data standards to promote “interoperability” of financial regulatory data across the agencies. The proposal would establish data standards for identifiers of legal entities and other common identifiers.

Also in August, the CFPB responded to the U.S. Treasury’s request for information on the use of artificial intelligence in the financial services sector. The CFPB emphasized that regulators have a legal mandate to ensure that existing rules are enforced for all technologies, including new technologies like artificial intelligence (AI) and its subtypes. It’s clear that the CFPB has an interest in how those technologies are used and what the consumer impact may be.

In September, the bureau issued its annual report on debt collection, which highlighted aggressive and illegal practices in the collection of medical debt and rental debt. The report focused on improperly inflated rental debt amounts and on debt collectors’ attempts to collect medical bills already satisfied by financial assistance programs, also noting that many medical bills from low-income consumers do not get addressed by financial assistance in the first place.

Finally, the CFPB published guidance to help federal and state consumer protection enforcers stop banks from charging overdraft fees without having proof they obtained customers’ consent. Under the Electronic Fund Transfer Act, banks cannot charge overdraft fees on ATM and one-time debit card transactions unless consumers have affirmatively opted in.

Disjointed Consumer Sentiment Weighs Heavy

A September Consumer Survey of Expectations found that Americans anticipated higher inflation over the longer run as their expectations of credit turbulence rose to the highest level since April 2020, according to the Federal Reserve Bank of New York. While perceptions and expectations for credit access improved, the expected credit delinquency rates rose again and hit the highest level in more than four years. According to the survey, the average expected probability of missing a debt payment over the next three months rose for a fourth straight month to 14.2%, up from 13.6% in August, suggesting some Americans are concerned with their ability to manage their borrowing.

Despite inflation easing, consumers perceive that the costs of everyday items are on the rise. According to the latest report from PYMNTS Intelligence, which tracks the percent of consumers living paycheck-to-paycheck, 70% of all consumers surveyed said their income has not kept up with inflation. This feeling is stronger for paycheck-to-paycheck consumers, with 77% of those struggling to pay bills on time reporting that their income hasn’t kept up with rising costs. Even for those not living paycheck to paycheck, 61% shared this concerning sentiment. As a result, consumers are buying cheaper or lesser quality alternatives, if they’re buying at all.

Prior to the September interest rate cuts, the Conference Board’s Consumer Confidence Index showed consumer confidence plunging to the most pessimistic economic outlook since 2021, based on a weaker job market and a high cost of living. Americans reported being anxious ahead of the upcoming election and assessments of current and future business conditions and labor market conditions turned negative.

However, following the Fed’s rate cut announcement, another report from the University of Michigan’s sentiment index showed a rise in late September, reaching a five-month high on more optimism about the economy. Consumer expectations for price increases dropped simultaneously with more expectations for declining borrowing costs in the coming year. Consumer sentiments on their finances directly impact their spending and payment behaviors, so understanding where they stand can inform a better debt collection approach.

What Does This Mean for Debt Collection?

You’ve heard of Christmas in July, but Christmas in September? With the holiday shopping season starting earlier and in the midst of a high-stakes election, consumers will continue to prioritize expenses and spending based on their current financial outlook, which hasn’t yet caught up with the optimism showing up in the overall economy. The unknowns of what happens post-election along with the delayed impact of lower interest rates and inflation on spending leave the outcome for consumer finances uncertain. Delinquencies continue to persist and it may be some time before the benefits of a friendlier economy show up in consumers’ bank accounts. For companies looking to recover delinquent funds now, understanding how, when and in what way to engage consumers can increase recovery success. For lenders and collectors, here are some things to consider for 2025 planning:

• Self-serve = more repayment. For both businesses and consumers, reducing the need to engage directly with human agents to make payments or access account information saves time and resources. Solutions like self-serve portals represent a shift towards greater consumer control over their financial health, providing an efficient way for individuals to address and manage their finances—and debts specifically—on their own terms.

• Omnichannel or bust. If your business relies solely on one channel for customer communications, it’s time to evolve. Utilizing a combination of calling, emailing, text messaging and even self-serve online portals is the preferred experience for 9 out of 10 customers. And it’s not just beneficial for consumers–the omnichannel approach has been shown to increase payment arrangements by as much as 40%!

• Keep an eye on compliance (or make sure your debt collector does). The regulatory landscape will continue to change, especially post-election. Your risk and success hinges on how well you can keep up with the changes, so having someone responsible for monitoring and tweaking your strategy is critical.

