Outbound calling has been the main mode of collections for decades, but the cost of a call center or in-house full-time employees (FTEs) making calls is no longer justifiable when most consumers simply don’t answer the phone, on top of the mounting compliance restrictions limiting opportunities to call in the first place.

But outbound dialing isn’t completely obsolete—digital-first omnichannel strategies can turn traditional call-and-collect operations around by integrating new digital channels into the communication mix.

Let’s compare traditional outbound calling methods versus a digital-first approach in three key areas impacting your business’s ability to collect more, faster:

- COST

- COMPLIANCE

- CONSUMER PREFERENCES

Get even more statistics and data in our latest eBook — Why Evolve from Outbound Calling to Omnichannel Engagement? Cost, Compliance, & Consumer Preferences — available for download now»»

COST: Call-and-Collect

The cost to collect has been on the rise for traditional methods for years, whether you outsource to a call center or have FTEs dialing the phones.

One reason for this rise is based on the fact that many lenders still practice old strategies to prioritize contacting customers based on their risk profiles, balance, and average days delinquent—completely missing portions of their portfolios. Factoring in propensity to pay is important to successful engagement, but it means that agents’ time is focused on only a small portion of accounts, leaving potential repayments on the table.

Add in the overhead costs, inflation, and hiring challenges of using agents as first attempts at engagement and watch the expenses continue to climb past what you’re able to collect through outbound calling.

COST: Digital-First Omnichannel

Right off the bat, digital-first shows the cost of collections can fall by at least 15%.

Since digital is infinitely scalable, this communication tactic can touch every single account, regardless of scoring models—unlike human dialers who can only physically call a certain number of accounts on any given day. Going digital-first cuts down on the time billed for making repeated outbound calls that are never answered or returned, and it allows agents to interact with customers that want to speak directly to a person.

Overall, digital-first has shown to boost customer engagement by 5x, the first step towards repayment.

COMPLIANCE: Call-and-Collect

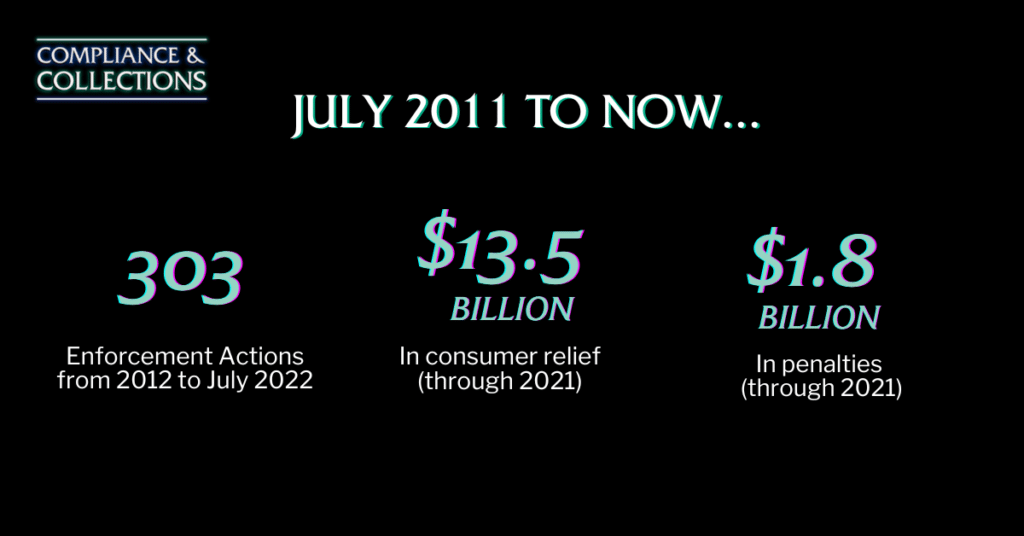

It’s no secret that it’s increasingly complicated to reach customers with all the legal communication restrictions.

While all debt collection communication is subject to compliance rules, outbound calling has specific laws and regulations that can carry costly penalties for non-compliance—and it’s only becoming more complex with new state-specific rules rolling out right and left. But no matter where your business is doing business, if you’re making collection calls you must follow these federal guidelines:

- Inconvenient Time Rule: prohibits calling before 8am or after 9pm

- Regulation F’s 7 and 7 Rule: Cannot call more than seven times within a seven-day period

- Telephone Robocall Abuse Criminal Enforcement and Deterrence Act (TRACED Act) tagging legitimate businesses as spam

- FCC Orders further restrict dialing to landlines and include opt-out requirements for prerecorded voice messages

But there is a more streamlined way to ensure your collection communications are following all the rules: enter code-based compliance.

COMPLIANCE: Digital-First Omnichannel

Code-based compliance works by programing rules that ensure all communications fall within all federal and state laws and regulations, such as:

- Frequency and harassment restrictions

- Consent requirements*

- Disclosure requirements

This digitally designed approach to compliance greatly reduces the opportunities for human error that are bound to occur in more manual processes. Additionally, the digital-first approach allows companies to continue to collect during times that calling would violate certain regulations, like the Inconvenient Time Rule. In fact, 25% of payments come in after 9pm or before 8am (the determined inconvenient times), since these hours can actually be more convenient for consumers to catch-up on digital communications they received throughout the workday.

*Generally, there is no requirement in the federal law to send debt collection communications by email, though some states are more restrictive. This is not legal advice, please consult an attorney for guidance on your unique circumstance.

CONSUMER PREFERENCE: Call-and-Collect

46% of consumers want to be reached through their preferred channels—so what are today’s consumers’ preferences?

Here’s a hint: phone calls aren’t at the top of the list.

And today’s Right Party Contact rates show it, ranging between just 0.5% – 4.0%. And out of those that do answer the phone, 49.5% of consumers take no action after a collection call. The old call-and-collect tactic may actually do more harm than good if compliance rules are ignored: out of the communication tactic complaints received by the CFPB in 2020, over half complained of frequent or repeated calls.

CONSUMER PREFERENCE: Digital-First Omnichannel

So if phone calls aren’t consumers’ preferred method of communication, then what is? For 59.5% of consumers, email is their first preference when it comes to debt collection communications. This is especially important considering that first contacting a customer through their preferred channel can lead to a more than 10% increase in payments.

This digital preference isn’t surprising since nearly nine in ten Americans are now using some form of digital payments—why would they expect collections to be any different? 14% of bill-payers prioritize payments to billers that offer lower-friction payment experiences, and digital is often preferred because of it. Digital communications are easily controlled by consumers and are tightly managed by service providers with built in mechanisms to prevent harassment (like with code-based compliance), which we know has historically been a challenge for call-and-collect practitioners.

Digital-First is the Future of Collections

And it’s here today, working for TrueAccord clients and customers.

At TrueAccord, we find that more than 96% of customers resolve debts without any human interaction when digital options are offered—reducing costs associated with outbound calling, lowering risks with code-based compliance built in, and delivering an experience that consumers prefer.

Get even more statistics and data in our latest eBook — Why Evolve from Outbound Calling to Omnichannel Engagement? Cost, Compliance, & Consumer Preferences — available for download now»»

Ready to go digital-first with your debt recovery operations? Schedule a consultation to get started today!