After its creation the Consumer Financial Protection Bureau (CFPB) had a broad mandate covering nearly all consumer financial products. The CFPB wielded expansive rulemaking, supervision and enforcement powers. As noted in their Fiscal Year 2024 Financial Report, in 2024 alone, the CFPB conducted 26 public enforcement actions through settlement, litigation or default judgment. With the administration change, the CFPB has entered a deregulatory phase.

The new priorities represent a sharp contraction of their mission. In a memo to staff, the Bureau announced it will cut exams by half, refocus on the biggest banks, and pursue a narrower set of enforcement cases centered on clear, measurable fraud. They’ve taken a drastic step back, cutting staff, retracting years of guidance, and focusing on enforcement and some rulemaking.

The philosophical core of this shift is a policy the CFPB calls “respect for federalism.” This is an explicit directive to avoid duplicative work and let states take the lead. The internal memo to staff confirmed this is a strategic decision to shift resources away from tasks states can handle. We even see this logic in the Bureau’s justification to rescind 67 pieces of guidance, some that had provided clarity to the industry, in part due to the existing authority of state regulators. This shows a clear, deliberate handoff of regulatory responsibility.

It’s a mistake to view this as simple deregulation. In our dual-sovereignty system, a federal vacuum doesn’t lead to a void. It leads to a flurry of state-level activity. For a national company, this means replacing one predictable federal regulator with 50 unpredictable state ones.

And, not surprisingly, as a result, the states are picking up the baton and stepping up to fill the regulatory gaps. States are expanding their oversight and passing new legislation that is reshaping the compliance landscape for consumer finance and the debt collection industry. This has left many people asking the question, are states going to replace the CFPB? We’re here to help you find the answer.

How State Enforcement Works for Consumer Finance and the Debt Collection Industry

The states have the legal authority, institution structures and legislative will to fill the CFPB void. As states are taking over the reins as the main enforcement authority, their actions mainly take place at two different levels:

- State Attorney Generals: They are the chief legal officers of their respective states and primary consumer protection enforcers. They wield broad authority on state Unfair Deceptive Abusive Acts and Practices statutes. They can investigate, subpoena, and sue for penalties and restitution.

- State Financial Regulators: These are state-run agencies that oversee specific sectors of the financial industry. These agencies are usually responsible for licensing and supervising a wide range of non-bank entities, including mortgage lenders, debt collectors, and money transmitters. Some states are even hiring former CFPB employees to help get their regulations positioned to be more effective. New York, Pennsylvania and Maryland have actively recruited ex-federal workers to bolster their consumer protection efforts.

It’s also important to know that state agencies don’t operate in a silo. Many of them coordinate their efforts through interagency bodies such as the Conference of State Bank Supervisors (CSBS). By paying attention to these interagency bodies, businesses can get a better sense of debt collection compliance trends to account for in their operations.

What Are States Doing in This Enforcement Role?

Since the federal supervision activities are receding, states are taking the reins through their powers of supervision, enforcement and rulemaking. There has been a big surge in state-level legislative activity specifically aimed at areas where federal action has been slow. States are not just enforcing; they are actively writing the rules for the future:

- The Bank Partnership Model (True Lending): One area that states are cracking down on is the “rent-a-bank model”. More states are trying to move forward with closing this banking loophole by forcing companies that use the true lending model to attain the same standard as traditional banks. A main motivation for this is to help protect consumers from deceptive lending and credit practices.

- Regulation Around Fintech Products: States are moving faster than the federal government on creating rules around new financial products. As BNPL services continue to grow, New York has introduced new regulations including a new licensing system. Other states like Ohio have created “regulatory sandboxes” to see how new financial products could impact consumers before being rolled out statewide.