The dog days of summer are ahead, and with inflation and high interest rates still sticking around, consumers in the U.S. will be feeling the heat financially. Consumer sentiment and data-based indicators tell some of the story, but what better way to gauge the consumer financial landscape than by looking at how people spend their free time and money?

While consumers embraced the ‘YOLO economy’ coming out of pandemic times – spending wildly on products and experiences – today’s high inflation, low savings and a cooling job market have shifted priorities for many, leading to weakened consumer spending. And businesses are responding accordingly to the lower demand – several top musical acts from Jennifer Lopez to the Black Keys have canceled summer tours due to low ticket sales while retailers like Walmart and Target are lowering prices on certain goods to appeal to budget-strained shoppers.

Despite families looking for ways to save this summer, their vacation plans must go on. The Transportation Security Authority has been anticipating and reporting record air travel numbers while a recent LendingTree survey found that 45% of parents go into debt to pay for a Disney vacation and few have regrets about it, indicating people will still prioritize spending for some experiences.

Meanwhile, the Consumer Financial Protection Bureau (CFPB) has been busy, with new rules impacting lenders and collectors across the spectrum. What does this all mean and what’s the outlook for the second half of the year? Read on for our take on what’s impacting consumer finances, how consumers are reacting and what else you should be considering as it relates to debt collection in 2024.

What’s Impacting Consumers?

Inflation finally started slowing in May and then showed a decline in June, landing at 3% from a year ago and the lowest level in more than three years. Both headline and core inflation beat forecasts but housing costs continued to rise and remain a key contributor to inflation. Being heavily weighted in the Consumer Price Index (CPI) formula, it’s unlikely to see big drops in CPI until these costs start to fall. In June, Federal Reserve officials held the key rate steady and penciled in a single rate cut this year while forecasting four in 2025, reinforcing calls to keep borrowing costs higher for longer. Meanwhile, the labor market has moved close to its pre-pandemic state and the overall economy continues to grow at a solid pace.

But even the 2% drop in the energy index won’t be enough to combat the inflated cost of keeping cool this summer, with predicted extreme heat set to drive home cooling costs up to a 10-year high. The average cost of keeping a home cool from June through September is set to reach $719, nearly 8% higher than last year and a big jump from the 2021 average of $573. Concerningly for lower-income households, organizations distributing federal financial support expect they’ll be able to help roughly one million fewer families pay their energy bills this year, in part due to government funding for the Low Income Home Energy Assistance Program (LIHEAP) falling by $2 billion from last fiscal year.

Coming out of Q1, total household debt rose by $184 billion to reach $17.69 trillion, according to the Federal Reserve Bank of New York’s latest Quarterly Report on Household Debt and Credit. Mortgage and auto loan balances continued climbing, increasing to $12.44 trillion and $1.62 trillion respectively. Overall, delinquency indicators decreased positively as we moved through Q2 as seasonally expected, partly due to tax season. In May, overall delinquent balances (30+ DPD) increased by 3.46%, driven by a 6.06% increase in delinquent mortgage balances. But mortgage was an exception, not the norm: there was a 0.55% decrease MoM in 30+ DPD delinquent accounts overall.

Credit card balances also declined seasonally as expected in Q1 to $1.12 trillion, but new delinquencies rose with nearly 9% of credit card balances and 8% of auto loans transitioning into delinquency. Despite this latest decrease, credit card balances are still up $259 billion since the fourth quarter of 2021. Thanks to record interest rates, stubborn inflation and other economic factors, credit card balances are likely only going to climb, despite what we saw in the first half of the year.

The verdict is still out on how those with student loans are faring with resumed payments. Missed federal student loan payments will not be reported to credit bureaus until the fourth quarter of 2024. Because of these policies, less than 1% of aggregate student debt was reported 90+ days delinquent or in default in the first half of the year and will remain low through the end of the year.

Busy Season at the CFPB

With a flurry of announcements in the past few months, the CFPB has been busy. The biggest win: a long-awaited United States Supreme Court decision came out in May ruling that the CFPB’s funding is constitutional, leaving the Bureau free to uphold its mission of protecting consumers and ensuring that all Americans are treated fairly by banks, lenders and other financial institutions.

