Buy Now, Pay Later (BNPL) plans have taken over as a popular financing option for consumers, partly due to an increase in online shopping demands during the pandemic. In 2021, Americans spent more than $20 billion through BNPL services, taking up a bigger part of the $870 billion-a-year online shopping market. From laptops and airline flights to clothing and furniture, BNPLs make it simple to pay for almost anything in small installments. Since the start of the pandemic, millions of international consumers, especially Gen Z (10-25 years old), have gravitated toward using this service. According to a study by Forbes, BNPL use among Gen Z has grown 600% since 2019. The rise of interest in BNPL is also likely influenced by increased financial uncertainty, high-interest rates and a downward trend in credit card approval. As consumers show preference for digital financial services, BNPL continues to grow and become available at more retailers.

Why are BNPLs Popular with Gen Z?

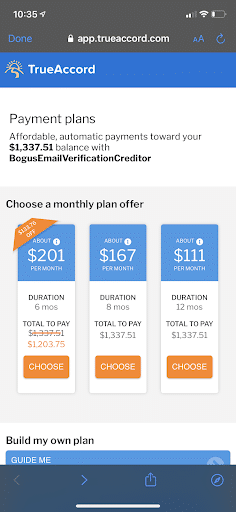

Services like Afterpay, Klarna, Affirm and others have gained a lot of popularity in recent years, especially among younger generations who may struggle with cash flow. With BNPL, the first payment is due at the time of purchase, with subsequent interest-free payments usually due within a few weeks or months.

More and more, BNPL providers are reaching these younger audiences through influencers and brands on TikTok, and the variety of goods and services you can purchase with the service continues to expand. Some popular buy now, pay later items include clothing, concert tickets, cosmetics, electronics, furniture, groceries, hotels and flights.

But, like credit cards, missing payments can result in late fees and other penalties. With Gen Z, there’s already a pattern of missing payments. A survey conducted by Piplsay showed that 43% of Gen Zers missed at least one BNPL payment in 2021.

Gen Z Favors BNPL More Than Other Generations

Debt types and payment preferences constantly change along with technology. The traditional credit card debt is being replaced by BNPL, specifically when we look at Gen Z. For one, it’s easier to be approved for a BNPL application since the process only requires a soft credit check, unlike a hard credit check that most credit card issuers require. When looking for an alternative to high-interest credit cards, BNPL installment payment plans are a popular option. BNPL consumers know upfront what will be expected of them, and the possibility for large debt build-up is replaced with a finite number of payment installments. This transparency and manageability make it easier to understand. And it’s one that has the potential to continue to evolve for the better by providing consumers with more inclusive credit and payments options.

When it comes to both luxury and essential purchases, younger consumers are more likely to take advantage of BNPL to afford them. A survey from TrustPilot found that 45% of consumers between the ages of 18 and 34 were likely to use such services for basic essentials while 54% would use them for luxury items. For those aged between 34 and 54, these results were 33% and 38% respectively. And for people aged 55 and up, the results were 16% and 24%.

Since it’s quite easy to sign up for one or more BNPL loans, the likelihood of losing track of payments or overspending is real, especially for Gen Z. According to a report from J.D. Power, about one-third of younger consumers said they spent more than their budget allows with BNPL. And since different retailers offer financing through various BNPL services, it can also be a challenge to track multiple accounts at once. This isn’t surprising as some of the younger generations do not have the financial literacy or experience that older generations have and they’re more likely to face consequences and penalties like missing a payment.

Meet Gen Z Where They Are to Effectively Recover More

The good news is that the outlook for Gen Z BNPL customers that end up with accounts in collection is different than for those who default on credit card debt. On average, BNPL debts see higher and faster repayment rates than similar-sized credit card debts. Higher engagement leads to better repayment rates. According to TrueAccord data, the percent of BNPL customers who make a payment is more than double the like-size credit card accounts at 30 days post placement and 50% higher at 90 days.

As a debt collection platform that engages digital-native consumers where they are and with a priority on customer experience, many leading BNPL providers partner with TrueAccord to address both early delinquencies and charged-off accounts. After these BNPL customers repay their loans and have a positive experience, they’re able and likely to use the service again, and this time with some experience about how it works. By using this information, TrueAccord can help find the most optimal ways to reach the younger audience and help them pay off their debt from BNPL.

Want to learn more about how to engage with consumers of any generation in whatever stage of collection they might be in? Schedule a consultation to see what TrueAccord’s digital solutions can do for your debt recovery strategy.

Further Reading:

- TrueAccord Report: Buy Now, Pay Later, Consumer Preference and Collections Outlook

- Klarna Report: https://www.klarna.com/us/blog/category/mindful-money/

- Dave Ramsey: https://www.ramseysolutions.com/dave-ramsey-7-baby-steps