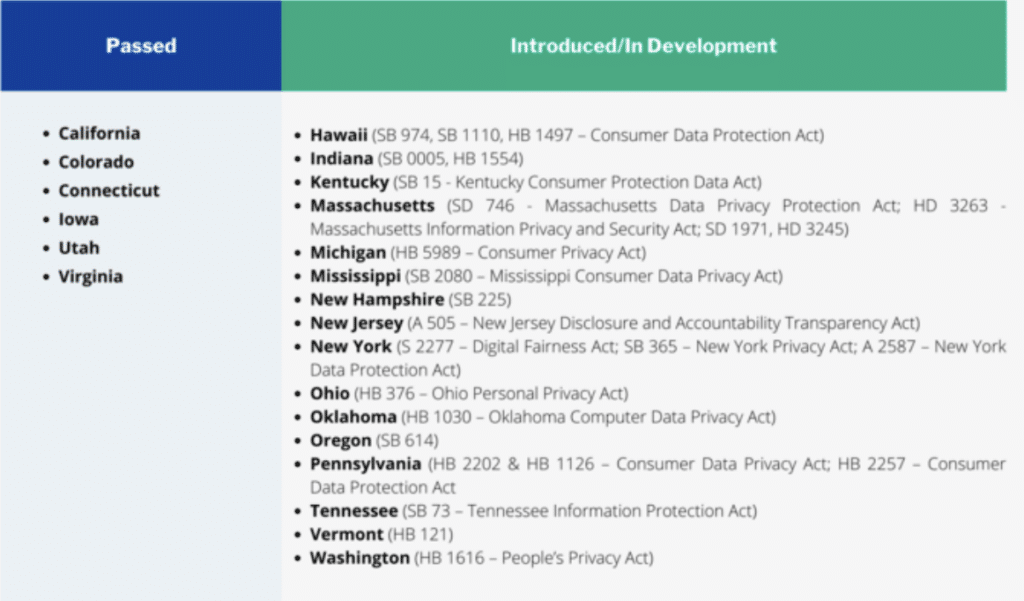

- Medical Debt: As the CFPB’s medical debt rule was struck down in the courts as an unlawful extension of regulatory authority, several states introduced similar legislation aimed to prevent medical debt credit reporting, to create state-funded debt relief programs, and to expand patient relief programs. In several states, including California, Illinois, New York, Oregon and Washington the bills passed codifying in law restrictions on credit reporting medical debt.

- Artificial Intelligence: In response to federal inaction, states have crafted their own unique legislative solutions to the challenges and opportunities presented by AI. Regulation of deepfake technology, particularly regarding non-consensual imagery, transparent disclosures when AI systems are used to interact with consumers, and formation of state-level task forces to study AI impacts and make policy recommendations. California, Colorado, Utah, Texas all have AI laws on the books with completely different requirements and definitions.

What Do These Changes Mean for Your Business and the Debt Collection Industry?

The idea that states are replacing the CFPB isn’t entirely accurate. States cannot replicate the CFPB’s most important function: creating a single, predictable set of rules for the entire country. The CFPB created a blanket of uniform rules which many states both formally and informally adopted. Today, the states are not creating a uniform floor but instead a patchwork of different requirements. This patchwork is more dynamic and, for industry, more complicated.

For any business operating in more than one state, the primary challenge is inconsistency. What is legal in Texas might be illegal in New York. This makes national product rollouts and standardized compliance programs incredibly difficult and expensive. Furthermore, enforcement is not uniform. A handful of states are very active, while many others lack the resources to bring major cases. Finally, state enforcement can be more political, with priorities changing every time a new attorney general is elected.

All of this together means that businesses are going to have to devote more resources into ensuring their collection efforts follow all the rules in the states in which they operate. This means actively tracking legislation, new regulations, and enforcement trends in every state where you do business. This can no longer be an afterthought; it must be a core compliance function. Conduct detailed, state-by-state risk assessments. Don’t assume a product that is compliant in one state is compliant everywhere. Pay extremely close attention to the bellwether states—California, New York, Pennsylvania, and Massachusetts. What happens there often doesn’t stay there; it becomes the template for other states to follow.

Following the activities of the state AGs, who are the source of the broad UDAAP actions and novel legal theories, is a must. Along with the specialized financial regulators, who control your licenses and conduct the day-to-day examinations. These are two different sources of risk that require distinct monitoring strategies.

These changes demand a more sophisticated and adaptable compliance management system. Your systems must be flexible enough to handle different disclosure requirements, different collection rules, different UDAAPs interpretations, often on a state-by-state basis. Investing in this adaptability is the key to managing risk in this fragmented landscape.

Small compliance departments face an immense, constantly evolving task and often don’t have the capability to scale their efforts to match the sheer number of new regulations that can emerge. Companies like TrueAccord can help your business leverage digital communications that are compliant at the federal and state levels.

Compliantly Scaling Your Debt Collection Efforts is Easy with TrueAccord

The regulatory landscape around financial services and debt collection will continue to evolve. While states aren’t a complete replacement for the CFPB, new state-level regulations will continue to be passed and make it more challenging for your business to stay compliant.

One of the best ways to keep up with this dynamic landscape is to partner with TrueAccord for your debt collection needs. TrueAccord combines dedicated legal experts with code-based compliance to ensure debt collection efforts are by the book. Contact our team today to learn more about how your businesses can compliantly scale your collection efforts.