On the consumer fairness front, and after releasing research showing that 15 million Americans still have medical bills on their credit reports despite changes by Equifax, Experian and TransUnion, the CFPB proposed a rule to ban medical bills from credit reports, a move that would remove as much as $49 billion of medical debts that unjustly lower consumer credit scores. In another attempt to help consumers by bringing homeownership back into reach amidst high interest rates and home prices, the CFPB also started an inquiry into mortgage junk fees and excessive closing costs that can drain down payments and push up monthly mortgage costs.

As related to business operations oversight, in June the CFPB issued a new circular on “unlawful and unenforceable contract terms and conditions in contracts for consumer financial products or services.” This warning makes it clear that it is a UDAAP (Unfair, Deceptive, or Abusive Acts or Practice) to have an unlawful, unenforceable term in contracts with consumers.

Later in June, the CFPB also finalized a new rule to establish a registry to detect and deter corporate offenders that have broken consumer laws and are subject to federal, state or local government or court orders. This registry will help the CFPB to identify repeat offenders and recidivism trends to hold businesses accountable as historically, nonbank entities faced inconsistent oversight, making it challenging for regulators to identify and address potential risks to consumers.

As the CFPB works to accelerate the shift to open banking in the United States, it also announced a new rule establishing a process for recognizing data sharing standards and preventing dominant incumbents from inhibiting startups.

At the end of June, the Supreme Court overturned the Chevron doctrine, a precedent that has allowed federal agencies like the CFPB significant authority to interpret ambiguous laws. This means that judges will use their own judgment to interpret laws rather than deferring to agency interpretations, making it easier to challenge and overturn agency regulations. As a result, the industry’s regulatory framework will become more unpredictable as courts take a larger role in interpreting laws and will require businesses to monitor and adapt their compliance and legal strategies.

A Roller Coaster of Consumer Sentiment

The first half of 2024 has been an economic roller coaster for consumer spending, resulting in whiplash for consumer sentiment. While the soft landing may still be on track, that track doesn’t appear to be as straightforward as hoped. There is an onslaught of mixed messages from, “consumers are proving to be more resilient than expected as they continue to spend, staving off what had been predicted to be an inevitable recession” to “consumers are actually financially stretched from depleting their pandemic-era savings and battling ongoing inflation and higher interest rates”.

The latest Paycheck-to-Paycheck report from PYMNTS Intelligence found that as of March, 58% of all U.S. consumers live paycheck to paycheck, regardless of their income levels. Causes for this financial situation vary and range from insufficient income and family dependents to large debt balances and splurging unnecessarily. While financial goals also vary across consumer segments, paying down debt is one common goal across all generations: 15% of Gen Z, 20% of millennials, 23% of Gen X and 22% of baby boomers and seniors said repaying debt is a priority.

Recent consumer surveys have found that 22% of respondents expressed feeling less discomfort about spending a lot of money when using a credit card, and more than half reported they are more likely to make impulse purchases when using cards. Whatever the sentiment, people are feeling some confidence to continue to spend and continue to carry a debt balance, with 41% of consumers reporting a revolving month-to-month balance on their credit cards.

What Does This Mean for Debt Collection?

Between these highs and lows of economic indicators and consumer sentiment, a serious fact remains for businesses: delinquency will continue to be an issue through 2024. For companies looking to recover those delinquent funds, understanding how to communicate with consumers where they are in this roller coaster can mean the difference between repayment and write-off. For lenders and collectors, here are some things to consider:

Shift the collection mindset. Pivoting debt resolution operations from only being focused on roll rates and placements to a more consumer-centric engagement strategy is the first critical step to productively engaging consumers.

Customization is key. Effective debt recovery communications will resonate with consumers and match where individuals are with the right message to engage with empathy and options for repayment; the right channel to engage through their preferred method of communication; and the right time to engage on their own terms when they are ready.

Don’t skimp on compliance. Not only does following the rules of debt collection keep you out of hot water, adhering to the consumer-friendly rules will set up the best possible experience for consumers, leading to better engagement and repayment rates. Here’s a comprehensive look at what you need to know about collections compliance to get started.

2023 brought a whirlwind of an economy, and we spent most of the year trying to predict when things would finally turn around. The good news is that things are looking up, and so are consumer sentiments on their financial outlook. Despite the optimism, consumers are still battling high prices and interest rates, though the holiday shopping numbers would make you think otherwise. For consumers, the challenge of balancing finances persists and holiday spending hangovers are adding to the swing. If you’re a creditor or collector working with financially distressed borrowers, considering consumer situations against the economic landscape and accommodating their financial needs and preferences when collecting is critical to your success.

Read on for our take on what’s impacting consumer finances and our industry, how consumers are reacting, and why employing digital strategies to boost engagement is more important than ever for debt collection in 2024 and beyond.

What’s Impacting Consumers and the Industry?

After a lengthy struggle against inflation and high interest rates, the economy is showing welcome signs of strength and stability, ending the year in a far better position than most predicted. Headline PCE fell 0.1% in November and was up only 2.6% from last year, unemployment remained flat at 3.7% and the economy grew at an annual rate of 4.9% from July to September. The Federal Reserve has indicated that the rate hikes are finished and it will be looking at cutting rates starting in 2024, an encouraging sign for the economy and consumers.

The fourth quarter marked the resumption of student loan payments for 22 million Americans, but repayment results were low. In October, the first month of resumed payments, 8.8 million borrowers missed their student loan payment—that’s 40% of loan holders. Some of this miss is attributed to an overwhelmed system and people making use of the Education Department’s 12-month “on-ramp” period, which guarantees that missed payments will not be reported to credit agencies until September 2024, protecting borrowers from the harshest consequences of missed payments like delinquency, default and collections. But interest will continue to accrue and only time will tell how much of this miss is actually due to inability to repay and what that will mean for those who can’t.

The Consumer Financial Protection Bureau (CFPB) has had its hands full overseeing actors across sectors–from regional and large banks to auto and online lenders to mortgage and credit agencies–in an ongoing effort to protect consumers in an ever-growing landscape of financial product offerings. And as offerings grow, so do the issues the CFPB must watch. In Q4, the CFPB issued statements and proposed rules relating to accelerating open banking, oversight of big tech companies and other digital financial service providers, and discrimination concerns. Bureau director Rohit Chopra himself has an eye on the future, saying he’s concerned that a handful of firms and individuals could wield “enormous control over decisions made throughout the world” with advances in artificial intelligence.

The CFPB also took a close look at fees and interest rates, issuing guidance to stop large banks from charging illegal fees for basic customer service and finding that many college-sponsored financial products offer students unfavorable terms and unusual fees. And despite recent changes at banks and credit unions that have eliminated billions of dollars in fees charged each year, a December report found that many consumers are still being hit with unexpected overdraft and nonsufficient fund (NSF) fees. A reported 43% were surprised by their most recent account overdraft, while 35% thought it was possible and only 22% expected it.

Key Indicators and Consumer Finances

According to the New York Fed’s Quarterly Report on Household Debt and Credit, total household debt increased by $228 billion (1.3%) in the third quarter of 2023 to $17.29 trillion. Breaking it down, credit card balances increased by $48 billion to $1.08 trillion in Q3 2023, showing a 4.7% quarterly increase while auto loan balances rose by $13 billion and now stand at $1.6 trillion. Student loan balances also increased by $30 billion up to $1.6 trillion. Other balances, which include retail cards and other consumer loans, increased by $2 billion.

Experian’s Ascend Market Insights for November reports overall delinquency (30+ DPD) rose in November, with a 7.26% increase in delinquent units and an increase of 3.54% in delinquent balances month over month. Serious delinquency (90+ DPD) continued to rise month-over-month for all products except auto loans, which appear to be stabilizing. Credit card delinquency rates, on the other hand, rose sharply in Q3, landing at 5.3% and up more than 2% from the previous year. Notably, according to a Liberty Street Economics blog post examining the composition of newly delinquent credit card borrowers, the rise in credit card delinquency rates is broad across demographics, but is particularly pronounced among millennials and those with auto loans or student loans.

After months of increasing delinquency rates, it’s not surprising that charge-off rates are following. The charge-off rate for all consumer loans was 2.41% at the end of Q3, up from 1.32% a year ago. As for credit card debt, the charge-off rates clocked in at 3.79%, up more than a half point from Q2 2023 and up from 2.1% a year ago.

The savings rate fell to 3.8% in Q3, down from 5.2% in Q2, while consumer spending jumped by 4%. This spending helped drive up the quarter’s GDP growth rate, but less saving could be a sign of financial strain amidst nagging high prices. And the excess savings from the pandemic? Americans outside the wealthiest 20% of the country have run out of extra savings and now have less cash on hand than they did when the pandemic began, which could spell trouble for consumers in the event of an emergency or unexpected life event. About 116,000 consumers had a bankruptcy notation added to their credit reports in Q3, slightly more than in the previous quarter. And currently, approximately 4.7% of consumers have a 3rd party collection account on their credit report.

Consumer Sentiment on Financial Outlook Improves

The economy’s resilience seems to be encouraging for consumers, with Americans’ perceived likelihood of a recession in the next 12 months falling in December to the lowest level seen this year. In fact, the Conference Board Consumer Confidence Index® increased to 110.7, up from a downwardly revised 101.0 in November. The overall increase in December reflected more positive ratings of current business conditions and job availability, combined with less pessimistic views of business, labor market and personal income outlook over the next six months.

The Federal Reserve Bank of New York’s November 2023 Survey of Consumer Expectations supports the optimistic findings. The report found that median one-year ahead inflation expectations declined by 0.2 % in November to 3.4%—the lowest reading since April 2021. Combining economic optimism with a decline in expected spending, the result is a 0.2% decrease in the average perceived probability of missing a minimum debt payment over the next three months, which is good news for lenders.

Similarly, Deloitte’s ConsumerSignals financial well-being index, which captures changes in how consumers are feeling about their present-day financial health and future financial security based on the consumer’s own financial experience, increased to 101.4 in November, up from 99.1 last month and up from 97.6 a year ago. The overall takeaway is that many consumers are feeling better about their financial situations and are more optimistic about the future of the economy.

Preparing for Debt Collection in 2024

Optimism about the economy’s turnaround hasn’t hit wallets just yet—consumers are still feeling the financial pinch of the high costs of rent, groceries and other basics that haven’t started retreating to pre-pandemic levels. But that didn’t stop holiday shopping—U.S. consumers spent a record $9.8 billion in Black Friday online sales, up 7.5% from 2022. Cyber Monday numbers were even stronger—consumers spent $12.4 billion, up 9.6% from the previous year. And those figures don’t include the 118.8 million Americans who spent money at brick-and-mortar stores on Black Friday weekend.

Today’s consumer is using more and different financial products to cover the cost of the holidays, and Buy Now, Pay Later (BNPL) was a big driver of purchasing power this year amidst elevated interest rates. BNPL purchases, which allow shoppers to buy items on short-term credit and frequently with no interest, also reached a record high on Cyber Monday, making up $940 million of the total online spending—an increase of 42.5% over last year. While a helpful product for consumers, BNPL can be tricky as it doesn’t show up on most credit reports and can be an invisible and unaccounted-for debt burden.

Every year, an estimated one-third of American adults go into debt to pay for holiday expenses. Growing debt balances, stubborn interest rates and elevated prices are still a thorn for consumers, and contribute to their overall financial stability. For lenders, service providers and debt collectors, guaranteeing repayment will still be a challenge as we start into 2024. So what’s the best way forward in engaging customers in debt collection who are balancing expenses and a bit of a holiday shopping hangover? Here are some things to consider:

Prepare for timely factors. Keep in mind post-holiday bills can make January a difficult month to collect from consumers. But tax season is almost here, when consumers’ refunds create a better scenario for repayment of past-due balances. Plan for this time accordingly and ensure your engagement strategy is in place before February.

Consider email deliverability. Just sending emails doesn’t guarantee your message will reach your customer. With inundated inboxes, your outreach strategy needs to include how to cut through the clutter and ensure successful email delivery of your customer communications. Learn more about deliverability, the most important debt collection metric you probably aren’t measuring, and how it impacts your debt collection efforts.

Options are your way forward. If there’s one thing we’ve learned from our consumer interactions, including the 16.5 million we added in 2023, it’s that no two consumers are the same, and what works for one may not work for the next. That’s why options are so important—in communication channel, customer support method, and perhaps most importantly, in repayment. Give your customers options for engagement and payment (think partial payments, payment plans, etc.) and you’ll likely see better collection results and customer experience.

With tumult in the banking industry in Q2 and inflation and economic stressors persisting, the financial outlook for American consumers remains uncertain. The ending of various pandemic-era benefits including the pause on student loan payments will impact consumers in the coming months. Student loan holders hoping for financial relief were disappointed in a Supreme Court decision that rejected President Biden’s plan to cancel more than $400 billion in student loan debt for millions of borrowers. Lawmakers are looking for other relief options, but in the meantime, many consumers will face higher monthly scheduled payments than they can cover, leading to delinquencies across credit types. If you’re a creditor or collector working with financially distressed borrowers, considering consumer situations and preferences when attempting to collect and employing digital strategies to boost engagement are more important than ever.

Read on for our take on what’s impacting consumer finances and our industry, how consumers are reacting, and what else you should be considering as it relates to debt collection in 2023.

What’s Impacting Consumers and the Industry?

High inflation and interest rates hung around in the second quarter of 2023. Inflation continued to ease month over month in May, landing at 4%, which is still double the Federal Reserve’s target of 2%. The CPI rose 0.2% in June on a seasonally adjusted basis, after increasing 0.1% in May, according to the U.S. Bureau of Labor Statistics. The index for shelter accounted for more than 70% of the increase, with the index for motor vehicle insurance also contributing.

In June, after 10 straight rate hikes, the Federal Reserve left the policy rate unchanged at the 5%-5.25% range, to allow time to see impacts from previous rate hikes. But “a strong majority” of Fed policymakers expect they will need to raise interest rates at least two more times by the end of 2023. Showing unexpected resilience despite higher interest rates, a late-June Commerce Department report showed the U.S. economy grew at a 2% annual pace from January through March as consumers spent at the fastest pace in nearly two years despite ever-rising borrowing costs.

In Q2, the pandemic-era benefit around Medicaid came to an end and has impacted more than 1.5 million Americans who lost health insurance coverage in April, May and June. Because only 26 states and the District of Columbia had publicly reported this data as of June 27, the actual number of people who lost coverage through the government’s main health insurance program for low-income people and people with certain disabilities, is undoubtedly much higher. The federal government has projected that about 15 million people will lose coverage, including nearly seven million people who are expected to be dropped despite still being eligible.

On the regulatory front, data protection is making headlines. Updates to the Gramm-Leach-Bliley Act (GLBA), the Safeguards Rule, provide financial institutions, including those in the accounts receivable management industry, with requirements on how to safeguard customer information, went into effect on June 9. The amendments lay out a more prescriptive recipe for the safeguards financial institutions must have in place around collecting, storing and transmitting consumer information. Several states have actively been considering and passing new legislation requiring additional policies, controls, and practices not only in the data security space but also for data privacy and data breaches.

Meanwhile, the Consumer Financial Protection Bureau (CFPB) published a Small Entity Compliance Guide covering the amendments to the Equal Credit Opportunity Act and Regulation B, requiring that financial institutions compile and report certain data regarding certain business credit applications, including examples that explain how the requirements should be applied.

There were also a couple of notable court decisions impacting debt collectors last quarter. First, the 6th circuit court of appeals determined that one phone call under the Telephone Consumer Protection Act (TCPA) is enough to establish standing, meaning the suit is based on an actual or imminent alleged injury that is concrete and particularized and, for the plaintiff in Ward v. NPAS, Inc., to establish a concrete injury.

Second, and in a victory for TrueAccord, the Northern District of Illinois showcased the benefits of digital collection as the court found that receiving an email about a debt is less intrusive to consumers than receiving a phone call. In the Branham v. TrueAccord opinion, the court found that unlike telephone calls, two unwanted emails are insufficient to confer standing and wouldn’t be “highly offensive” to the reasonable person.

Key Indicators and the Student Loan Predicament

According to the New York Fed’s Quarterly Report on Household Debt and Credit, total household debt increased in the first quarter of 2023 by $148 billion (.9%) to $17.05 trillion. Debt increases showed up across almost all categories, with larger balances for mortgages, home equity lines of credit, auto loans, student loans, retail cards and other consumer loans. Looking like an outlier, credit card balances were flat at $986 billion during Q1, but reading between the lines, this is the first time in more than 20 years that there hasn’t been a seasonal outright decline in that category.

And demand for more credit continues, which will drive household debt balances up farther. According to Experian’s June Ascend Market Insights report, new account originations were up 3.5% month over month with related balances up 7.7%. Breaking this down, auto loan account originations were up 0.7%, first mortgages were up 18.2%, while personal loans, HELOCs and second mortgages all grew significantly as well.

Indicators show that delinquency is here to stay. Experian reports that overall 30+ days past due (DPD) accounts showed a 0.4% increase month over month in May. While unsecured personal loan delinquency, which grew quickly in 2021 and 2022, has fallen for the fourth month in a row, this may be due to accounts progressing through delinquency – collections and charge-off rates for unsecured personal loans have grown to nearly 8% of balances. Auto loans, and particularly those in the subprime category, are seeing delinquency rates surpassing levels last seen during the Great Recession, coming in at 1.69% for 60+ DPD in Q1 2023.

Experian also reports that 1% of all consumer accounts rolled into higher stages of delinquency in April, which is in line with pre-pandemic norms and significantly higher than it was during the pandemic. Notably, 0.29% of accounts rolled into a lower delinquency status during May, a sign of collection effectiveness and of the relative financial health of delinquent consumers. This metric is still far below its historic norms and will be an important metric to watch as millions of consumers face higher monthly scheduled payments later this year tied to student loans.

After three years of relief from payments on $1.6 trillion in student debt under the CARES Act, student loan debt is scheduled to begin accruing interest in September 2023, with payments due starting in October. 40+ million borrowers who paid $200 to $299 on average each month in 2019 will soon face the resumption of a bill that is often one of the largest line items in their household budgets.

What’s more, research shows that student loan borrowers used extra space in their budgets during the pause to increase their leverage. Rather than paying down other debts, those eligible for the pause increased their leverage by 3% on average, or $1,200, compared with ineligible borrowers. According to the CFPB, as of September 2022, 46% of student loan borrowers had scheduled monthly payments for all credit products (excluding student loans and mortgages) that increased 10% or more relative to the start of the pandemic.

The CFPB also reports that approximately 2.5 million student loan borrowers already had a delinquency on a non-student loan as of March 2023. That’s an increase of around 200,000 borrowers since September 2022, and that’s still without a monthly student loan payment obligation. This signals that many borrowers aren’t or won’t be in a financial position to repay or will face delinquencies on other loans in order to do so. For a data-driven look into this topic, read our report, “Consumer Finances, Student Loans and Debt Repayment in 2023”.

Consumers Feel a Pinch but Remain Optimistic

As daily life continues to be more expensive for everyone, PYMNTS’ research finds that 61% of consumers lived paycheck to paycheck in April 2023, similar to the year prior. And the data shows that consumers in urban centers are especially feeling the financial crunch, likely due to a connection to cost of living, with 7 in 10 living paycheck to paycheck. Wealthier consumers comprise a growing portion of the paycheck-to-paycheck cohort, with the share of consumers annually earning more than $100,000 who live paycheck to paycheck increasing 7% from April 2022.

The US personal savings rate hovered at 4.6% in May, which is double last year’s record lows but still down significantly from pre-pandemic averages. Easing inflation seems to be improving consumers’ financial outlook, with fewer respondents citing concerns around savings levels, delaying large purchases, and worsening personal financial situations. However, the number of consumers feeling anxious about their job or employment situation steadily increased to 25% in May, up from 18% in February.

According to the Federal Reserve Bank of New York’s May 2023 Survey of Consumer Expectations, the average perceived probability of missing a minimum debt payment over the next three months increased by 0.7% to 11.3% in May. The increase was largest for respondents below the age of 40 with no more than a high school education, and those with a household income below $50k. Additionally, households’ perceptions and expectations for credit conditions and their own financial situations all deteriorated slightly.

For Debt Collection, Digital is Now a Must-Have

While consumers balance budgets amid high costs of living, more and more are using streamlined, digital payment methods. New studies show consumers are embracing the convenience of digital payments via payment portals even for healthcare bills, noting how it can minimize pain points in the payments process. Today, 9 out of 10 customers want an omnichannel experience with seamless service between communication methods, and transacting where it’s convenient for them, on mobile devices, is even better.

According to the Pew Research Center, reliance on smartphones for online access is especially common among younger adults, lower-income Americans and those with a high school education or less. In fact, 87% of TrueAccord consumers visit our web portal from their mobile devices and tablets, not their desktop computers. Choosing not to engage via digital methods can hurt vulnerable populations of consumers who primarily conduct most of their affairs digitally.

If your business has been relying on calling alone for customer communications, it’s time to shift gears to a more effective way of maximizing repayment and conversion rates in a challenging financial environment. For lenders or collectors engaging with distressed borrowers, here are ways digital can boost your efforts:

1. Cost-effective customer communications at scale. When almost all communications with consumers can happen electronically via email and SMS with no human interaction, the cost of agents, who now only manage inbound emails or calls from already engaged customers, is reduced. Lenders that have implemented digital-first solutions have seen their cost of collections fall by at least 15%.

2. Online payment portals. When consumers can make payments online when it’s convenient for them, they’re more likely to repay. Add options like payment plans and flexible payment days to appeal to distressed borrowers and see repayment and liquidation rates improve.

3. Code-based compliance. When compliance is coded into an algorithm that helps make decisions on customer engagement in debt collection, you can ensure that all digital communications fall within federal and state laws and regulations. Compliance built into the code can help prevent costly mistakes especially with the complex patchwork of regulations.

Disclaimer: The information provided in this blog post does not, and is not intended to, constitute legal advice.

Protecting consumer privacy is not an unfamiliar concept in our industry and it’s something that should already be woven into our policies, procedures, and practices. With the rapid increase of state privacy laws across the United States, any company that collects, uses, transmits, or receives consumer data has to stay up-to-date on all related compliance issues.

In a previous webinar, Coast to Coast—the State of Privacy and Compliance in 2023, TrueAccord’s legal experts discussed the newest federal privacy laws and all the related compliance issues. Watch the full webinar on-demand now!

The passage of the FTC’s Safeguards Rule, amending the Gramm Leach Bliley Act (GLBA), has been a big topic in data security conversations across the financial services industry as businesses prepare to be in compliance on or before the extended effective date of June 9, 2023. Meanwhile, several states have actively been considering and passing new legislation requiring additional policies, controls, and practices not only in the data security space but also for data privacy and data breaches. It is important for Chief Information Security Officers, Privacy Officers, and Chief Compliance Officers to stay on top of this legislation, as well as Chief Executive Officers since we have seen many federal and state actions naming the CEO in their individual capacity for failing to properly secure and protect data or to properly delegate these responsibilities to the appropriate persons within their organizations.

**Please note this article is not legal advice. This is not an exhaustive list of all laws. You should consult a lawyer if you have questions about federal and state data security, privacy or breach laws.

Data Breach Laws

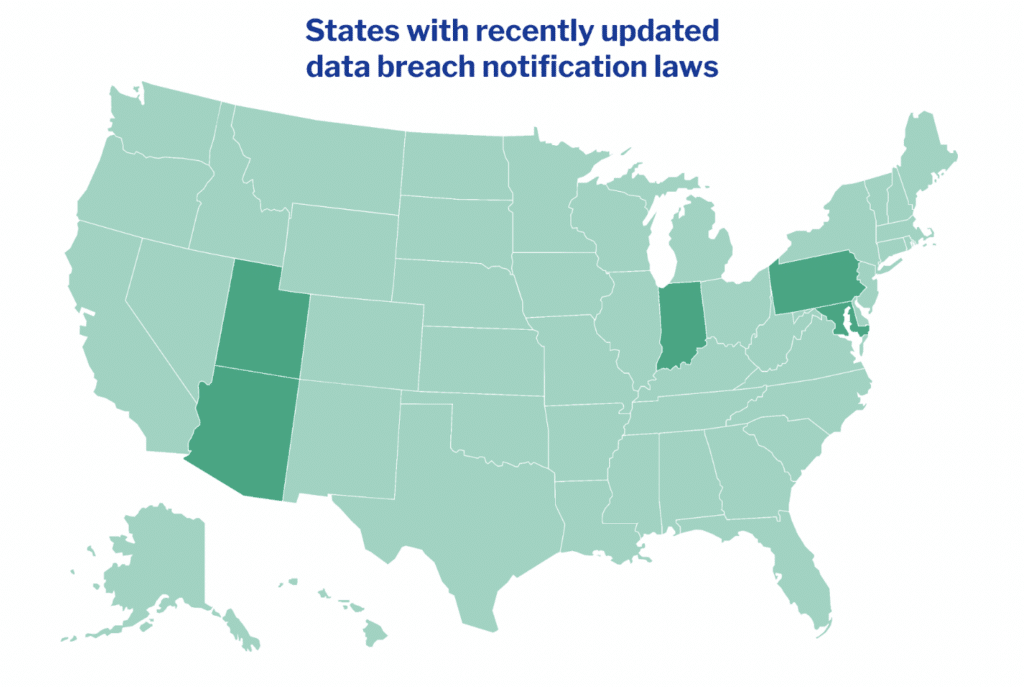

All 50 states have data breach notification laws on the books. In 2022, 19 states considered enhancing their data breach laws.

Those states that passed revised data breach laws, tightened up notification timelines, added additional definitions of what constitutes personal information, and expanded the notification requirements to include additional state agencies. For example, Arizona’s law HB 2146, amending Arizona Revised Statutes section 18-552, not only requires that notification be made to consumers but also to the Director of Arizona’s Department of Homeland Security. If the breach impacts more than one thousand people, then the law requires the notification also be given to the three largest nationwide credit reporting agencies, the attorney general, and now the Director of Arizona’s Department of Homeland Security.